Bail-Ins Of “Big Deposits” In Greece Would Be “Extraordinarily Counter-Productive”

share

share

share

share

share

share

share

share

share

share

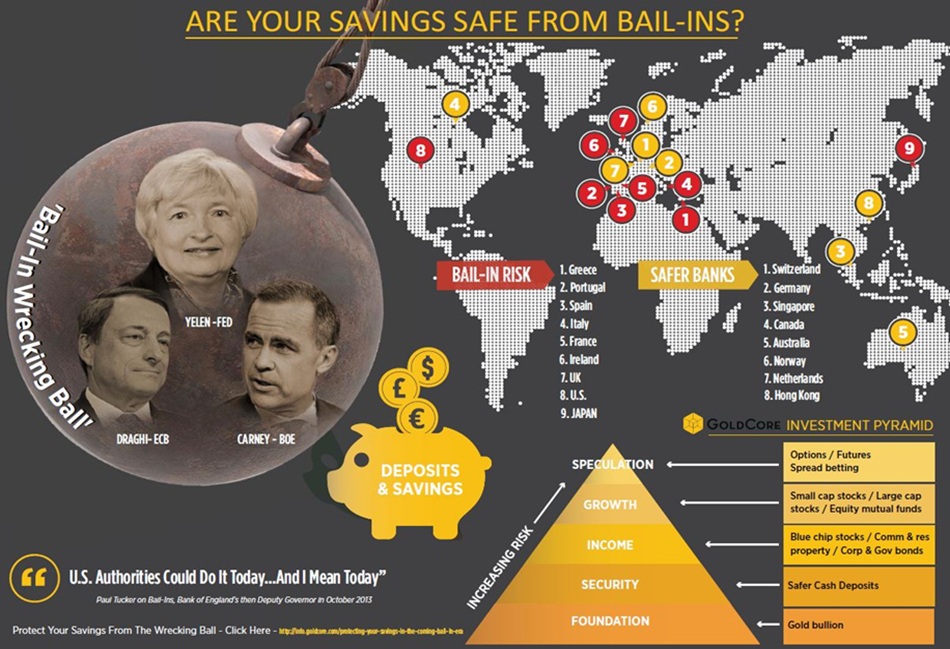

- Bail-ins are the biggest risks now facing Greek savers and businesses

- ‘The Economist’ warns bail-ins in Greece would be “extraordinarily counter-productive”

- Capital controls choking small and medium size businesses

- Greek liquidity crisis now a solvency crisis

- ELA now provides more liquidity to the Greek banking sector than deposits do

- Greece households and especially businesses worry about a “bail-in” of big deposits – above €100,000

- Financial interests of banks placed over those of small and medium businesses and taxpayers

“Bailing-in” of larger deposits would have a very detrimental effect on Greece, The Economist has warned. The magazine points out that such an action would “destroy the working capital” of small and medium size businesses, which it describes as the “backbone” of Greece’s economy.

The risk that bail-ins pose to companies, trade, commerce, employment and entire economies is something at which we have looked frequently in recent months. Indeed, we think we are largely alone in focussing in detail on the risk that bail-ins pose not just to individual savers but also to millions of small and medium size enterprises throughout the world.

See Fallout From Bail-ins More Negative than Many Realise (Irish Times, Dec 2013)

See From Bail-Outs To Bail-Ins: Risks and Ramifications – Includes 60 Safest Banks In World (Nov, 2013)

See Protecting Your Savings In The Coming Bail-In Era (Nov, 2013)

There has been little or no debate by commentators or in the media about the risks posed by bail-ins.

The cozy consensus is that bail-ins are good as they allegedly protect the taxpayers from bailing out banks. As if it is a fait accompli that banks should be bailed out by anybody – taxpayers or depositors – in the first place.

The better option of winding down failed banks is verboten in our banker-captured financial and political world.

The narrative is that bail-ins are good as they protect taxpayers. This forgets that small and medium enterprises employ millions of people who are taxpayers and contribute billions in tax revenues. Therefore, if you confiscate their deposits, their very working capital, they will not have the monies needed to pay wages and salaries of millions of employees.

Is it not before time that we have a real debate about the developing bail-in regimes and the deflationary risk they pose to western economies?

In Greece, small and medium size enterprises – the backbone of the Greek and indeed most economies – are already suffering the adverse effects of capital controls. The restrictions on transferring cash abroad has prevented them from importing the various products they use to run their businesses or sell to consumers.

The limits on cash withdrawals – now €420 per week which can be withdrawn all at once as opposed to the previous €60 daily limit – is greatly hampering their ability to do business. All business has to be done with cash and some with the return of barter.

The Economist suggests that a separate Emergency Liquidity Assistance (ELA) program be introduced to specifically to give banks greater flexibility in lending to businesses to keep them afloat.

Failure to provide emergency liquidity to businesses will lead to defaults by otherwise reasonably healthy businesses which will further undermine the balance sheets of banks, increase unemployment and further impact the already devastated Greek economy.

The Economist also makes a passing reference to the insane situation whereby businesses would have to beg their banks for credit while their own cash reserves are being withheld: “Any such improvements are likely to rely heavily on extra ELA rather than a return of deposits.”

The magazine argues that Greece now faces a solvency crisis. They almost ran out of cash during the bank runs of the past few weeks. The situation was only barely stabilised when the Greek central bank received the go ahead from the ECB to provide ELA.

The Economist also points out that, despite capital controls, ELA now provides more liquidity to the highly indebted Greek banks that customer deposits do. This underlines that the current model of treating debt crises with more debt and hoping the problem will go away is utterly stupid and futile.

It is storing up a world of financial pain in the coming months and years.

The erstwhile capitulation of Syriza likely opens the door to further ELA and a stabilisation of the Greece’s banking system but the true health of that system will only become clear when stress tests are performed in the autumn according to the magazine.

The magazine suggests that – now that a “Grexit” is off the table – “bail-ins” are the biggest concern facing Greek savers and businesses.

They argue that bail-ins are unlikely because the program is not set to be fully ratified Europe-wide until next year and suggest that assurances from Europe to Greece that “bail-ins” are off the table would help stabilise the system.

We are unclear as to whether bail-ins will be applied to Greek deposits at this time. They may not be as they would send an extremely negative message to savers throughout Europe. However, the threat of bail-ins may be used to keep Tsipras and the Greek government in line and force them to implement the new austerity regime.

The treatment of Greece – who are one side of a two sided process and who have been forced to bear the brunt of the consequences of the foolishness of the Troika in recent months has alarmed many Europeans. They are beginning to sense that policy is being directed by financial and banking interests rather than by a democratic process.

Financial interests of banks are once again being placed over those of small and medium businesses and taxpayers in general.

In the event of a systemic European banking crisis, however, laws can be changed at the stroke of a pen and “bail-in” mechanisms could become fully operational. Also, the comforting guarantee of €100,000 will be erased in such a crisis.

MARKET UPDATE – Gold “Capitulation” As Down 8% In July – Smart Money Buying Dip

Today’s AM LBMA Gold Price was USD 1,083.75, EUR 990.042 and GBP 699.89 per ounce.

Yesterday’s AM LBMA Gold Price was USD 1,101.65, EUR 1003.69 and GBP 705.91 per ounce.

Gold in USD – 1 Week

Gold fell $5.20 or 0.3% to $1,088.70 per ounce and silver was down 15 cents to $14.65 per ounce yesterday.

Today, gold in Singapore was hammered lower in another bout of concentrated selling and gold bullion in Zurich moved slightly lower.

This morning in European trading, silver for immediate delivery fell 1.3% to $14.57 an ounce. Spot platinum fell 0.5% percent to $977 an ounce, while palladium fell 0.16% percent to $619 an ounce.

Gold in EUR – 1 Week

Gold failed to maintain an early rise yesterday, slipping to a new multi-year low in New York trading hours before extending those losses overnight.

If gold ends down again today, it will have fallen in 9 out of ten sessions over the last couple of weeks.

Gold has fallen in all currencies this week. It is down 4.4% for the week and looks like it may have its biggest weekly drop since October. It has fallen for five weeks in a row, its longest such run of losses since late 2012.

On a monthly basis, gold is down 7.6% in dollar terms so far in July, their biggest monthly loss since June 2013.

Gold in GBP – 1 Week

Investors are dumping billions of dollars’ worth of gold, commodities and emerging market assets in a wave of “capitulation” selling, Bank of America Merrill Lynch said today as reported by Reuters.

Gold and copper prices have hit five and six year lows respectively this week. Funds flows data showed the biggest outflow from precious metals in four months and emerging market fund outflows reaching $10 billion over the last two weeks.

“Capitulation is beginning in emerging markets, resources and commodities,” BAML analysts wrote. The receding threat of Greece crashing out of the euro has helped deflate safe-haven demand for gold, while the likelihood of a U.S. interest rate hike this year has spooked emerging markets.

Gold and silver are oversold on a host of indicators and due a bounce. Smart money is again accumulating on the dip and we have had a busy week – with some a small amount of concerned selling but more clients adding to allocations on the current price dip.

Capitulation tends to be a good time to allocate funds by dollar cost averaging into weakness.

********

Courtesy of http://www.goldcore.com/

share

share

share

share

share

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.