COT Report: Predictably Stomach Churning But Bullish

share

share

share

share

share

share

share

share

share

share

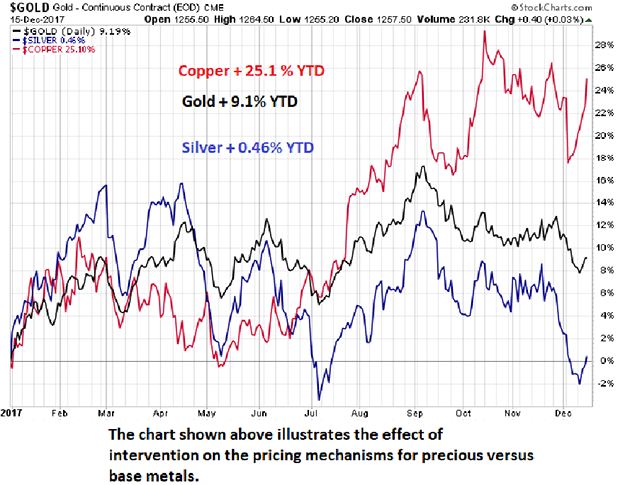

Here is a really good question. Anyone out there lose money trading gold and silver or related mining shares in the past couple of months? I did. My friends did. The bulk of the managed money (hedge fund) players did. However, it's all "JUST FINE" because the Dow and the S&P hit all-time highs again as the last vestiges of the post-2008-GFC rescue reflation is now SURGING into paper assets. More importantly, those bullion bank millennials that were hired by their uncles and fathers and grandfathers in the banking business with EXPRESS INSTRUCTIONS to contain and control precious metals have now been given leave to TAKE PROFITS. Parties will be attended; frivolity and joy will be experienced; and massive bonuses will be paid. And the prices of gold and silver reside at levels representing 9.1% and 0.46% returns, year-to-date, versus 28.86% for the NASDAQ and 1,761% for Bitcoin. Is it any wonder why this new generation of investors ignores the precious metals complex like the bubonic plague?

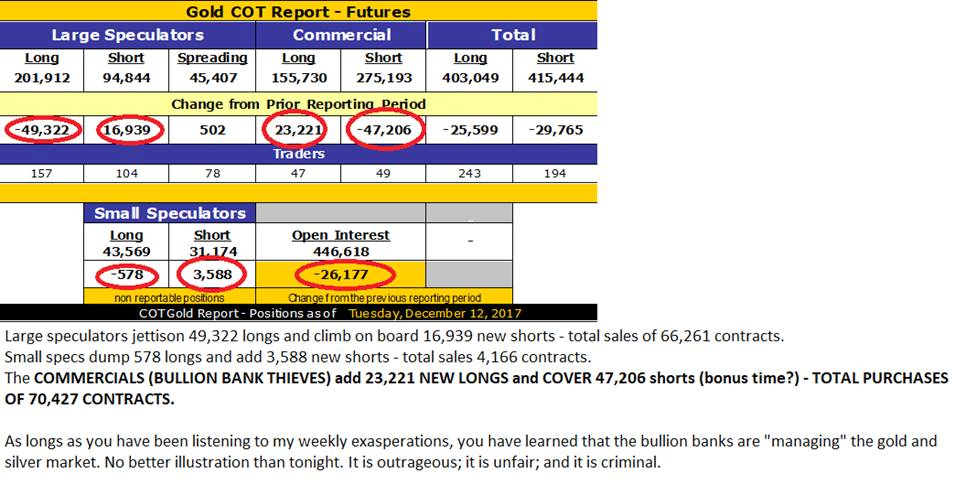

Friday's COT report (as predicted) sent waves of revulsion through every nook and cranny of this portly countenance while sending my beloved canine howling into the upper regions of the house, certain beyond all doubt that wine bottles, coffee mugs, computer monitors, and the like were destined for flight paths not unlike the space shuttle on a clear day. The inappropriate and inordinately loud string of profanities and other rage-ridden invectives came as a result of the revelation of a massive reduction in the aggregate short position in gold and silver futures held by Commercial traders, otherwise known as bullion banks. As maddening as it was, it confirmed that greed rules the waves of highly motivated behaviors that exist today in the financial markets.

I opined at the end of November that "Bullion bank short covering will become year-end profit-taking" and received confirmation last Friday when they covered the equivalent of over 5.6 million "ounces" and it set a floor for pricing as it closed with its first weekly gain in the past four and only the third up week in the last twelve. The good (and possibly GREAT) news came Friday afternoon with a 70,427-contract swing comprised of new long and covered short positions and one of the top five Commercial purchase COT weeks in history. This is a classic repeat of the lows seen in early December of 2015 and while not as extreme in terms of the aggregate short position, the size of the drawdown was breathtaking and bullish for the near-term outlook. But then again, that was the analysis I gave in late November and again last week and continue to believe that the gold miners are dirt cheap here and certainly less stretched than the valuations virtually everywhere else. There are no champagne flutes tinkling at the gold miner parties this year; it has been a "beer and pretzels" year and not a great deal of fun.

There is an expression that has stayed with me since my early days as a commodities broker that came as a quote from a book I read highlighting stories from the soybean trading pit at the Chicago Board of Trade where the legendary Richard Dennis ruled the roost. "When they're yellin', ya should be "sellin' and when they're cryin;, ya shud be buyin'!!!" was the nuts and bolts of the phrase as it clearly defined one critical rule for trading against human emotion.

And, yes, there was indeed a time when one could utilize human fear and greed as a trading tool but that went the way of the dodo bird when the bankers decided to allow computers to manage markets and set prices arbitrarily by digital committee. The elitists that are now in control of the programmers and software engineers are, however, in full grasp and grapple of what is needed to keep the throngs at bay and avoid the storming of the banker Bastille complete with pitchforks and torches. They need rising paper markets! Whether it is Bowie Bonds or cryptocurrencies or blue-chip stocks or social media, give the legions of terminally indebted university grads the hope of enrichment and credit-relief by way of ANYTHING that can be bought, sold, traded or shorted, as long as it creates "flow" upon which the bankers can slice off their piece of flesh. Global "growth" is now 100%-dependent upon the financial economy with production of literally everything the responsibility of either robots or slave minimum-wage labor located in Third World sweatshops and Emerging Market warehouses. And this peculiarity is eventually going to rise up and bite the elitist price managers squarely on the backside.

Here in Canada, the Toronto housing bubble has made geniuses out of morons and millionaires out of part-time, construction-site laborers (not that there is anything wrong with work of that ilk) but you get my point. It has turned the city into an elitist stronghold and Asian mecca (again, nothing wrong with meccas or strongholds) but gone forever is the distinctive ethnic influence of the Irish, English, and Scottish ancestry that founded the city and morbidly diluted is the dominant influence of the Italians that built it later into the massive megalopolis that it has become. The Chinese money gorging on Toronto property is not just the result of "easy money" lending policies back home but more so "easily-printed-out-of-thin-air-money" that has been the national policy instrument allowing the migration of hundreds of thousands of cashed-up immigrants into the Canadian market place. The result has been infinitely unfair advantages for the holders of the Chinese shadow banking paper that gets easily converted to loonies and toonies and winds up in the hands of former residents of WASPy neighborhoods such as Rosedale and Forest Hill.

Now that speculators around the world have moved way beyond "yellin'" to the fever pitch of high-pitched, megaphone-assisted "howlin'", the contrarian clarion call for equal and opposite reactions otherwise known as "sellin'"is long overdue. Similarly, the "cryin'" in the gold and silver pits and in the boardrooms of the junior exploration companies has been amplified to sound like Jerusalem's Wailing Wall on a particularly bad day. Accordingly, the Senior (GDX/NUGT) and Junior (GDXJ/JNUG) gold miner ETFs are the items I will be "buyin'" as a suitable response to all that "cryin'". I am also taking down yet another piece of the recently announced private placement in Stakeholder Gold Corp. (SRC.V/SKHRF.US) at $0.25 per unit (in the interest of full disclosure I do consulting work for them). With drilling having started at Goldstorm last week, it is important to remember that Stakeholder has stated that "The first drillhole will test the 100 m wide Clayton zone and transect seven discrete fault zones that could host Midas-style, epithermal, low sulphidation gold-silver mineralization".1

Photos2 taken from a mineralized section included the one shown below showing an ample dollop of a mineral known as "naumannite," whose occurrence includes "in Nevada, large crystals in the Ken Snyder mine, Gold Circle district, Elko Co., and at the Rex Grande deposit, Midas, Elko Co."3. I'm taking 10% of the deal because of all of the reasons I gave in the article I wrote for Streetwise Reports entitled "Rebirth in Nevada for Gold Explorer"4. However, I am also stepping up because we have more than a few "grey-hairs" active both in the field and in the engine room. If you are an exploration company, share structure is critical not only in the exploration phase but more so in the development stage where, despite the discovery, costs escalate as the resource is defined and its economic viability is determined. We older guys recognize the importance of protecting the share structure because you KNOW that the most expensive period is "dressing her up for the ball" (sale). Stakeholder will have less than 30 million shares outstanding after this raise is completed, which gives it massive leverage in the event of a discovery. And, most importantly, this IS the Carlin Trend, elephant country of the highest order. Since the Midas Mine is a 2 million (+) ounce gold deposit, the fact that we have confirmed naumannite content in the first 400 feet of an 800-foot hole is enough for me to take the proverbial plunge.

*********

share

share

share

share

share