Breakout Of 35-Year Downward Yield Range Will Blow-Up Interest Rate Derivatives ($500 Trillion+)

Nothing makes sense anymore. The markets keep going up like it is going out of fashion Trump’s honeymoon period or not. Trump might be getting a strong cabinet around him and have good ideas to stimulate the economy…though you first have to spend money (increasing debt) before you make money, which takes time.

And the obvious question is how the expenditures and lower tax rates (15%) will be financed. Inevitably it will mean a further increase in the already high debt burden of nearly $20trn further straining the Debt/GDP ratio. Total US debt plus unfunded future liabilities is estimated at some $200trn+. We are a debt society. As indicated in my earlier article $10 of debt is needed to generate $1 in GDP growth showing the inefficiencies of our legacy systems. The 0.25% increase in Fed Funds Rate and a potentially 3 further interest rate hikes (complete nonsense!) for 2017 is further strengthening the already strong US dollar and blowing all other currencies out of the water which is a strong argument for gold, the best hedge against currency devaluations. Gold is by far the best preservation of purchasing power under the current circumstances and the pension funds should take notice if they want to have purchasing power left for their pensioners.

From November 8 the US dollar index has increased by 6% from 97 to 103 with the US dollar at 14-year highs. Over the same period the Euro has fallen by 9% from $1.13 to $1.04 whilst the Yen weakened by 13% from Y103 to Y117.

Following the December 16th devaluation and the Chinese seizing of the US underwater drone the offshore Yuan hit a fresh record low of Y6.96 against the Dollar. Since the "one-off" devaluation in Aug 2015, the Chinese currency has now weakened almost 14% against the dollar. And the chart shows that following the Trump effect more weakness is on the way not the least because of the rising debt/equity ratio, already at 250% for China, and the increasing amounts of money leaving the country in an accelerated fashion in anticipation of further Yuan weakness.

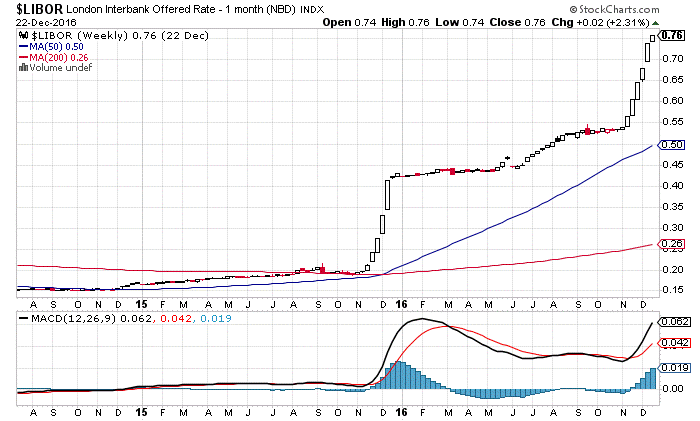

As a result of the stronger US dollar EM (Emerging Market) debt, which is mostly financed in US dollars, is getting more expensive by the day because more local currency has to be exchanged for the ever more expensive US dollars, now at 14 year highs. The increasing demand for dollars in order to pay off the loans and the US dollar loans not being rolled over has translated in a further tightening of the Eurodollar market, which constitutes of all dollars “held” outside the US, and shows in higher Libor (London Interbank official rate) rates.

Following the stronger dollar the yield on the EM debt is also increasing because the weaker exchange rate for the Emerging Market currencies increases the risk of repayment. Next to the negative impact on the EM debt the strong dollar is also increasing the foreign translation losses. Some 50% of all S&P companies profits stem from abroad. As a result profit growth forecast for 2017 will have to be adjusted downwards keeping everything the same. Another effect of the continuous and self-fulfilling feed of a stronger dollar following the rate hike and potential further hikes in 2017 is that investors swap their Japanese and Euro sovereign bonds for US treasuries triggering higher domestic interest rates. In other words the upward pressure on interest rates in the US has a lot of undesired effects perhaps the most important one the triggering of higher interest rates worldwide on total global debts of $220trn (up $70trn since 2008).

In my point of view the dollar strength is artificial because the lack of better alternatives except for gold and silver which are being purposely suppressed. Six-week retail sales up to December 5 are down 5% y.o.y. According to a research piece published by Cowen & Co. on December 14th, mall traffic fell 6.4% in November from October and December month-to-date traffic was down 9.9%. Next to that a new study by economists from Harvard and Princeton indicates that 94% of the 10 million new jobs created during the Obama era were temporary positions, they were part-time jobs or contract positions. In other words low quality jobs. The proportion of workers throughout the U.S., during the Obama era, who were working in these kinds of temporary jobs, increased from 10.7% of the population to 15.8%. Obama’s boastful pretended improvement in the number of people employed reducing the unemployment rate to “4.6%” shows he either lies or doesn’t know what he is talking about. Anyway my point is that the strength in the US dollar is not fundamental because of a strong economy but purely a function of “relative strength” and lies about economic statistics manufactured (manipulated) by the Government.

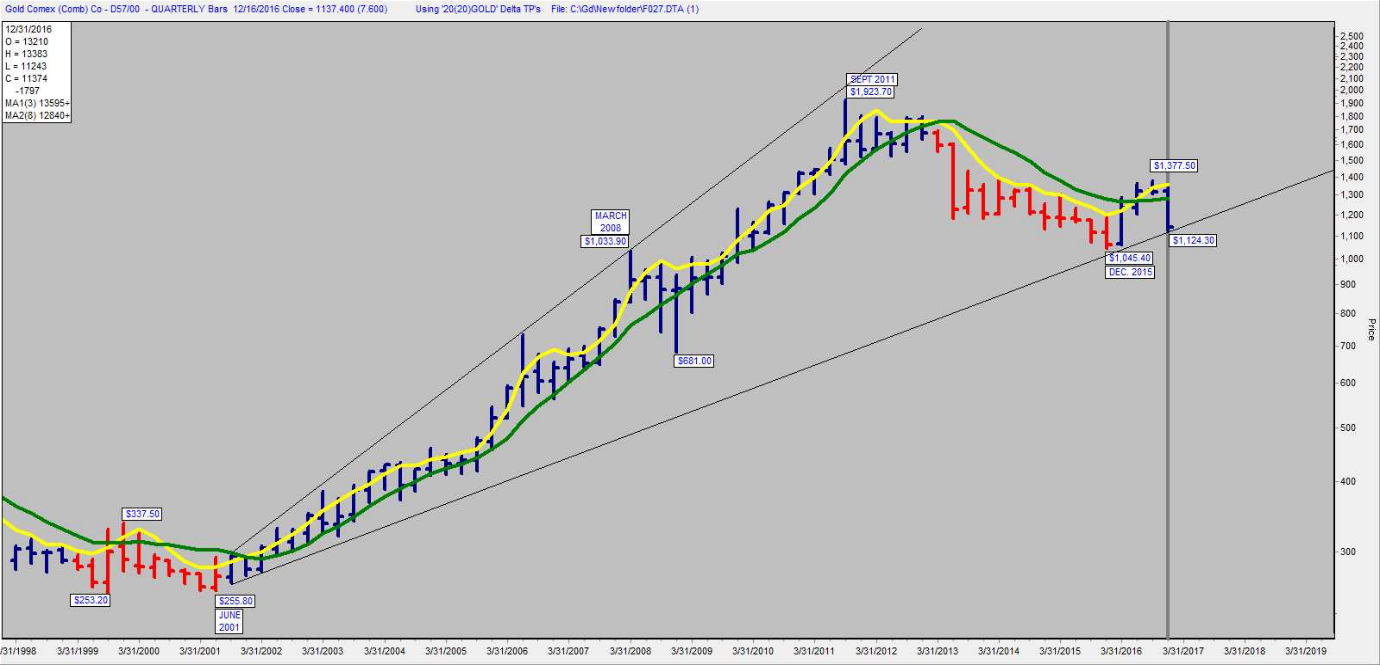

Gold and silver are THE only alternative to the US dollar though they, the central banks and BIS, consistently and methodically suppress the precious metals in order to give the US dollar the flawed upper hand. Though I believe that the quarterly chart for gold, as shown here below, is indicating that the correction since 2011 is nearing its end and that we can expect much higher gold and silver prices. Hey it has been tough but the rewards are coming.

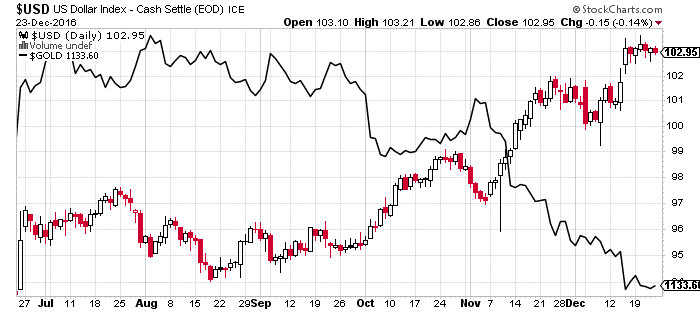

It should be emphasized that the “strongest” US dollar in 14 years also is an important reason why gold has been underperforming. Gold and the US dollar are inversely correlated see chart below. However the question really is if the gold price is weak because of the US dollar strength or because the manipulation by the central banks. Well looking at the fundamentals and the incredible high debt levels all over the world with China and Japan having debt/GDP ratios in excess of 250% and the US nearing the $20trn level I put my money on gold and silver.

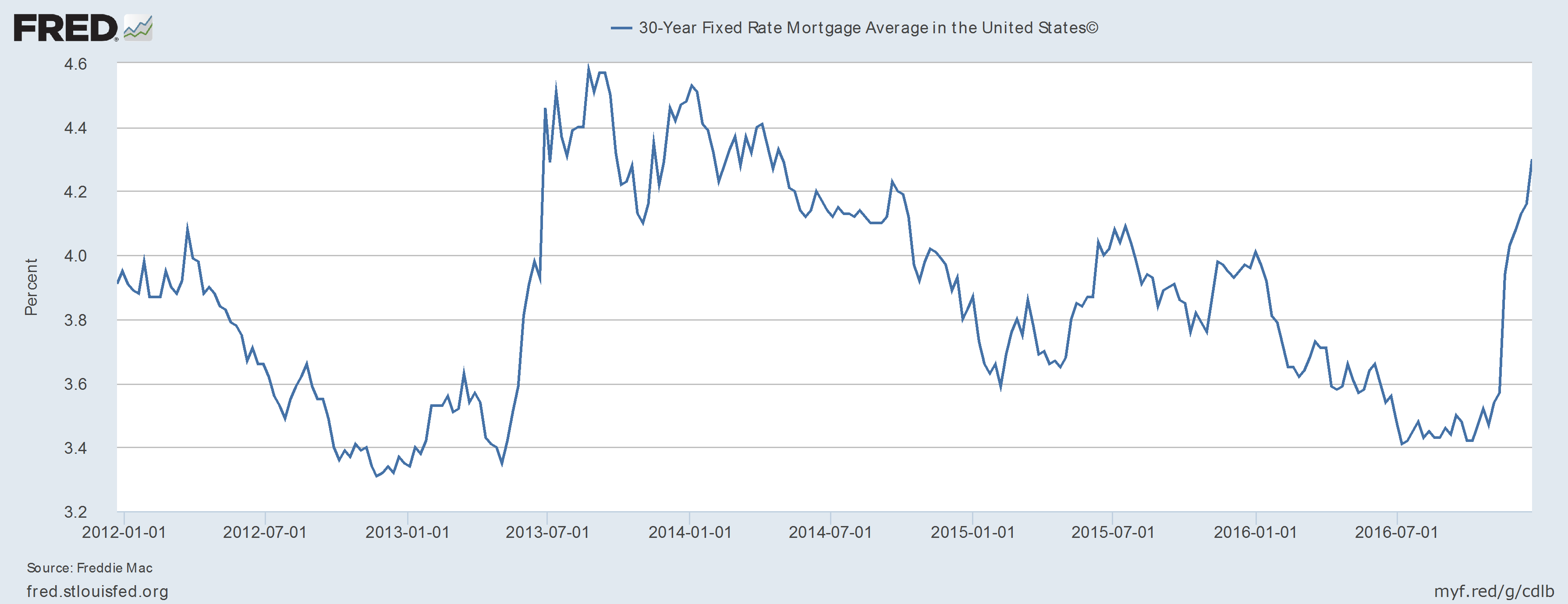

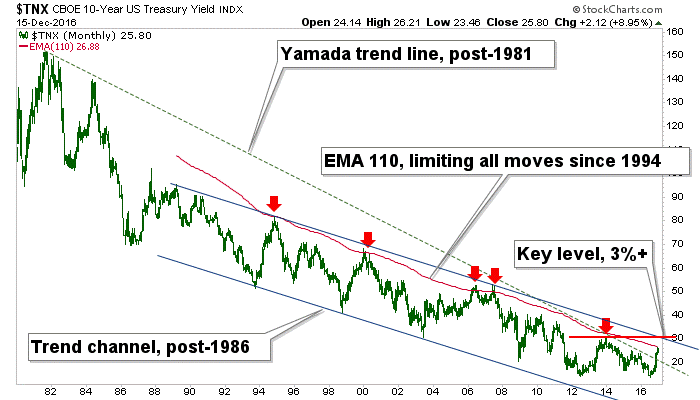

I believe that with the anticipated Trump initiatives for the US economy, the very fragmented inflation and the illiquidity in the bond markets (because regulations and Central Bank buying) the 3% break-out level is nearer than we might wish for. As eluded in earlier articles the 3% level represents the breakout level (see chart below) from the 35-year downward trend in the 10y treasury yield, since 1981, which will lead to very violent upward moves in the yields. Next to technical reasons as a result of new regulations market makers no longer keep inventory sincerely reducing liquidity in the treasury market and because they also don’t want to hold the bag at the other end I don’t exclude that the yield can quickly rise to 4%, 5% and even 6% when we break out. The low in the treasury yield was 1.36% July, and now it’s around 2.55% and it is not missing its impact on the real estate market that is starting to go off-line with 30y mortgage rates at 4.3%+. If you look at new home starts, they were down 19% in November month over month. There is no more refinancing market. As the housing market goes, so goes the economy and we know what happened last time. Housing values represent the soundness of the banks and the consumer confidence crucial for consumer spending.

Anyway the breakout theory is also confirmed by Louise Yamada, a renowned technical analyst who believes the 2.5% level is the crucial level. “The bull run is definitely over” after 10-year yields pierced 2.5%, said Yamada. She notes that a trend line has been broken; period. “Prices of bonds are going to go down and you are going to lose your capital,” said Yamada. I though still believe the major breaking point is the 3%. However if it is 2.5% or 3% the tone has been set.

As a result there will be a bloodbath in the bond market when we break out and because the markets are asymmetric there won’t be any rotation from bonds into equities but a similar sell-off in the equity markets because of the much higher rates making the equity markets PERs too expensive. Besides that I believe what will feed on the sell-off will be the rapid move in the interest rates which will unsettle the interest rates derivatives which are $500trn+ or $500,000bn+. Interest rate derivatives can’t be reset when the moves in the underlying interest rates are to steep over a short period of time. The $500trn+ in interest rate derivatives are amounts that are unimaginable to comprehend and these derivatives are the real nuclear instruments of financial destruction as also acknowledged by Buffett. Just imagine how far reaching the consequences will be.

The only asset class that currently is inversely correlated to the current peak bond and equity markets is the precious metals, gold and silver, because of the strong US dollar and the artificial suppression. And as we know gold and silver are the best hedges against devaluations of the currencies or otherwise said global purchasing power (the goods you can buy with the same amount of money (fiat or precious)). Just look up the gold price chart in Sterling, Mexican peso and Chinese Yuan since 2011. Because gold and silver are priced in all currencies a devaluation of a currency is reflected in a higher price for gold in the local devalued currency because the price in all other currencies stays the same. And since all world currencies are anchored to the reserve currency, the US dollar, the real rise in the gold and silver price will truly show itself when the US dollar loses its appeal or credibility. And when the yield for the 10y Treasury breaks out of the 35y range foreign investors will sell their bonds, which will weaken the US dollar. In fact one can argue that that process is already in place with the Chinese Russians and Saudi selling their US Treasuries and accelerating.

The continuous capital flight from China will further devalue the Yuan, which will ultimately help boosting the best currency hedge: physical gold and silver. Next to that do you believe people will continue to trust paper money in India after the abolishment of the R500 and R1,000 notes which is bankrupting the poor people in India?

Authorities in China halted trading on December 16th for the first time ever in futures contracts of government bonds, after prices had swooned, with the 10-year yield hitting 3.4%. Trading didn’t resume until after the People’s Bank of China injected $22 billion into the short-term money market financed by dumping treasuries. According to the US Treasury Department released Treasury International Capital (TIC) data for October, net “acquisitions” of treasury bonds & notes by “private” investors amounted to a negative $18.3 billion in October. And “official” foreign investors, which include central banks, dumped a net $45.3 billion in Treasury bonds and notes. Combined, they unloaded $63.5 billion in October. In September, these foreign entities had already dumped a record $76.6 billion.

Although there was also net selling of US Treasuries in 2012, 2013, and 2014 it never matched the same magnitude as in 2016. When the QE tapered, forcing higher LT interest rates, the selling pressure of treasuries picked up in 2015 with a sharp acceleration in 2016. And tighter credit conditions will also mean lower PE multiples for equities.

In general it is the ESF or Exchange stabilization Fund, part of the US treasury, that buys the treasuries preventing the interest rates from going through the roof. So far foreign central banks liquidated a record $375 billion in US government debt in the last 12 months. The total amount of custodial paper, these are the treasuries that are being held for foreign governments, has fallen to $2.805 trillion, the lowest since 2012.

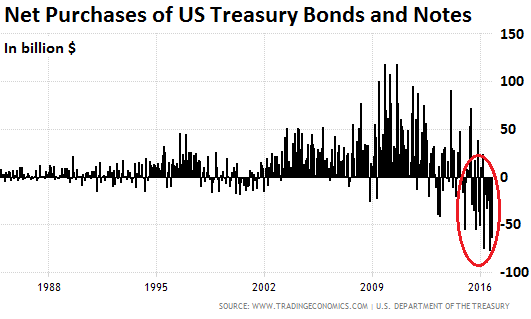

Going back to the early 1980s, the chart of net purchases of US treasuries bonds and notes just shows how this wholesale dumping (circled in red) of US Treasury bonds and notes by foreign entities started after 2009:

China, once the largest holder of US Treasuries, has now problems of its own with its banking and shadow banking system. Authorities have been busy trying to keep a lid on its own financial problems that are threatening to boil over. It’s trying to prop up the Yuan and to stem rampant capital flight whilst at the same time it’s trying to keep its asset bubbles, particularly in the property sector, from getting bigger and from imploding. And in doing so, it has been selling foreign exchange reserves.

According to the TIC data (market price adjusted), China was the largest seller in October, unloading $41 billion. Over the last six months, it unloaded $128 billion. This slashed its holdings of Treasury securities to $1.116 trillion, below the holdings of Japan. Japan, now the largest holder of Treasury securities, reduced its holdings by only $4.5 billion in October to $1.132 trillion. Japan and China are by far the largest two creditors of the US and they’re cutting back their lending.

Over the last 24 months, the US gross national debt has ballooned by $1.85 trillion, or by about $925 billion per 12-month period. Under Obama the government debt doubled, the biggest increase ever. On January 20, 2009, when he was sworn in, the debt was $10.626 trillion. Today it is almost $20 trillion. How irresponsible is that and how much has it tarnished the US monetary credibility!

This time, neither China nor Japan, nor any other major foreign entities may be willing and able to bail out the US, as they’ve done during and after the Financial Crisis, because they now have their own problems. The bond market sees this too. Hence, the bloodletting in Treasuries, once considered amongst the most conservative investments in the world. Though in my point of view RISK FREE is no longer RISK FREE!

The yield of the 10-year Treasury has nearly doubled since July 6 this year, when it reached a low of 1.36%, whilst settling at 2.55% on December 23, 2016. And as mentioned the selling into any strength in the 10y Treasuries doesn’t seem to be abating. And the closer the interest rate will come to the 3% break-out rate the more nervous holders of the Treasuries will become and be more incentivized they will become to sell their positions in order not to incur much larger losses.

The Modi abolition of the R500 and R1,000 notes enacted on December 9 had some well-timed “coincidence” with the Trump win. Modi reasoned it by fighting corruption, which was the biggest nonsense ever. He was clearly “instructed” by the BIS and other central banks to dampen or eradicate the seasonal buying of gold in India for the different festivals etc. This Modi, now prime minister of India, was a tea seller in an Indian train station, do you believe he could stand up to the “sophisticated” BIS people and central bankers and who knows what has been promised to him. Anyway it sounds that this plan is not working the way they had envisaged it to work out. Gold in India is now trading at a $300+ premium per ounce to LBMA and Comex prices. It will be a long time before the Indians, and especially the poorest people, will trust paper money again. And the reason we don’t see higher gold prices in London and New York yet is because India has closed off its gold market for the rest of the world invoking increased smuggling especially from Dubai. Though if this situation continues it will definitely impact London and New York prices.

At present the Shanghai Gold Exchange, which is a physical exchange, is showing $30+ premiums for gold prices following the continuous downward pressure on the Yuan. These gold premiums should be arbitraged hence push gold prices in London and New York up.

A last remark I want to make here is about Bitcoin. Last week Bitcoin prices climbed to as much as $918.95, a 17.7% gain since the start of the week. Bitcoin is a proxy for gold and silver, for the uncertainty in the markets, especially the currency markets. Bitcoin is an easy way to evade capital, banking and transport restrictions though ultimately it is a virtual digital currency and can’t compete with the real gold and silver. Though be aware everything that is digital can be hacked and ask yourself who is going to be willing to sell physical gold for a digital algorithm when the US dollar, still the anchor of the financial system, is failing. It is the same with the nominal settlement of the Comex options when people don’t accept any dollars anymore for the settlement of their futures but want to have the physical gold for the settlement of their contracts. Continuous much higher prices for Bitcoin kind of signifies what the outlook for gold prices could be. Anyway all the above situations should be increasingly favor gold and silver in increasingly difficult economic and monetary circumstances.

Conclusion

To recapitulate situations that will favor gold and silver. Inflationary U.S. and Chinese policies will result in speculative fund flows into gold. President-elect Donald Trump’s plans to cut taxes is estimated to add $7.2trn to the federal debt in the first decade and as much as $20.9 trillion by 2036, on top of the $20 trillion outstanding today. Even in the absence of such additional spending (Congress has never been able to implement a “revenue-neutral” tax cut in the modern era), the U.S. federal debt is still expected to increase over the next decade, driven by entitlement spending such as Social Security and Medicare/Medicaid. Next to that higher fiscal spending amid a “tight” labor market and rising wages invariably leads to higher inflation. Another form is the commodity inflation, fuelled by the low base effect (prices that have come down significantly - and then start rising again). We also witnessed commodity inflation in the 70’s, with two oil crises, it was a period of stagflation which propelled gold from $35/oz. to $850/oz.

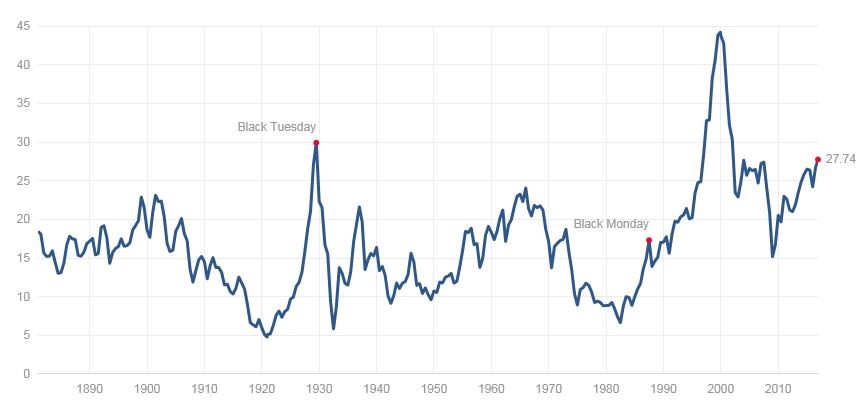

Trump is being compared to Reagan in terms of their no nonsense and pragmatic approach and that 2017 is like 1981. However, Reagan was elected after a recession. Interest rates were over 20% when he took office and indebtedness for the whole economy was only at Debt/GDP ratio of 32%, the federal debt held by the public was $1trn, according to CBO and the P/E for the stock market was 12x. Trump comes in with indebtedness at $20trn whilst the stock market is on 27x current earnings. "The cyclically adjusted P/E (CAPE), a valuation measure created by economist Robert Shiller now stands over 27 and has been exceeded only in the 1929 and 2000 mania see chart below. My point is that the starting position for the Trump presidency, despite all the right ideas he has, is very unfavorable and we first have to get back to earth before we can make headway in the economy. Too many tricks, unreliable statistics, manipulations have been used in order to keep the pretense up that the economy is doing well. Nothing is less true and this is something we first have to correct. And the bond market is most likely going to do the job for us see comments mentioned here above about the breakout of the 35-year downtrend in the 10y yields and the impact on the interest rates derivatives. The impact of a reset in the markets might be quite severe and take a long time to resolve the more because we are facing a global debt problem.

Shiller CAPE PE Ratio Chart

Source: Multpl.com

Ongoing fiscal stimulus and a surging housing market has led to significant credit creation in China with regulators now instituting policies to prick the Chinese housing bubble. Chinese speculators have been turning to the commodities market to hedge the depreciation in their Chinese Yuan-denominated assets. Over the past three months, zinc and copper prices, for example, have risen by 20% and 25%, respectively, driven by Chinese buying. In other words they hedged by investing in US dollar denominated commodities to escape the Yuan devaluations.

In the footsteps of this trend, gold futures turnover in China has risen to about 25% of that on the Chicago Mercantile Exchange, suggesting that precious metals pricing power is increasingly shifting to the East. China is a physical market settlement takes place in the form of physical delivery and is not a nominal or paper money settlement market like the Comex. And it is clear to me that the SGE, the Shanghai Gold Exchange, will set the future pricing of gold. Physical will win from paper it is just a matter of time.

According to the World Gold Council, global jewelry demand was down 21% year-over-year in the third quarter. This was driven by an unprecedented decline in jewelry demand in the world’s two largest markets, China and India (which collectively account for 60% of global jewelry demand), where jewelry consumption was down 27% and 41%, respectively, year-over-year. Jewelry demand is expected to hit a seven-year low in China, and a 13-year low in India. This year’s unprecedented weakness of the Chinese and Indian jewelry markets was due to a confluence of factors that will not have the same impact in 2017. These include: 1. A loss of Chinese consumer confidence; 2. Chinese gold import curbs designed to restrict capital flight; hence why Bitcoin is doing so well 3. A tax hike on Indian gold imports earlier this year; 4. Lastly a cash crisis in India as the country’s government outlawed the use of large-denomination notes. With the recent correction in gold prices and loss of trust in paper money and the devaluation of the currency, I expect both Chinese and Indian consumers to step up their gold and silver purchases in 2017.

I believe a lot of factors are coming together and that the bear trend that started in 2011 for gold and silver prices has ended…and that the secular bull market is about the resume with the breakout of the 35-Year downtrend of the 10-Year Treasury yield above 3% being the game changer.

Gijsbert Groenewegen ©