Gold And Silver Will Be Increasingly Bought As A Hedge Against The US Dollar And The Illiquidity In The Bond Markets. (Part 3)

So what is there left when you have sold your local currency in return for the “almighty” US dollar and the reserve currency fails? The ultimate currencies: gold and silver!

Gold and silver are the best preservers of your capital when other currencies fail, especially because you don’t have loss of purchasing power or loss of opportunity costs because interest rates are almost zero or negative. The question is when the dollar reverses its climb if investors will swap back towards their “local” currencies, the Euro, Yen, Swiss franc, Sterling, Kroner etc. I think that will only be the case if the economies of those countries have improved materially and thus their interest rates are rising which respectively makes their currencies more attractive. Considering the deflationary mindset that is taking hold everywhere, with everybody exporting their deflation by lowering the currencies, that seems very unlikely. As I have argued here before negative interest rates favor gold and silver above everything especially when the currencies are at stake. They function as the ultimate safety net in those situations.

Gold has a way of adjusting to inflation by automatically rising in price in order to match the same purchasing power. But because gold has been manipulated by several central banks for such a long time this mirror image of the reserve currency has not been allowed to show us its true value and function. Nominal money can’t move with inflation or deflation because it has a fixed nominal value written on the paper note, which only has a value of say $100 because the $100 is written on the paper and because it is underwritten by the Treasury otherwise there wouldn’t be any value to the piece of paper. That is different for gold, gold has its own inherent, real value. We all know that realistically interest rates, which give a compensation for the use, risk and re/devaluation of money, should be much and much higher though as a result of the ongoing orchestrated dilution of money (QEs) these interest rates are near zero or even negative. And because at these low interest rate levels the opportunity costs, the loss of potential gain, interest from deposits, when gold is chosen as in investment, are so low that gold should be priced much higher than it is today. Hence why we see that gold is performing very well in other currencies and especially measured in Euros (see chart below). The outperformance in US dollars will just be a matter of time when the default status of the US dollar, other currencies have been exchanged into, will have come to and end.

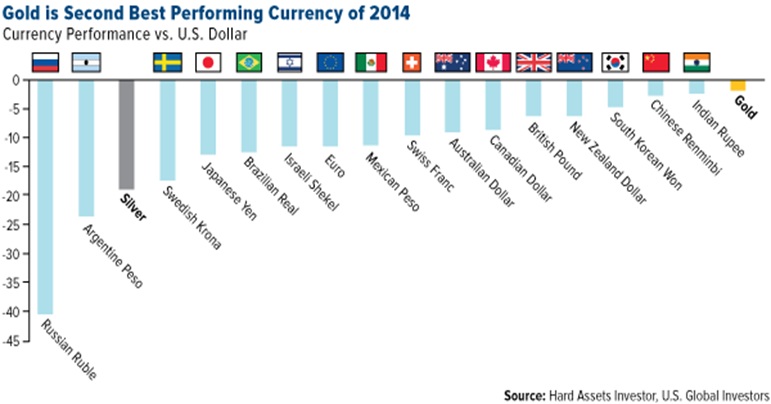

Despite the dollar strength investors have been buying gold, the best performing currency after the US dollar in 2014!

And to illustrate the abovementioned point despite all the extreme bearishness, following rising stock and bond markets, gold has actually been extraordinarily resilient in recent years given the dire circumstances. Amid its June 2013 low of $1,179 and April 15, 2015 gold price of $1,201, gold merely rose 1.9%. Yet over that same span, the S&P 500 and US Dollar Index exploded higher by 35% (2107: 1560) and 22.4% (98.56:80.50) respectively! Despite these increases there was still enough investment demand to support gold (notwithstanding the fact that gold is inversely correlated to the equity markets and the US Dollar) in all of 2014 with global gold investment demand amounting to 905 tons. And to top that off in 2014 gold was the best performing currency after the US dollar.

Since the beginning of the year the gold price measured in Euros has risen by 25% from 9 to 11.24 versus an increase of 1.4% for gold measured in US dollars from $1,185 to $1,201. Gold is outperforming in all currencies except against the US dollar! The moment the gold price measured in Euros closes above 11.50 followed by the 50 day moving average crossing the 200 day moving average the outlook for gold will look even better.

Anyway it is clear that investors have been buying gold as a hedge, an insurance policy despite the so-called strength in dollar. What is that telling you? That this buying of gold will continue especially when the uncertainties remain and QEs and low interest rates don’t have the desired effect despite peak equity and bond markets.

Eventually investment demand for gold should explode when the stock markets, the US economy and US dollar reverse lower, leading to far-higher gold prices in the coming years. Undeniably gold is the ultimate currency that only really comes in play when there are structural problems in the economies resulting in the debasement of the currencies. I can’t emphasize it enough but currencies are in the end the spill and the true reflection of the true state of the economies. Currencies are the real benchmark of your wealth. Remember if your currency becomes like the Zimbabwean dollar you don’t have anything! The overriding question is why gold and silver haven’t taken off yet. I will try to explain that in the following paragraphs!

A $2,000+ gold price was not conducive to reinstating “confidence” in the markets

Until now futures (paper) speculators or non-commercials have dominated gold action using naked futures in recent years scaring away many investors. Naked futures, versus futures backed by the physical, have been used by large speculators (the bullion banks) or non-commercials to stampede the gold price for obvious reasons: to secure the reserve status of the US dollar. Gold is the mirror image of the reserve currency and visa versa. When gold threatened to take the $2,000 level (the $1,921.50 high was achieved in September 2011) the authorities started to depress the gold price. Truly who can genuinely argue that equity and bond markets are improving and really reinstating confidence when the gold price is above $2,000? Next to that suddenly the Swiss franc, which tend to move in tandem with gold, was pegged (fixed, stuck, not moving freely any longer) to the Euro on September 6, 2011. When the Swiss franc was de-pegged gold jumped $33! And it is no coincidence that at the same time Switzerland has the most negative interest rates. Its currency has one of the highest correlations to gold so what I have been suggesting about currencies with strong negative interest rates and the link to gold clearly corresponds here.

We should wonder what other tricks the US Treasury has left up their sleeve besides the pegging of the Swiss franc, the QE in Japan and the QE in Europe in order to put downward pressure on the gold price in US dollars! Another QE, QE4, will most likely slaughter the US dollar.

Naked gold futures, without physical backing, have facilitated the downward pressure on gold prices despite strong physical demand

In order to make sure the gold price wouldn’t exceed the $2,000 level concerted actions of the bullion banks were administered to achieve this result. Because of futures’ inherent extreme leverage a relatively small amount of capital has a strong disproportionate impact on price action. Hence why the speculators (the bullion banks) were able to manipulate gold prices down using naked gold futures despite very strong physical demand from investors and countries such as China, India and Russia. Next to that the archaic intransparant dynamic between the exchange (regulated, transparent, standard contracts, settlement: trades are matched up and guaranteed by the exchange) and OTC (unregulated, intransparant, bilateral contracts, clearing and settlements of trades are still left to the buyer and seller) markets is still very opaque and definitely not helping a fair price setting. It should also be understood that it is assumed that the bullion banks make “unlawful” usage of their insight in where large investors have bought their positions and at which levels they have their possible stop loss orders. Front running?

Naked gold futures can be described as contracts that are sold without any underlying physical gold to deliver if the buyer on the other side decides to ask for delivery. Under normal circumstances investors will suffice with a cash settlement though as mentioned this will change and annul cash settlement when the reserve currency loses its attraction. The use of naked futures distorts the real price setting of the gold price because of the gearing and the fact that they are not backed by the physical gold. It is a paper game by the bullion banks and doesn’t have anything to do with the real price of gold because there is no physical gold backing up the contracts.

While investors usually buy gold outright, or at most run a 2x margin through gold-tracking ETFs like the flagship American SPDR Gold Shares (GLD), it takes far less capital to speculate on gold via futures. Each Comex gold-futures contract controls 100 ounces of gold, which was worth about $120k at a gold price of $1200/oz whilst the minimum margin requirement for that single contract is only $4k or a margin of 3.33% equal to a 30x leverage to the gold price! In other words a mere 3.3% move against a speculator position will wipe out 100% of their equity! Hence the sharp movements at peak short and long positions.

The gold price has a nearly perfect strong inverse correlation with speculators’ total (naked) gold-futures short positions.

Over time it has been demonstrated that the gold price has a nearly perfect strong inverse correlation with the large speculators’ total naked gold-futures short positions. And in recent weeks, these short positions surged to what’s very likely their third-highest spike in history indicating that a rally in the gold price is imminent. Gold bottoms near major shorting peaks without fail.

The game played by the speculators works as follows. As the short selling of the naked futures forces gold lower, some traders start to buy futures to cover their short futures position and realize their profits. The covering of short positions reverses gold higher, putting other speculators’ shorts at risk of rapidly becoming big losses. So they rush to cover too, sparking even more widespread buying to cover shorts. The more buying, the bigger and faster the potential losses, the quicker speculators exit. So once short covering starts from a major shorting peak, it tends to feed on itself and unfold rapidly. According to David Hamilton of Zealllc.com in the past an average short-covering gold rally lasted approximately 9 weeks and propelled gold on average 14%.

When the dollar tanks gold settlement will take place on the basis of the physical price setting annulling the paper or futures price setting

But think what will happen if a short-covering gold rally coincides with the lofty US stock markets and/or the parabolic US dollar finally rolling over, with the physical price setting of the gold price finally becoming the norm! When the US dollar tanks for reasons described in this article I don’t think investors want to have cash settlement for their futures contract they surely want to have the real thing: physical gold and silver (if you don’t have possession of the physical you don’t have anything but counter-party risk). And at that moment the physical price setting for the precious metals will takeover from the paper or futures price setting. That will be the moment, if not earlier, that finally the gold and silver prices will reflect their normal price setting not being manipulated by the bullion banks. Some of these factors need to be coinciding for the speculators to run for the hills. There will be a big resurgence in gold investment demand way beyond speculator short covering.

Anyway I believe we are setting up for some very exciting times in gold and silver though this might not be exactly the same for the markets and the societies we are living in. It might actually be some foreboding of some very difficult times of much needed “creative destruction”, a reset, a change of the DNA of our societies. It is like the “French Revolution” which corrected the excesses and corruption of the French society.

Stanley Druckenmiller (who has an impressive track record): "I know it's tempting to invest, but this will end very badly.

Stanley Druckenmiller: "Horrific sense" of deja vu: "I know it's tempting to invest, but this will end very badly. In 2006 and 2007, which I think most of us would agree was not a down period in terms of speculation; corporations issued $700bn in debt over that two-year period. In 2013 and 2014 they've already issued $1.1trn in debt, 50% more than they did in the '06, '07 period over the same time period. But more disturbing to me if you look at the debt that is being issued back in '06, '07, 28% of that debt was B rated. Today 71% of the debt that's been issued in the last two years is B rated. So, not only have we issued a lot more debt, we're doing so at much less standards. Another way to look at that is if those in the audience who know what covenant-light loans are, which is loans without a lot of stuff tied around you, back in '06, '07 less than 20% of the debt was issued cov-light. Now that number is over 60%. So, that's one sign”.

“The other sign I would say is in corporate behavior, just behavior itself. So, let's look at the current earnings of corporate America. Last year they earned $1.1trn; $1.4trn in depreciation. Now, that's about $2.5trn in operating cash flow. They spent $1.7trn on business and capital equipment and another $700bn on dividends. So, virtually all of their operating cash flow has gone to business spending and dividends, which is okay. I'm onboard with that.

But then they increase their debt $600bn. How did that happen if they didn't have negative cash flow? Because they went out and bought $567bn worth of stock back with debt, by issuing debt. So, what's happening is their book value is staying virtually the same, but their debt is going like this”.

Anyway do we need any more confirmation from someone with a track record like that of Stanley Druckenmiller to have an inkling that something is seriously wrong? Go figure. By the way the US companies seem to exceed 1Q15 estimates again! Mind the word estimates. It is a travesty, analysts lower estimates (to make sure they get the corporates business) so that the companies can exceed them and the management announces buy back programs in order to “meet” estimates and stock option programs for the management at the cost of a deteriorating debt/equity ratios. Basically they are using and deteriorating the shareholders capital to satisfy their own remuneration schemes, a better expression is fraudulent schemes. It is unbelievable what these people get away with.

To confirm the uneasiness Bloomberg just reported, "one measure of Treasury dealers’ trading activity has fallen closer to its financial-crisis levels”

Bloomberg reports, "One measure of Treasury dealers’ trading activity has fallen closer to its financial-crisis levels”. Deutsche Bank AG’s index that gauges liquidity by comparing the three-month average size of dealer trades against moves in the 10-year note’s yield fell to about 25 in February. It was above 500 in 2005, and reached as low as 19 in 2009 during the depths of the financial crisis." The increasing scarcity and disappearance of money-good assets ("safe" or otherwise) which is due to the way "modern" finance is structured, where a set universe of assets forms what is known as "high-quality collateral" backstopping trillions of rehypothecated shadow liabilities all of which have negligible margin requirements (and thus provide virtually unlimited leverage) until times turn rough and there is a scramble for collateral, has become perhaps the most critical, and missing, lynchpin of financial stability. It is especially these underlying intransparant liabilities that will create havoc because nobody really knows what the exposures and the ripple effects are.

The direction of the dollar will show the way. The strengthening of the dollar though is a strengthening by default (by lack of alternatives) and an indication of how uncertain and vulnerable (illiquidity) all markets are

Since currencies no longer pay interest because they are manipulated, whilst they should in order to pay for their ongoing devaluation (QE), they are no store of value any longer. The strength in the dollar is not only a fake strength by default (by lack of alternatives) but also an indication of how uncertain and vulnerable other markets are. People don’t know better and thus go for the US dollar also because they haven’t come around the concept of gold and silver yet. There is no inherent value to paper and especially when the nominal amount printed on it is being rapidly diluted away! And I strongly believe that the longer this nonsense will go on the more investors will buy the insurance against the ongoing erosion of paper money: gold and silver. More and more people finally get the sense that there is something wrong in the markets and would like to have a REAL (tangible) insurance in case things don’t map out the way the government wants us to believe. Believe and reality are two completely different things.

Next to that one should take into consideration that interest rates just simply can’t be increased because the debt structure would implode in other words there would be hardly any opportunity costs holding gold and silver. If anything it will be the opposite. Do you see the silver lining?

Related Articles

© Gijsbert Groenewegen