Gold And Silver Will Be Increasingly Bought As A Hedge Against The US Dollar And The Illiquidity In The Bond Markets (Part 2)

share

share

share

share

share

share

share

share

share

share

The lack of risk free paper also shows itself in Germany following a budget surplus

The lack of available risk-free paper was further accentuated by the fact that Germany's public sector posted a total budget surplus in 2014 of €6.4bn ($6.95 billion), helped by strong tax revenues in a recovering economy, compared with a deficit of €7.2bn the previous year. In other words, not only a balanced budget - which Germany achieved for the first time in half a century last year - but a surplus which means no need for debt issuance, especially when the debt carries negative rates. And since the ECB has no choice but to monetize about €11bn per month in German debt, it means that German net issuance is now solidly negative. This also means that the ECB it will soon have no choice but to taper its QE program, long before its scheduled expiration in the fall of 2016. That would basically mean that they have come to the end of the road!

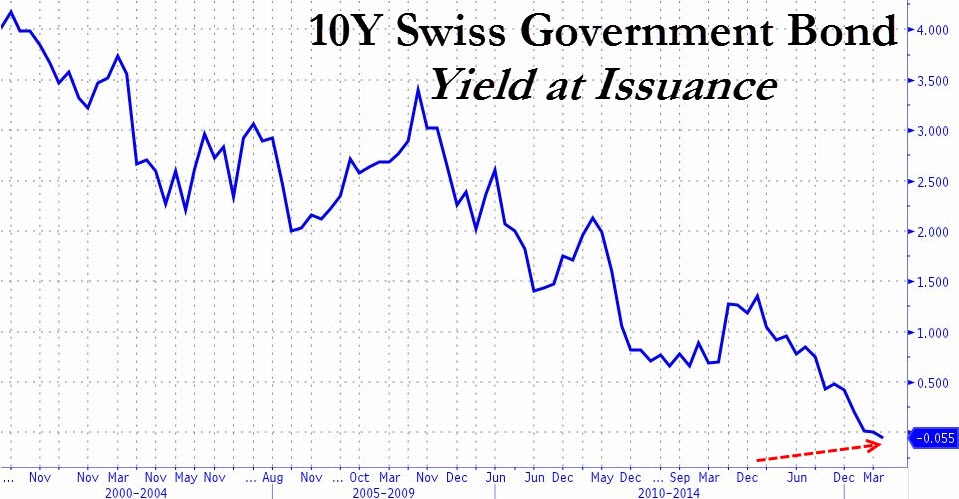

Swiss government becomes first ever to issue 10Y debt at a negative yield. Do you think investors like the Swiss franc?

The Swiss government has become the first ever to issue a 10Y sovereign bond at a negative yield. As the WSJ notes, while several European countries have sold government debt at negative yields up to five years of maturity - which means investors effectively pay for the privilege of buying it - no other country has previously stretched this out as long as 10 years. Investors clearly like the Swiss franc! Though what does this in general tell you about the value of your money, deflation or the fear of continued erosion of the purchasing power of the less important currencies?

Central banks are destroying their own creation, money, in order to try and kick start their economies!

On the 10-year slice, the Swiss yield was -0.055%, compared with 0.011% on its most recent similar bond two months ago. In the post-issuance secondary market, Swiss bonds maturing up to 11 years in the future already trade with yields under 0%. But such low yields at the initial point of sale “illustrate well the world we live in,” said Jan von Gerich, chief strategist at Nordea, referring to collapsing yields on debt amid widespread stimulus from central banks around the world.

The central banks are destroying their own creation, money, in a desperate attempt to try and kick start their economies! And no real structural changes (budget deficits) are being undertaken in order to deal with fundamental problems we are witnessing in our societies.

See the correlation between currencies with strong negative interest rates and the “opportunity income” for gold and silver

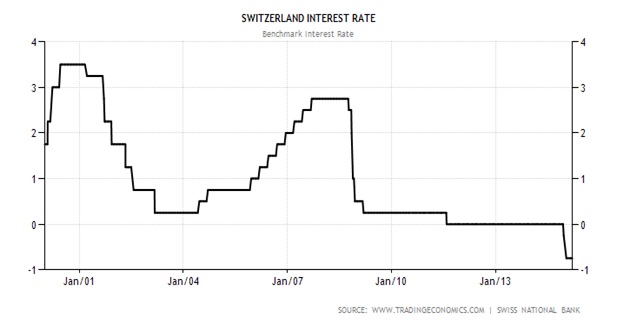

The Swiss and the Danes are trying to weaken their currencies with negative interest rates in order not to outprice their exports but in the end will probably attract even more buyers for their currencies because investors like the way they run their economies (that is in the first place why a currency is fundamentally strong or weak) compared to other countries and are therefore willing to pay a price to ensure that their purchasing power, expressed in a strong currency, is secured, even if it is for a period of 10 years. The longer out the negative interest rates the more desirable a certain currency, government bond, seems to be. The race for competitive currency devaluations is now being replaced by the chase for the currency that will best keep its future value (purchasing power) and those are the currencies that have the most negative interest rates. They are like balls that you try to keep underwater, at one stage they will bounce back with huge ferocity because of the upward force from the water.

And the more negative the interest rates are the more there is an argument to buy gold and silver, the ultimate currencies, because there are no opportunity costs holding the precious metals any longer because there is no lost interest with negative interest rates. If anything negative interest rates now carry “negative” opportunity costs for gold and silver or differently said “opportunity income”! It is like backwardation for gold and silver prices whereby spot delivery is more expensive than future delivery!! And therefore in this context Yellen’s recent quote is the more remarkable if one thinks about it.

Yellen: "Cash is not a very convenient store of value"

“We must be reasonably confident at the time of the first rate increase that inflation will move up over time to our 2% objective, and that such an action will not impede continued solid growth in employment and output”. Next to that Yellen commented in the Q&A session on March 18, that "It is really interesting to see these European countries moved to negative interest rates. And in a way I am surprised that there hasn’t been more pick-up in the demand for cash. Cash is not a very convenient store of value but at a minus 0.75% interest rate I would have thought that maybe there would be some moving around".

It sounds as if she's surprised there hasn't been a larger pickup in demand for cash in the Eurozone areas where interest rates are negative. Physical cash acts as a store of value (or potentially even rises in value if the area is experiencing deflation) when interest rates are negative because the nominal amount you own doesn't change, where as if you hold a deposit in a bank account you may be charged a negative rate of 0.75%. As we know negative rates are imposed in order to deter foreign buyers of the currency or in order to prevent saving i.e encourage consumption.

This brings up real interest rates. The real interest rate is the rate of interest or net reward an investor expects to receive after allowing for inflation. It can be described more formally by the Fisher equation, which states that the real interest rate is approximately the nominal interest rate minus the inflation rate.

When an economy is struggling, it is standard practice for a central bank to cut interest rates. That makes saving less attractive and borrowing more attractive, boosting the amount of money being spent and kick starting an economic recovery. That is under “normal” circumstances though we don’t live under normal circumstances. In fact very low inflation can make a central bank's life harder. As we know many big economies are now experiencing “deflation” characterized by falling prices resulting from more supply than demand. In the Eurozone, for instance, the main interest rate is at 0.05% but the "real" (or adjusted for inflation) interest rate is considerably higher, at 0.65%, because Euro-area inflation has dropped into negative territory at -0.6%.

If deflation gets worse, assuming the main interest rate stays the same, then real interest rates will rise even more, incentivizing deposit holders to not spend their money, choking off recovery rather than giving it a lift. Desperate to avoid this trap, ever more European central bankers have waded into the unfamiliar territory of increased negative interest rates.

Consumers might well respond to negative rates by withdrawing money from banks and stuffing it in their mattresses or buying gold (is now “cheaper” than loaning money to the government). Why the hell would you keep your money at a bank that gives you back less as if banks are not already stealing enough of your money! The resulting shortage of loanable funds would push interest rates up. Hello fractional banking system! Though at present central banks are still betting that savers won’t run for the hills—after all, storing money is costly and risky. But negative rates may create financial instability in other ways. Banks may be reluctant to pass negative rates on to depositors for fear that they lose customers to other financial institutions (or the mattress or gold and silver) and because they have assets, like mortgages, with interest payments contractually linked to the interest rate. For institutions in that position, negative rates would lead to lower profits and, eventually, to erosion of capital.

And again if we look at the bigger picture what are we all doing is debasing and destroying all our currencies and economies. Next to that the accompanying liquidity issues in the secondary bond markets resemble a clear expression of failure of monetary policy: the encouragement of risk-taking in credit markets to drive borrowing and spur investment in economic projects is clearly not working and won’t work. A deflationary mindset in combination with poor job opportunities and a poor pension outlook (since the financial crisis in 2008, US savers alone have lost roughly $470bn in interest income net of lower debt costs (to the banking system) according to a report by Swiss Re) is not helping. We saw the Nikkei above 20,000 on March 10 and the Dax increasing by almost 25% since the beginning of the year though the illiquidity in the bond markets is telling us something else. There is no real confidence its all inflated, artificial confidence that will last as long as the music keeps on playing. And when the music stops there will be no bids but a deep black hole. As I have mentioned here above how much more evidence do investors need? Don’t you think it is time to structurally change things instead of bandage things?

The weak employment figures in the US clearly illustrate that things are not working as planned.

Despite the abysmal jobs report for March, reported on Friday, April 3rd, 2015 the US dollar strengthened quite substantially last week following bullish comments of Jeffrey Lacker. The case for the Federal Reserve to raise U.S. interest rates in June remains "strong," according to Richmond Fed President Jeffrey Lacker, who has long called for a prompt tightening of monetary policy, repeated his views that consumer spending, the labor market and other economic conditions have improved significantly over the last year. “Unless incoming economic reports diverge substantially from projections, the case for raising rates will remain strong at the June meeting," Lacker said on Friday April 10th.

The Bureau of Labor Statistics (BLS) reported that non-farm payrolls rose 126,000 in March. However, the number is much worse, since 72,000 of these reported 126,000 new jobs were a guess according to the birth/death model from the BLS of new jobs they hope were created by new businesses in the month of March. This means that actual new jobs were only 54,000!! This is about a third of what the economy needs to create to breakeven with population growth. This is evidence of a shrinking employment picture. It is fuel for the Fed to hold off raising short-term interest rates, probably moving back the targeted time to September 2015 from June 2015.

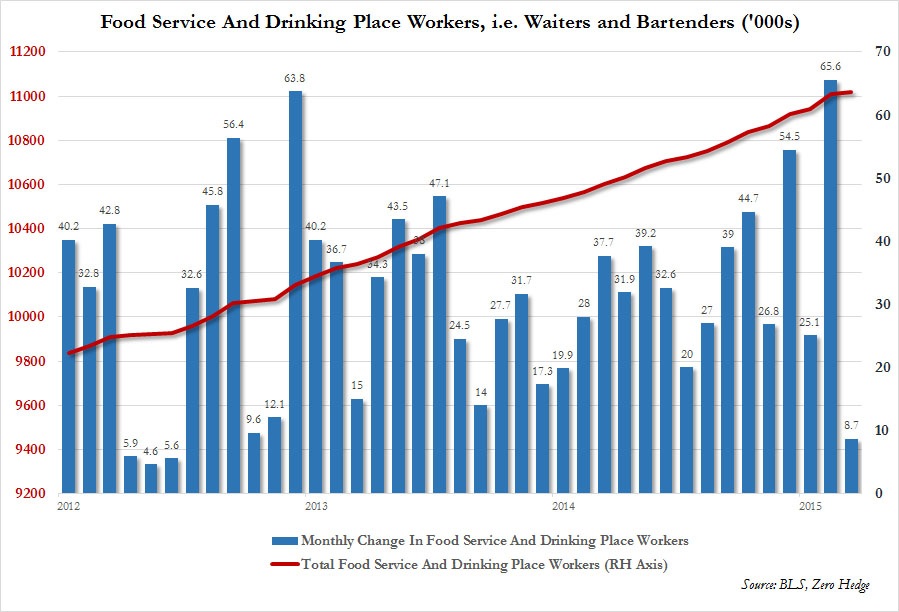

What recently propelled employment figures were the low paid jobs such as bartenders and waiters. Though the March number of "Food Services and Drinking Places" workers, aka waiters and bartenders just saw its worst monthly increase since June of 2012. So much for the "waiter and bartender" recovery so heavily praised by the WSJ a month ago.

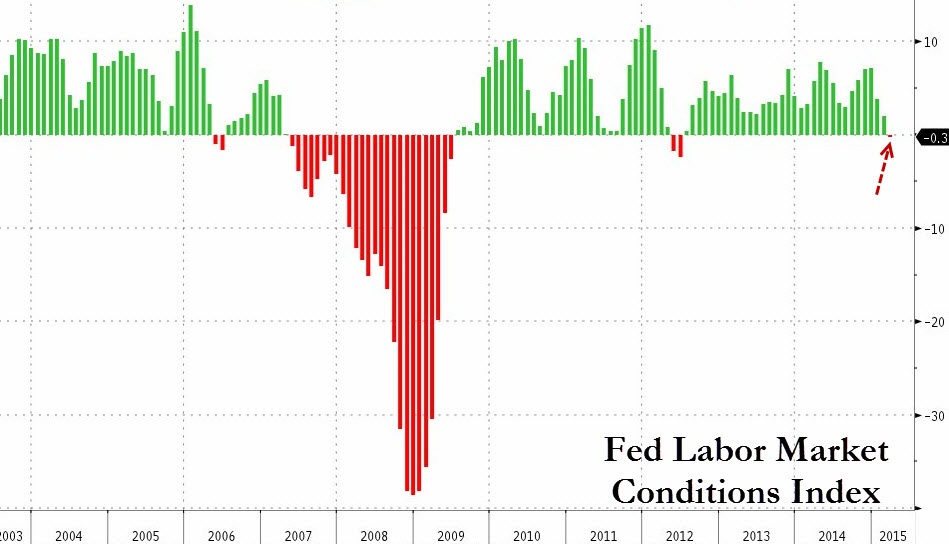

It should be noted that most of the “new” jobs in the job reports of the last couple of months have been low paid, part-time (counted as full-time jobs!!) and filled by 55-year and older people! Poor quality to say it at the least. Four of the five most active job categories hiring in March were also the lowest paid: Education and Health saw the addition of 38K workers, Retail Trade added 26K, Leisure and Hospitality added another 13K and Temp workers increased by 11K. And these abysmal conditions were confirmed on Monday April 6th by the Fed Labor Market Conditions Index (the aggregate index of all Yellen's indicators) that collapsed to its lowest level in almost 3 years.

The weak economy readings were confirmed by the Credit Managers Index (CMI) for the month of March, which stands at levels not seen since 2008

Confirming my view is the Credit Managers Index (CMI) report for the month of March which "deteriorated significantly over the last two months and current readings stand at the recessionary levels not seen since 2008. The most drastic fall took place with the unfavorable factors that indicate the real distress in the credit market. It has tumbled from 50.5 to 48.5 and that is firmly in the contraction zone—a place this index has not been since the days right after the recession formally ended. The signal this sends is that many companies are not nearly as healthy as it has been assumed and that there is considerably less resilience in the business sector than assumed. By far the most disturbing is the rejection of credit applications as this has fallen from an already weak 48.1 to 42.9. This is credit crunch territory—unseen since the very start of the recession. This can be seen on the chart below. Suddenly it seems companies are having a very hard time getting credit! Not a good sign.

The accounts placed for collection reading slipped below 50 with a fall from 50.8 to 49.8 and that suggests that many companies are beyond slow pay and are faltering badly. The disputes category improved very slightly from 48.8 to 49, but is still below 50. This indicates that more companies are in such distress they are not bothering to dispute; they are just trying to survive. There are big, big problems as far as the financial security of these companies are concerned.

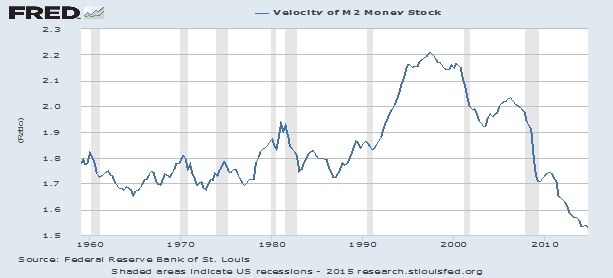

The rejections of credit applications fell strongly below the 50s going from 50.3 to 43.8! There is most definitely a credit crunch underway stemming from access to credit similar to the situation that existed at the start of the recession in 2008. The overall economy didn’t look all that bad in late 2008, except that there was a dearth of credit and that soon led to business failures and struggles. And see where the velocity of money stands now compared to 2008!

And despite all this negative news it looks like the Fed members are eager to increase interest rates on the basis of so called “strength” in the economy. St. Louis Fed President James Bullard a leading hawk on the Federal Reserve on Wednesday April 15 made a case for raising interest rates soon, arguing the level needs to be appropriate for the coming “boom” for the U.S. economy. My comment: “Yes the economy is so strong that we need continuous liquidity infusions (QEs) and manipulation of the markets to keep them up and next to that the markets are so healthy and confident that the liquidity is completely drying up in the secondary bond markets. Am I missing something?” Next to that he apparently said: Cut rates if the economy suffers a shock after Fed liftoff. What do you think that will do to the dollar? How much credibility do you want to give these …………..?

Anyway based on the above unemployment and CMI figures I don’t believe that the US economy shows any real strength justifying a rate hike. I think that the economy is so weak that when the Fed increases interest rates, as suggested by Bullard, the economy will implode and that the Fed will have to launch QE4. This will most likely reverse the strong run up we have seen in the US dollar since July 2014 and at the same time propel gold and silver.

© Gijsbert Groenewegen

Courtesy of www.groenewegenreport.com

share

share

share

share

share

More from Gold-Eagle