Gold Breaks The Ice As Buyers Roll The Dice

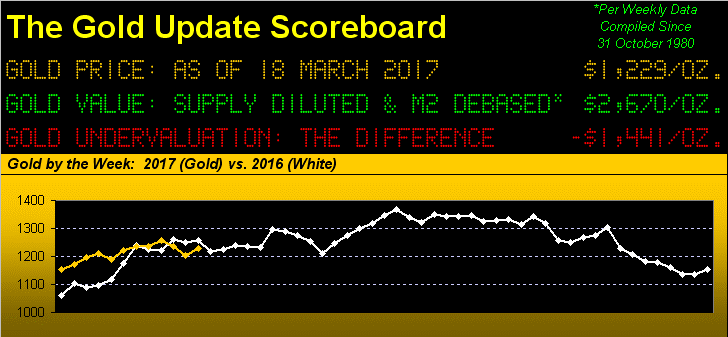

The Federal Open Market Committee's policy statement released this past Wednesday, despite its confirming the raise of the FedFunds target range to 0.75%-1.00%, was couched as "dovish". We read the statement -- twice -- and didn't find anything about it that was "dovish"; rather, primarily hawkish to neutral at minimum, but not "dovish". Yet given the way news is thrown together these days, it must have been "dovish" because Gold, (as did everything else save for the Dollar), instantly soared -- the yellow metal itself some 13 points in less than 60 seconds -- on the announcement, ahead of Chair Yellen's "thrice we'll raise the interest price" (and exacerbate the negative real rate) press conference. That commentary some 30 minutes later led to Gold's making up even further ground, as we can see in the above panel at least toward where price was at this time a year ago, settling the week yesterday (Friday) at 1229. And in a week's time, price may well cross above last year's white line.

Regardless, Gold buyers rolled the dice in pressing their buy buttons precisely on the policy's 2:00pm ET release. The FOMC's announcement might have been anything from a biblical psalm to a chapter from "Tom Sawyer", given such soaring of Gold at the millisecond the statement was released, (i.e. no one actually had time to read, let alone digest, it). Rather, "they" (and their algorithms) just instantly, dare we say blindly, bought. "We'll actually read it later and then worry about it", which oft results in post-Fed whiplashes. But it makes for believable news to justify soaring Gold by guessing the Fed must be "dovish". Still to us, the statement was (for once) quite rightly in line with our Economic Barometer, which now post-FOMC continues of its own accord to soar. Here 'tis, bearing in mind that the Fed has the right to change its own mind at any time ... oh yes, 'tis happened before, even between scheduled FOMC meetings:

'Course, a fear fostered by FedHikes is the fouling of the stock market. Yet from our "What, Me Worry? Dept." regular readers by now well know that from 30 June 2004 through 29 June 2006 the FOMC nicked its FedFunds rate up 17 consecutive times over those two years from 1.00% to 5.25%, (i.e. some eight rate hikes per year). Yet in the same time frame, the S&P 500 rose 11.6% from 1141 to 1273 and the price of Gold 49.8% from 393 to 589. What's different this time 'round is that the price/earnings ratio of the S&P, (then an average of 19x) is today by our "live" reading 34x, whilst the price of Gold today (1229) given money supply debasement "ought be" 2670. Put that definition for "out-of-balance" in yer Funkin' Wagnalls.

Still, as fundamentally depressed as we've found Gold in recent years, it nonetheless is technically suffering the demons therein. Price this past week having come within a whisker's breadth of seeing the weekly parabolic trend flip to Short, we doff our cap the Fed Chair for letting Gold instead run higher only to now find itself en route toward again encountering the ever-annoying 1240-1280 resistance zone. Trapped betwixt the rising parabolic Long dots and overhead resistance, the drama mounts: "We shan't stay in Kansas forever, Toto..." Here are the weekly bars:

The good news which continues is seen in Gold's broader picture, price on balance basing for better than a year now, indeed with an upside bent, and the 300-day moving average in ascent as shown here:

Remember: last year's run precisely up to Base Camp 1377 was an intra-year move of +29.8%, an historically outlying event which failed to hold up. To now see Gold more methodically work its way back up to 1377 would better reinforce an underlying foundation of support toward opening the door to the 1400s, (and the bottom of "The "Floor" at 1466). As for "The When", until Gold puts the 1240-1280 resistance zone behind itself once and for all -- which last year had appeared to have been the case -- one can only watch ... but not be without ... for as you know when Gold goes, it GOES (!)

As for how it has been going, let's next go to Gold's "Baby Blues" and the 10-day Market Profile. And on the left across Gold's three months of daily bars, the baby blue dots of 21-day linear regression trend consistency continue their decline for which we declared a week ago that -- "no" -- price's fall had yet to stall; yet it did in Chair Yellen's racing to Gold's rescue. That said, if from mid-chart Gold is now forming a "head-and-shoulders" pattern by which this Fed Fête becomes but a weak right shoulder, then we ought expect price to revisit the 1204 supporter as shown in the Profile on the right:

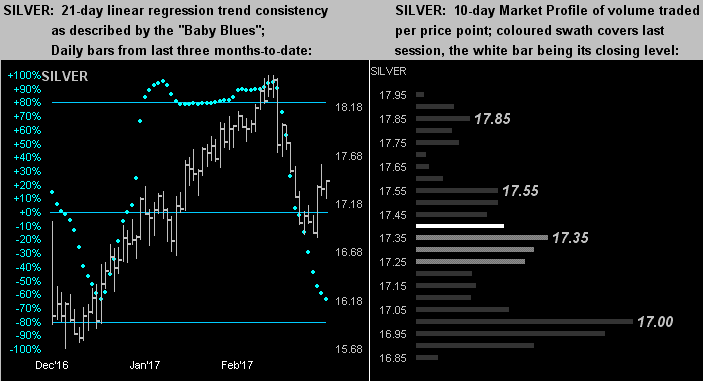

Similarly for Sister Silver, with her Baby Blues continuing to lose, should her post-Fed shine turn back to decline, 'twould be the sellers rolling the dice down toward the Profile's 17.00 support level:

So to put all this pricing into perspective here we have...

The Gold Stack

Gold's Value per Dollar Debasement, (from our opening "Scoreboard"): 2670

Gold’s All-Time High: 1923 (06 September 2011)

The Gateway to 2000: 1900+

Gold’s All-Time Closing High: 1900 (22 August 2011)

The Final Frontier: 1800-1900

The Northern Front: 1750-1800

On Maneuvers: 1579-1750

The Floor: 1466-1579

Le Sous-sol: Sub-1466

Base Camp: 1377

Neverland: The Whiny 1290s

Resistance Zone: up to 1280 (from 1240)

2017's High: 1264 (27 February)

Trading Resistance: none

The 300-Day Moving Average: 1247 and rising

Gold Currently: 1229, (expected daily trading range ["EDTR"]: 13 points)

Trading Support: 1218 / 1204

10-Session “volume-weighted” average price magnet: 1213

10-Session directional range: down to 1195 (from 1237 = -42 points or -3%

The Weekly Parabolic Price to flip Short: 1195

2017's Low: 1147 (03 January)

Finally, these few observations:

■ March-to-date in Minneapolis, quite normally, is a bit frigid up there, the low through this month's first 16 days having averaged -7°C (19°F). To the extent this may have led to brain freeze we've haven't the foggiest notion, other than to note that Federal Reserve Bank of Minneapolis President Neel Kashkari on Wednesday solely voted against the FOMC's action to raise the Fed Funds rate. If someone has a moment, please forward to him our Econ Baro, (along with a nice Nordic ski cap).

■ Our colleagues in the media are finally coming 'round to an effect we've been pointing out for better than a year: that banks passing FedHikes onto their customers means higher interest costs on new and existing variable rate debt. Can you imagine working the phones at some credit card help desk? "Hullo? It says my minimum and interest went up? What did I do?" You accepted the terms, blockhead.

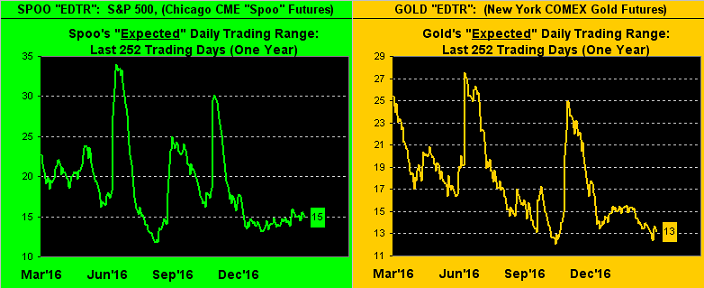

■ CNBC ran a piece yesterday pointing to how narrow the daily trading range of the stock market has become. We confirmed such by looking at our website's Market Ranges page, which specific to the S&P futures (below left) shows the EDTR ("expected daily trading range") as follows from a year ago-to-date at a rather lowly 15 points, as 'tis the case for Gold (below right) at just 13 points. Looks in both instances like we're due for "sumpthin' to happen":

"What does that tell you, mmb?"

Squire, it brings to mind of one the quintessential logicities uttered by the iconic Inspecteur Clouseau whilst resuscitating the mad man Dreyfus: "Out with the bad air, in with the good." Or for our purposes: "Out with the stock market, in with the Gold!"

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.

More from Gold-Eagle