Gold Revisits The Year's High; S&P500 Goes Bye-Bye

share

share

share

share

share

share

share

share

share

share

■ Whether driven by NorKNoise, or just plain ole common sense, Gold further reinforced its recent firmness in all but tapping the year-to-date high (1298.8 on 06 June), reaching up to 1298.1 yesterday (Friday) before settling out the week at 1295.0.

■ Whether driven by NorKNoise, or just plain ole common sense, the stock market finally responded to its recent technical weakness, the S&P 500 giving back six days of record high closes (from 14 July through 07 August) in a single session this past Thursday, settling out the week at 2441.

In the eyes of the pure technician, these two markets would have performed just as they did, NorKNoise or not. Our being more of a "fundatechnilist", the NorKNoise was a catalyst to propel both gold and the S&P in their proper, long overdue directions. To wit our response to a reader who wrote in regarding our take that gold ought rise and the S&P fall:

"Stocks cannot maintain exorbitantly high and increasing p/e ratios in perpetuity, even were interest rates to remain flat. Investors’ capital gains are now so terrifically high from these recent years that at some point common sense shall kick in, at which point, selling will further beget selling as the crash unfolds. But even should selling in stocks not immediately nor even over many months begin to occur, gold right now ought be at least double what it is, regardless of the stock market’s level or direction. That’s the key point. Gold does not need stocks to fall for its own price to rise. The realization oold being as undervalued as it is needs to spread across the investing spectrum, such that when it does start to ascend at a more material pace, investors without will begin piling on so as not to miss the up run to 2000 and beyond."

With respect to stocks and but a week to run in Q2 Earnings Season given 427 of the S&P 500 companies having reported, only 210 of them -- that's 49% -- have bettered their bottom lines from the like period a year ago. 'Tis why our "live" price/earnings ratio for the S&P remains an insane 42.1x. No, you shan't find that in the news as no one takes the time to do the work: all we hear there is the parroting of one another over this and that "beating estimates". Further, 'tis a reasonable bet the top is in when you see headlines such as Bloomy's "Americans 401(k)s Crushing It".

With respect to gold, it has beaten back the declining red dots of the Parabolic Short trend, flipping it to Long as we below see with a fresh new blue dot in the chart of weekly bars from a year ago-to-date. But is that all so great? 'Tis oft gold's fate following a geo-political up push to then dwindle back down into the bush. As well, price again finds itself back here in Neverland, (aka "The Whiny 1290s"), the 15-month centerpiece of where it regularly got stuck from June 2013 through August 2014. Moreover, the pricing structure from the low 1300s up to last year's high at Base Camp 1377 is a bit of a congested mess. At least that's by "the then"; let's look to "the now":

As to how both gold and the S&P shake out year-to-date, here are their respective percentage tracks, neither having been in the red throughout, albeit the yellow metal being the more volatile, no doubt:

'Course, we continue to view most the important proponent for the price of gold as the increasing money supply, (let alone unrepayable debt, unfunded derivatives and seniors retiring broke). To be sure, Quantitative Easing (Part Trois) came to a conclusion nearly three years ago on 29 October 2014. The level of the US money supply on that day as measured by M2? $11.56 trillion. Gold's price that day? 1212. Now: Gold's price today? 6.8% higher at 1295; M2's level today? 18.0% higher at $13.64 trillion. Specific to solely that time frame, an 18.0% increase in gold ought have it right now at 1430, although we might shave off a few flecks for any modest increase in its own supply, but certainly 1400. (Then again, our multi-decade gold Scoreboard puts the supply-adjusted price today at 2708 ... and as you know that's before "overshoot").

We mention all that as by the Economic Barometer, clearly activity is slowing, which makes more amusing that died-in-the-wool professionally-paid economists per a Reuters poll out this past week see at least another two years of StateSide expansion. Perhaps they're simply hanging out too much with their FedFolks friends? We instead see the diving Baro as the early hint of having to return to good ole stimulative currency expansion, which of course is nature's own upping of the ante to own gold. As for the Baro's pullback in recent days, notable contributors included a drop in the usage of Consumer Credit, a backing up of Wholesale Inventories, and the Producer Price Index itself actually going backward. Here's the result:

And 'tis not just here. Notwithstanding all the more enthusiastic EuroZone econometrics cited of late, we suddenly see King Germany's industrial output dropping for the first time in 2017, in turn leading to a fall in the nation's trade activity. 'Round the world the other way, Dragon China's growth in both its imports and exports slowed in July. Oh my. Populations grow, economies slow, thus obliging the need for more dough. Got Gold?

We've got gold here in the following two panel chart. On the left are the daily bar's from three months ago-to-date, their baby blue dots of 21-day linear regression trend consistency high in the sky. On the right is the 10-day Market Profile, the most dominant supporter being the heavily traded 1274 level:

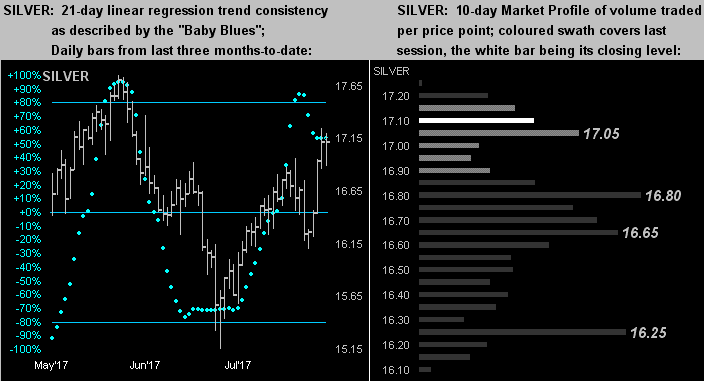

Similarly for Sister Silver we've the same dual view, her "Baby Blues" having come off a bit more than those for gold. Still, her price re-achieved the 17s this past Thursday on a closing basis for the first time since 10 June, 17.05 showing as trading support along with the 16.80 to 16.65 range:

And with a concerned eye toward our "nuthin' but stocks" friends, here too is the like drill for the S&P 500 as depicted by its futures market ("SPOO"). Therein note that the "Baby Blues" have dropped only to the mid-point on their chart, suggesting that should their full downside oscillation play out, there's still time to get out before it all goes wrong. Oh, and for those of you scoring at home, from the S&P's record closing high of 2480 just this past Monday, the correction to here (2441) is but a wee -1.6%. That for a -5.0% move puts the Index at 2356, and then for a -10.0% plunge at 2232. ('Course, the latter never takes place anymore, right?):

In summary, NorKNoise or otherwise, both gold by its rise and the S&P in its dive are for the present on what we see as their directionally proper paths. That said, obviously NorKNoise is not nonsense: the fallout figuratively, let alone literally, of a NorKNuke frightfully can lead to more than just "one and done". But toward maintaining some perspective about it all, we did some simple depth digging to find that NorKLand is the size of Pennsylvania, has quite limited internet availability the architecture of which is archaic, and generates a gross domestic product per capita (nominal basis per the UN) of $648 (vs. that of $56,054 in the US). Thus at the end of the day, one might say, there's not a lot of "there" there and that the good will out.

In the meantime, the upcoming mid-week highlight is the release of the Federal Open Market Committee's minutes from their 25-26 July meeting, (you'll recall after which there was no press conference). Will they have followed the jolly economists as seen in the poll, or instead recognize the economy doth slow? Either way, hang onto your gold!

share

share

share

share

share

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.