The Pensions Mess: Can Gold Help?

The British have recently seen two unpleasant examples of the cost of pension fund deficits. A deficit at British Steel, estimated to be about £485m, was followed by a deficit at British Home Stores of £571m. In both cases, pension fund deficits have scuppered corporate rescue plans, because understandably no buyer will take on these liabilities.

These two cases are the small tips of a very large iceberg, and reflect problems not just in Britain, but anywhere where pension schemes exist. They have been brewing for some considerable time, but have escalated as a direct consequence of central banking’s monetary policies. They are a crisis whose cause is concealed not only from the pensioners, but from trustees and investment managers as well.

This article lays out the problem and its scale, so far as it is known, and notes that a pension fund that has a holding in gold is a very rare animal. Indeed, one of the best known examples, the Teacher Retirement System of Texas, holds less than 1% of its $130bn assets in gold.

A short recap of the industry’s post-war development will give the pension issue its context, before commenting on the role gold can play. Pensions have existed for some time, but they really took off after the Second World War, driven by tax policy. Corporations were encouraged to set up pension funds for their workers, with employer and employee contributions being tax deductible.

From a government’s point of view, the tax relief granted cost little in terms of current expenditure, because it replaced the tax income forgone from corporations and employees, with deficit funding through bond markets. Furthermore, the demand for government bonds from accumulating pensions meant that there would always be demand for government debt, and interest paid would be less than otherwise. While governments have generally increased taxes on savings, pension schemes have been encouraged. They have become a material component in the financial system, and the only savings channel encouraged by governments.

In setting up a pension fund, the advising actuaries would have taken all variables into account. Of the many variables, the principal ones are the period of employment required for a full pension, the life expectancies of the scheme members, and the expected return on investments.

We are all aware that pensioners live longer, and that life expectancies have generally been underestimated. This has certainly been a problem. Some countries have responded by raising the retirement age. It is also obvious that rising or falling bond and stock markets have a direct impact on portfolio valuations. However, investment returns in the early days were relatively simple to calculate: they would be the average gross yield to redemption of the bonds that comprised the whole fund. These were mostly government and municipal bonds, and therefore unlikely to default. Bond prices didn’t matter, because they were nearly always held to final redemption at par.

That was fine, until portfolio managers began to explore other investment possibilities in the 1960s. Portfolio allocations started to migrate from low-risk government debt and high-quality corporate bonds, into blue-chip equities. This was the era of the nifty-fifty, and diversification was rewarded with enhanced capital returns over the redemption yield on government bonds. The seventies were somewhat different, with portfolio losses mounting on equities in the savage 1972-74 bear market, but compensation was found in the compounding effect of higher bond yields, which still comprised the dominant portfolio allocation. And we still haven’t mentioned on the most significant factor.

Increasing bond yields over the seventies decade benefited pensions because they allowed actuaries to sign off on lower amounts of capital required to cover pension obligations. This is because the capital required to fund a given income stream is lower when interest and dividends accrue at a high rate of interest, compared with when it accrues a lower rate. For example, an annual commitment to pay pensioners $100m from a portfolio yielding 10% requires it to have a minimum invested value of $1,000m. But a portfolio yielding only 5% has to be worth at least $2,000m to cover the same payment obligation. This is why the assessment of future returns is the most volatile component, leading to unexpected surpluses and deficits as reality unfolds.

Obviously, pension funds which are invested in high quality bonds produce a reasonably certain return, because they are held to maturity, so gross redemption yields are what matter. Equities used to be valued on dividend payments, originally yielding more than government bonds, reflecting their credit risk. That changed in the late 1950s, when portfolio managers began to take a different view, attracted by the potential that equities offered for capital gain. And over time, the potential for returns on equity investments even came to be defined as total returns, de-emphasising the dividend element.

Consequently, actuaries were progressively forced to move from the certain world of gross redemption yields into the uncertain world of guessing future returns on equities. By the 1990s many pension funds, faced with declining bond yields, were increasing their allocations in equities, property and even alternative investments such as art, to the point where bonds were often a minor component of pension portfolios. Inherently speculative capital gains on investments were generating valuation surpluses large enough to allow companies to take contribution holidays.

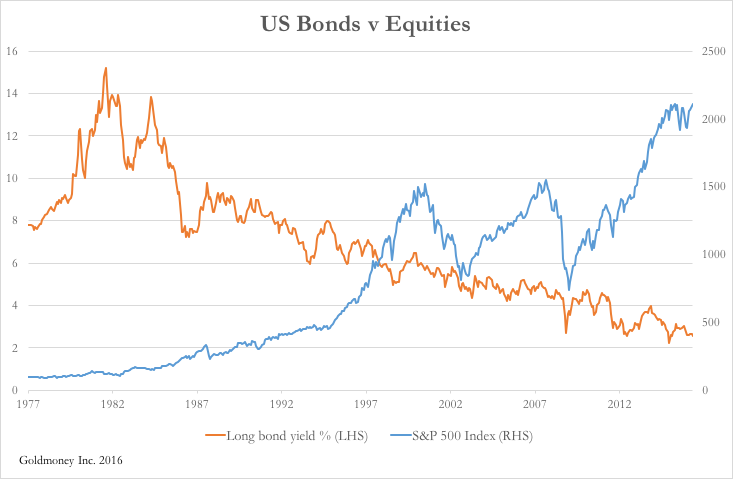

The outperformance of equities drove the shift from bonds to equities. This is illustrated in the chart below, which clearly shows why over the long term, allocations in favour of bonds have decreased, while allocations in favour of equities have increased.

However, the 2000-02 bear market created the first significant set of difficulties for pension funds. Not only did equity markets roughly halve, but bond yields continued their decline as well, when the Fed lowered the Fed funds rate from 6 ½% in December 2000 to only 1% eighteen months later. This created a double problem for the pension fund industry, because the sharp decline in equity markets was accompanied by a record low in interest rates. Unlike the seventies, falling equities were not compensated by rising bond yields.

Faced with triggering a wave of insolvencies of large labour-intensive businesses, pension actuaries in the US came under considerable pressure not to show large valuation deficits. The solution was to endorse incautious long-term estimates of total returns in equities. This at least got corporate America off the hook, and actuarial practice elsewhere followed this example. Fortunately, the stock market performed well, doubling between September 2002 and October 2007.

The Lehman crisis that followed hit the pensions industry hard a second time. In the fifteen months to February 2009 the S&P500 Index more than halved, as did the yield on the long bond. Following this sharp sell-off, valuation problems were partially covered by a stock market recovery, and there was the prospect of higher bond yields when monetary stimulus normalised economic activity. The latter never materialised, and the prop of rising equity markets, after an impressive run, now appears to be stalling. The big problem now, the elephant in the room, is realistic assessments of total return on the amount of capital required to pay existing and future pensioners.

In summary, since the dot-com bubble, we have seen a ratchet effect of declining bond yields, a doubling and then halving of equity markets, leading to alternate periods of deficit reductions followed by deficit increases. This problem has been totally ignored by central banks when setting monetary policy. You could describe the current situation as one of a massive wealth transfer from pension funds to debtors, storing up yet another savings crisis. The idea that monetary policy assists and encourages businesses to grow, ignores the detrimental off-balance sheet effects on the pension liabilities that the same companies now face.

The result is pension fund deficits today stand at record levels, even after a doubling of equity markets over the last five years. A Financial Times article (10 April) reported the deficit on US public pensions at the end of 2015 was $3.4 trillion, and in the UK, the aggregate deficit of some 5,000 pension schemes is estimated at £805bn (FT 27 May). Bear in mind that these numbers are based on total return estimates that are likely to turn out to be far too optimistic, because of the valuation effect described in this article.

Goodness knows how bad it must be for pension funds in countries where negative interest rates have been imposed. The cost in Japan will be reflected in $1.2 trillion of pension assets, and in the Eurozone a further $2.33 trillion. Of particular concern must be the liabilities faced by the banks in these regions, bringing in a direct systemic element into the equation.

Can gold help?

We can see that pension funds have an enormous and accumulating problem of capital shortfalls, which through over-optimistic assessments of future total returns are likely to be understated. The cost will be swallowed by pensioners in all the advanced nations, who have been promised a certain income in their retirement. It amounts to the impoverishment of the elderly, and the prospective insolvency of companies unable to cover their pension deficits. The question we now need to ask ourselves is whether or not an allocation of gold and related investments can help ameliorate the situation.

Essentially, we are now moving our analysis from considering nominal returns to real returns adjusted for price inflation. At the moment, roughly a third of all sovereign debt carries negative interest rates, but adjusted by consumer price indices, this increases to almost half. Furthermore, if we take into account the simple fact that standardised CPI estimates understate true price inflation, negative real yields probably apply to over three quarters of all sovereign debt.

The only salvation for pension funds is for global equities to continue to rise at significant rates, yet this seems unlikely given that equities on an historical basis are already extremely expensive. The Grim Reaper is knocking more insistently on the pension fund door.

In the medium to long term, gold has a track record of enhancing investment returns. The reason is very basic: the economic costs of production tend to be considerably more stable measured in gold than in fiat currencies. Given monetary policies are explicitly designed to reduce the purchasing power fiat currencies over time, the price of gold measured in these depreciating currencies is set to rise. With bonds reflecting negative real yields and stock markets wildly overvalued, gold, along with other tangible non-depreciating assets, is therefore the only game in town.

The explanation why gold performs well in deflation is equally simple. With falling prices, the purchasing power of gold tends to rise. Whether or not this is reflected to the same extent in a fiat currency is mainly a function of the rate of monetary expansion in the currency relative to the expansion of the quantity of gold available for monetary use. No prizes for guessing which can be expected to expand fastest.

Therefore, gold has a place in portfolios irrespective of inflationary or deflationary expectations. There is, however, a problem. Global pension fund assets are estimated to have been valued collectively at over $26 trillion at the end of 2014, and a one per cent increase in allocation into physical gold is the equivalent of 6400 tonnes at today’s prices, about 40% the estimated above-ground stocks. Investing in gold mines is similarly constrained.

For an investment in gold, a balanced pension fund portfolio would have to consider an allocation closer to 10%, which on an industry-wide basis is impossible at anything like current prices. Furthermore, the average investment manager has difficulty categorising gold as an investment, unsure if it is a commodity, money, or a hedge against future uncertainty. Ironically, the oldest asset class is now being described as the newest asset class by the few managers showing an interest in gold. There is a considerable educational challenge involved.

Nothing educates more rapidly than experience. If bond yields remain low, and equity markets spend some time just consolidating the rises of the last five years by moving sideways, pension fund deficits will continue to increase to new record levels of deficits. That is probably best-case. Anything else is likely to accelerate the crisis, encouraging investment demand for gold, particularly if, as has been the case so far this year, it continues to outperform both equities and bonds.

The best solution for any pension fund will be to get in early, ahead of its peers.

___________________________________________________

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

MOBILE: +44 7790 419403