Technical Analysis vs. Fundamentals

Every week we talk about the supply and demand fundamentals. We were surprised to see an article about us this week. The writer thought that our technical analysis cannot see what’s going on in the market. We don’t want to fight with people, we prefer to focus on ideas. So let’s compare and contrast ordinary technical analysis with what Monetary Metals does.

Technical analysis, in all of its forms, uses the past price movements to predict the future price movements. In some cases (e.g. momentum analysis) it calculates an intermediate signal from the price signal (momentum is the first derivative of price). But no matter the style, one analyzes price history to guess the next price move.

This is necessarily probabilistic. There is no way to know that a particular price move will follow the chart pattern you see on the screen. There is no certainty. And when it does work, it is often because of self-fulfilling expectations. Since all traders have access to the same charts, and the same chart-reading theories, they can buy or sell en masse when the chart signals them to do so.

We are not here to argue for or against technical analysis. We simply want to say that it’s not what we are doing. Not at all.

Our analysis is based on different ideas. The key idea is that there is a connection between the spot and futures market. That connection is arbitrage. Think of each market as a platform that moves up and down on its own vertical track. The two tracks are close together. And the platforms are connected to each other by a spring. Suppose platform A is a bit above platform B. If you push up on A, then the spring stretches a bit more and will pull B up, though perhaps not as much. The same happens if you push down on B.

Conversely, if you push down on A, then it will compress the spring and platform B will tend to go down, though not as much.

A and B are the futures and spot markets for gold (the same analogy applies to silver). Arbitrage works just like a spring. If the price in the futures market is greater than the price in the spot market, then there is a profit to carry gold—to buy metal in the spot market and sell a futures contract. If the price of spot is higher, then the profit is to be made by decarrying—to sell metal and buy a future.

There are two keys to understanding this. One, when leveraged speculators push up the price of gold futures contracts, then that increases the basis spread. A greater basis is a greater incentive to the arbitrageur to take the trade. Two, when the arbitrageur buys spot and sells a future, the very act of putting on this trade compresses the spread.

If someone were to come along and sell enough futures contracts to push down the price of gold by $50 or $150 or whatever amount is alleged, then this selling would be on futures only. It would push the price of futures below the price of spot, a condition called backwardation.

Backwardation just has not happened at the times when the stories of the big “smash downs” have claimed. Monetary Metals has published intraday basis charts during these events many times.

The above does not describe technical analysis. It describes physics—how the market functions at a mechanical level.

There are other ways to check this. If there was a large naked short position in a contract that was headed into expiry, how would the basis behave? The arbitrage theory predicts the opposite basis move. We will leave the answer out as an exercise for the interested reader, as thinking this through is really good work to understand the dynamics of the gold and silver markets (and you can Google our past articles, where we discuss it).

This check can be observed every month, as either gold or silver has a contract expiring (right now it’s gold, as the April contract is close to First Notice Day).

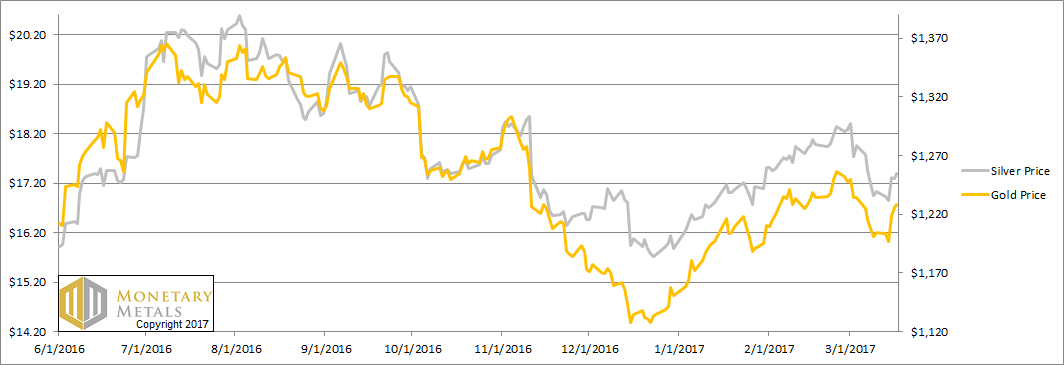

This week, the prices of the metals both rose. The price of gold is almost back to where it was the prior week, but that of silver is not.

Below, we will show the only true picture of the gold and silver supply and demand. But first, the price and ratio charts.

The Prices of Gold and Silver

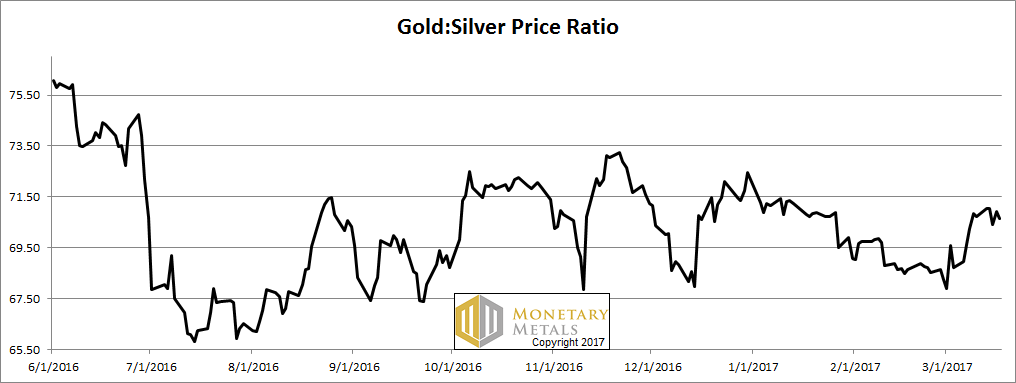

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. It moved sideways this week.

The Ratio of the Gold Price to the Silver Price

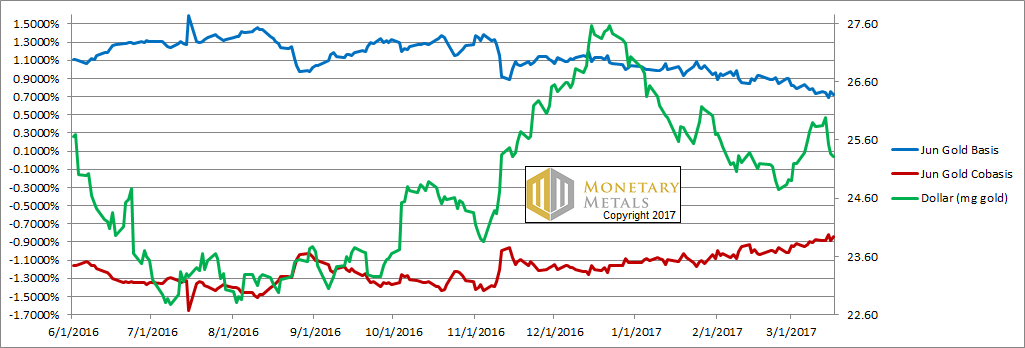

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

NB: we switched from the April to the June gold contract.

As the price of the dollar fell (inverse of the rising price of gold, measured in dollars) we see the cobasis (our measure of scarcity) increased a bit. This means the buying in gold, which pushed up the price, was buying more of physical than of futures. This seems to be the new pattern of late, though it is sputtering a bit like an engine trying to start up and run at a steady RPM.

Our calculated fundamental price of gold is up nearly $50. It is now over $1,400.

Now let’s look at silver.

The Silver Basis and Cobasis and the Dollar Price

The story is the same in silver. Rising price accompanied by rising scarcity.

The silver fundamental price rose 50 cents. It is now about $1.30 over market.

© 2017 Monetary Metals

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.