Four Important Facts To Remember About Gold

When volatility prevails in the gold market, I love seeing so many different opinions because it promotes critical thinking and healthy markets. But because gold is unlike any other commodity, many perspectives can be extreme, such as “goldenfreudes” who take pleasure in gold bugs’ pain.

I continue to persuade readers to take a balanced and thoughtful approach to the yellow metal. With this in mind, here are four facts to remember about gold that should help neutralize those extreme bullish and bearish views.

1. You can’t print more gold

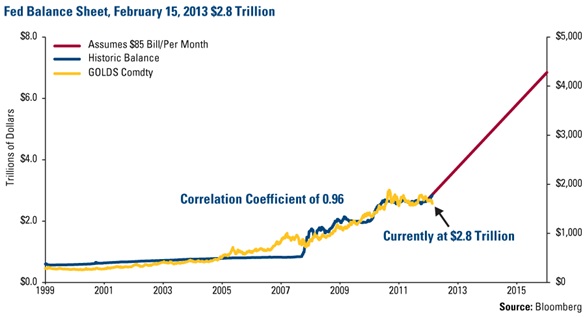

The Federal Reserve continues to print fresh, crisp stacks of U.S. dollars amounting to $85 billion every month, driving up the balance sheet to almost $3 trillion dollars. If Ben Bernanke continues churning out dollars at this rate, by 2016, the balance sheet will more than double to $7 trillion dollars.

And research has found that the price of gold moves in near-lockstep to each increase in the Fed’s balance sheet.

Even with the incredible two-day drop in gold prices, U.S. Global portfolio manager Ralph Aldis calculated that the correlation between the rise in gold and the U.S. balance sheet is 0.96. Perfect correlations of 1 are extremely rare in markets, but gold and the balance sheet have moved in sync with each other since 1999, before gold’s bull run began.

2. Gold is viewed as a currency by central bankers

As gold was falling on April 15, Carl Quintanilla from CNBC asked me what I thought about how investors viewed currencies. I feel investors should look at how central banks around the world are viewing their own reserves. Although Cyprus and Italy were possibly forced to sell their gold holdings to pay down debts, take a look at the actions of emerging countries central bankers who are scooping up gold.

The World Gold Council (WGC) reported that in 2012, central banks purchased 535 tons when only a few years ago central banks were net sellers of gold. And it’s important to keep in mind that these central banks love these corrections, as they can purchase gold at cheaper prices.

Russia bought 75 tons, bringing its gold holdings to the seventh largest in the world, with about 1,000 tons. Last year, Brazil, Paraguay and Mexico purchased gold, as did South Korea, the Philippines and Iraq.

Turkey is another country that has been building reserves, though not from purchases. Rather the WGC says its growing gold reserves “reflect the increasing role that gold plays more broadly in the Turkish financial system as these reserves are substantially pledged from commercial banks as part of their required reserves.”

While the tonnage is only a fraction of the overall gold market, it is widely acknowledged that central banks are building their supplies of gold as a means to diversify their holdings away from the U.S. dollar and the euro. As a percent of total reserves, many of these emerging countries mentioned above own very little gold. In fact, Pierre Lassonde, chairman of Franco-Nevada, has noted that even if emerging market central banks wanted to increase their gold reserves to 15 percent of total reserves, they’d have to buy 1,000 tons every year for the next 17 years!

3. A lack of love from the Love Trade is affecting fundamentals

Too many people focus on the Fear Trade, which is when investors buy gold coins or a gold ETF out of a fear of the fallout that may result from governments’ rising debt levels and weakening currencies.

The Love Trade, on the other hand, is the buying of gold out of an enduring love for gold. Two emerging countries that make up almost half of gold demand—China and India—have had a long relationship with the precious metal that is intertwined with their culture, religion and economy. With half of the world’s population buying gold for their friends and family, it’s important to put into context what is happening in their countries.

It was announced this week that China’s income growth slowed in the first quarter of 2013, with urban household disposable income rising only 6.7 percent on a year-over-year basis. This is down from 9.8 percent in the first quarter of 2012, and “the slowest pace since 2001,” says Sinology’s Andy Rothman.

This is very important to gold, as China’s income growth has been shown to be highly correlated to the price of the precious metal over the past decade.

China’s weaker GDP also disappointed gold investors, but I believe this is only a temporary setback. It’s only a matter of how fast China will move to stimulate the economy, since this is a key to global growth.

In India, gold consumption has been hurt by both a weak rupee and government taxes on imports. In the first quarter of 2013 alone, gold imports declined 24 percent, according to Mineweb.

4. Corrections happen, but have historically offered buying opportunities

As of the end of April 15, the gold price on a year-over-year percentage change basis registered a -2.6 standard deviation. While minor corrections in the gold price happen frequently, a move this severe has never occurred before over the previous 2,610 trading days.

With gold’s standard deviation drastically below the “buy signal” blue band, we consider the yellow metal to be in an extremely oversold position on a 12-month basis. The probability that gold will move higher over the next several months is high.

Be Curious to Learn More About Gold

Gold is clearly unlike any other commodity on the periodic table. Its climb year-after-year has enraptured investors to learn more about what’s driving gold.

Want to receive more updates like this one? Sign up to receive email updates from Frank Holmes and the rest of the U.S. Global Investors team, follow us on Twitter or like us on Facebook.

********

U.S. Global Investors, Inc. is an investment management firm specializing in gold, natural resources and emerging markets opportunities around the world. The company, headquartered in San Antonio, Texas, manages 13 no-load mutual funds in the U.S. Global Investors fund family, as well as funds for international clients.

The commentary references the investment theory of an investment as insurance against a separate market event that could negatively affect performance of an investment. The reference does not guarantee performance or a safeguard from loss of principal by investing in that asset. By clicking the links above, you will be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].