Gold Coins And Bars In Demand…+9% In Q1, 2017

– Global gold demand in Q1 2017 was 1,034.5t

– Total demand -18% from record high levels in Q1, 2016

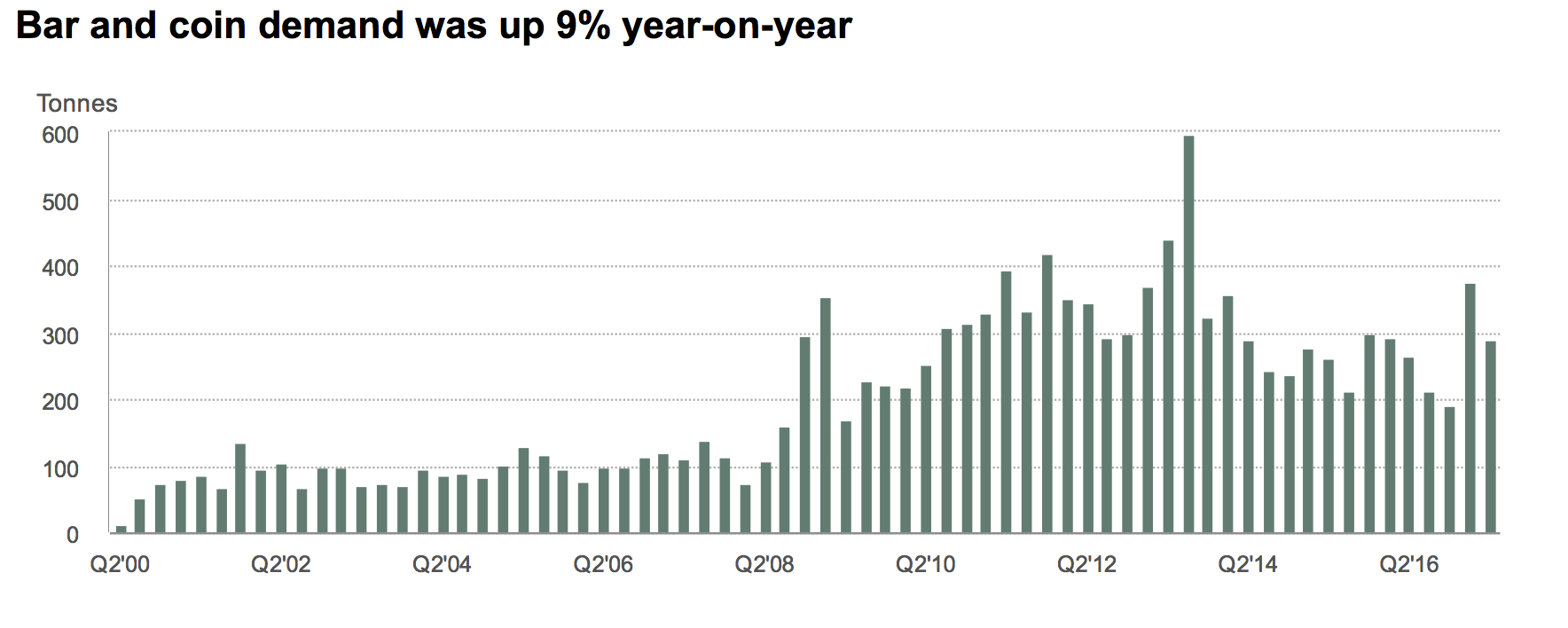

– Demand for coins and bars up 9% yoy to 290 t

– UK demand for coins, bars at highest since Q2 2013

– ETF inflows fell by 2/3, account for overall -18% fall in demand

– European uncertainty brings gold investors to market

– Innovation continues to drive gold demand in China

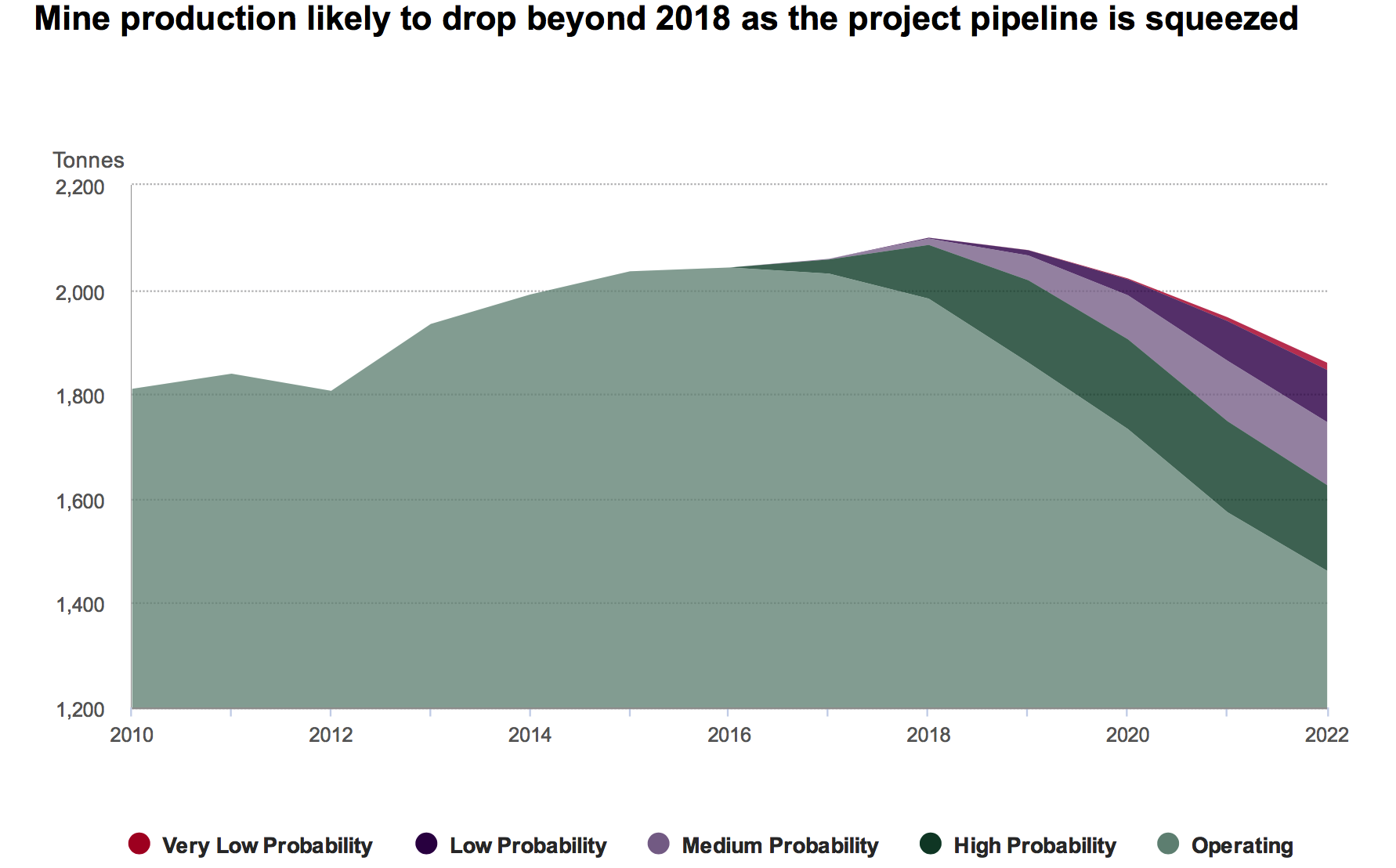

– Peak Gold: Mine production likely to drop

Global Gold Demand Driven By Climb In Bar And Coin Investment

Uncertainty in Europe increased demand for gold investment products in the first quarter of the year, according to the World Gold Council’s Gold Demand Trends Q1, 2017 report.

Across the globe a mixture of festivities and renewed safe haven buying saw demand for gold bars and coins climb by 9%.

Demand for physical investment products helped to reduce the overall fall in gold demand, which came in at 18% YOY, across investment, jewellery and central bank demand.

In all, global gold demand across a number of measures points towards a world that is uncertain and to ongoing safe haven demand. In some cases such as in the US, EU and China, demand remains robust whereas in the likes of Turkey demand is down from record levels.

Much of this is thanks to geo-political uncertainty and political upheaval.

Political uncertainty in Europe has helped to increase demand for gold bullion. Elections (upcoming and past) in the UK, Netherlands, France and Germany have helped to buoy investment in safe haven gold. German gold bar and coin demand had its strongest first quarter since 2011 – 13% yoy to 34.3t, but this must not take away from the UK which hit its highest level since Q2 2013.

China (discussed in full below) was a major contributor to the uptick in demand for gold bars and coins, posting a 30% gain. As with its European counterparts, there is much uncertainty over the economic situation of the country and both investors and retailers alike are able to match these feelings with gold purchases.

Politics, Uncertainty And Gold Prices Make For A Mixed Bag Of Jewellery

When it comes to jewellery, demand was mixed across the board but overall very low, compared to recent years. Demand was 18% below the 587.7t five year quarterly average. The 9% climb in the USD gold price, meant that there is overall long-term weakness in the sector.

Whilst uncertainty can be a positive driver for gold demand, this combined with a high gold price in Turkey saw demand for jewellery sink to a four year low of 7.7t. The looming referendum (held in April) combined with the fact that the price of gold in lira rose more than in any other currency during Q1 (+12%), meant that the fragile political and economic conditions continued to impact the sector.

The WGC state that “The outlook for the [Turkish] market is weak” and this is expected to continue as both economic and political reforms keep both uncertainty and the gold price high.

In the United States however, a feeling of relief following the US election propelled jewellery demand to its strongest Q1 since 2010 – it rose 3% to 22.9t. The WGC refers to a climb in ‘clicks and mortar’ (online) purchases. There is little doubt that the election hasn’t increased uncertainty, but it seems there is a calm before the storm element to purchasing decisions.

In Europe, both the UK and France let the side down when it came to jewellery demand, which fell 6% in the Fifth Republic. Much of the fall was down to uncertainty in the run-up to elections and a spate of terrorist attacks.

It seems many buyers are favouring ‘branded silver’ in their jewellery purchases. In the same way that silver coin and bar buyers see silver as better value than gold – it seems that jewellery buyers also may be attracted to getting better value with silver.

Investment Is Better Than Jewellery – Even For Romantics

On Valentine’s Day we discussed the problems with buying jewellery as an investment. Jewellery is a terrible investment due to the significant mark-up at the point of sale, ‘valued added’ (VAT) and sales taxes and it’s very poor resale value. We suggested that romantics buy gold coins and bars for their loved ones instead.

This advice was perhaps heeded even after Valentine’s Day as gold bars and coins had an excellent quarter, with 289.8t of demand (+9% yoy). Much of this was thanks to China, where safe haven flows, tech innovation and Chinese New Year is helping to push demand (see below).

The WGC accounts much of the increase in coin and bar demand to the ‘strength of the retail investment market’ internationally. Companies such as GoldCore are seeing very strong demand – particularly for allocated and segregated storage for risk averse investors looking to own in gold bars and coins.

The feeling of uncertainty and uncertain outlook does appear to be driving demand and this is a trend we suspect we will continue to see. Whilst elections have been, or will soon be decided, that does not guarantee the economic result, investors are aware of this and stocking up on gold accordingly.

Gold ETFs Failed To Benefit As Much As Physical Gold

Whilst ETF inflows did not experience the same surge as gold bar and coin demand, US demand was strong. As the WGC points out, geopolitical tensions were ‘more of a concern for European based investors than for their US counterparts.’

The report refers to the positivity in the US towards gold, and that the speculative buying seen in 2016 has been ‘reversed in the November/December washout’ leaving strategic investors behind. Having said that the only net inflows were in February, ‘sandwiched between’ outflows in January and March.

Collectively in Europe we make for a worried bunch. Europeans increased inflows in gold ETFs, as we saw with gold bar and coin demand.

As summarised by the WGC, we are surrounded by both economic and political uncertainty which, with some dips in the gold price, meant we could increase our exposure to gold:

‘On top of a fragile political environment, conditions in financial markets gave investors a further incentive to build their positions in gold-backed ETFs. Safe haven flows pushed two year German yields further into negative territory, reaching a record low of 0.95% in February. And European equity markets were subdued with volatility at multiyear lows. Negative real and nominal yields coupled with a period of relative calm in regional stock markets improved the appeal of gold, particularly as its price strengthened through the quarter. The dips in the euro denominated price of gold in January and March were also taken as a good opportunity to add it to portfolios.’

Gold ETF holdings grew tremendously in 2016. 2017 has failed to keep up as of yet. Inflows were just one-third of those seen in Q1 2016. Unsurprisingly the WGC do not seem unduly worried, despite pointing towards the fact that Q1’s figures might be pointing to a wider financial issue, ‘inflows of 109.1t are in line with quarterly average between Q1 2009 and Q4 2011 (108.7t), a period that encompassed the global financial crisis.’

Whilst calm is often seen settling across a market after a surge such as that seen in 2017, we wonder if we will continue to see a slow-down in ETF inflows, especially if averages such as these have not been since since the financial crisis.

Earlier this week we wrote about the tenuous London property market and asked if this was an indicator of a bubble about to burst, setting off a domino effect around the world. This would obviously lead to even greater safe haven flows and demand.

Innovation Holds Key To Future Of China’s Gold Market

Whilst the gold market is one of the oldest in the world, it is markedly different from how it once began.

Gold bullion dealers and jewellery sellers have made a concerted effort to keep up with innovations across the technological, investment and retail spaces. This is more important today than it has ever been.

In China, there has long been concern that China’s millennial population will not look at gold in the same way as their elders do. The WGC cites research from Agility Research & Strategy which shows the top three priorities for young Chinese are ‘health, travel and spending time with the family’. This, combined with concerns over the economy, has prompted worries for the future of the world’s largest gold market.

However, innovation both technological and in marketing suggests that the Chinese gold market has a resilient and fruitful future. As the WGC writes, “the industry is keen and determined to adapt – an attitude that should help stem any weakness.”

In the jewellery space, where demand was slightly down by 2% thanks to high gold prices following Chinese New Year, sellers are providing services and products to keep up with today’s younger generations – such as more modern 18k gold jewellery pieces, rather than the traditional 22k gold designs. In a perhaps more reflective sign of the times, sellers of bridal jewellery are ‘offering customers a no-cost exchange option on jewellery from its bridal range.’

Jewellery demand may have experienced a small decline, but gold bars and coins saw a 30% increase (yoy), its fourth best quarter on record. We would generally expect the first quarter of the year to be a strong one for China, given their New Year, however it was this combined with concerns regarding the economy (falling yuan and property market) that drove demand to 105.9t.

Some of this stellar demand can be attributed to the innovation appearing in the local gold market, namely interest-paying gold accounts, benchmarked on the Shanghai Gold Exchange (SGE)’s AU9999 contract with a minimum entry point of one gram. It is traded online, with an option for physical delivery – all important for Chinese investors.

Online developments continue with 800 million WeChat users being given access to MicroGold, a physical gold-backed product offered by ICBC. Digital gold can be traded between individuals, online, supporting festivals and culturally significant events with ‘red envelopes.’

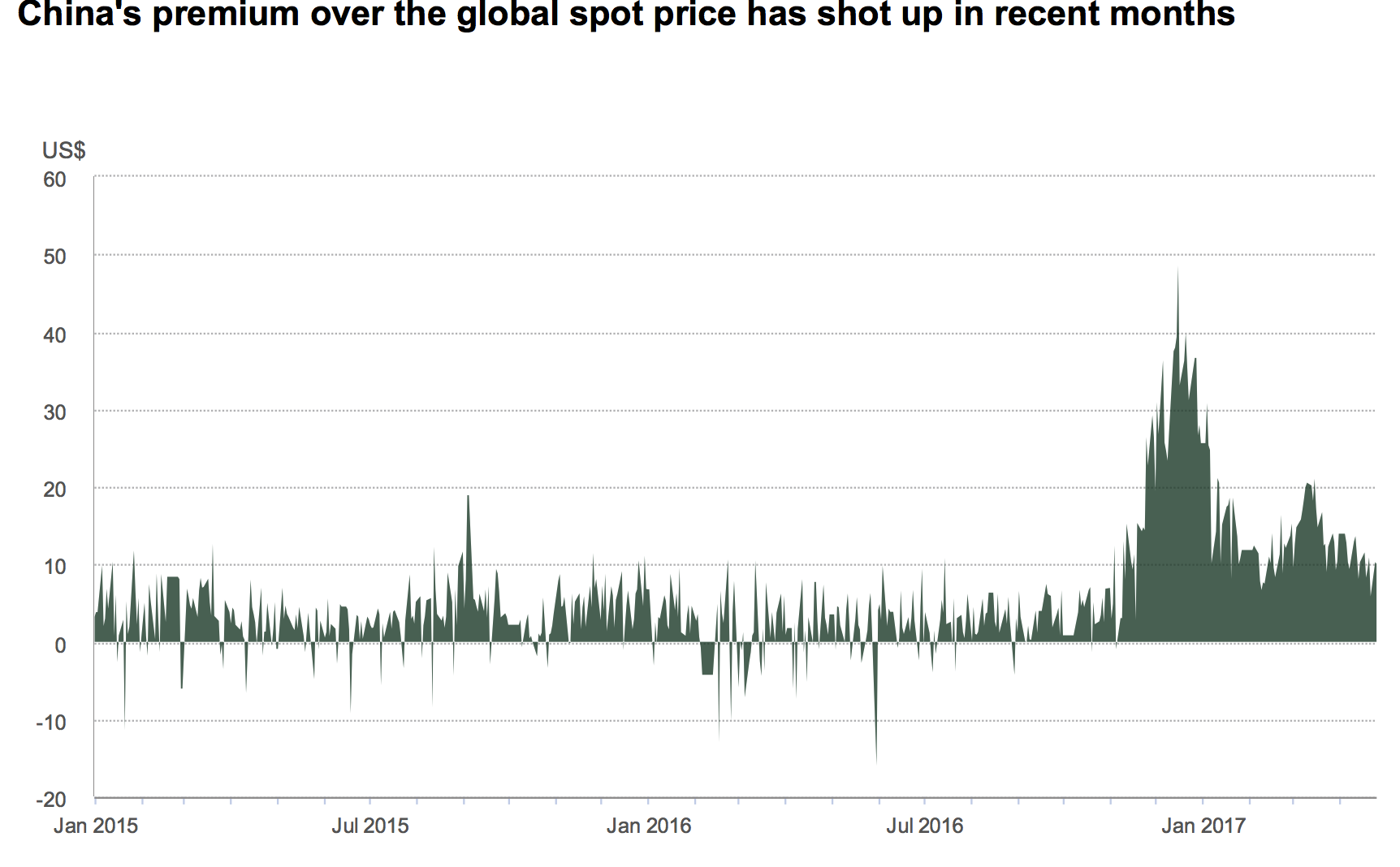

These moves, combined with recent changes supported by the government have led to an imbalance between supply and demand. Premiums have shot up over global gold price in recent month, they averaged $17/oz in Q4, 2016, and averaged down to US$14.2/oz.

India, Cashless Push Was Merely A Setback But Innovation Required

India had a tumultuous year last year, the second-half of 2016 saw Modi take the country by surprise when he announced the removal of old Rs 500 and Rs 1,000, throwing millions of people into financial chaos. The announcement was particularly badly timed due to wedding season which is vital to the country’s gold industry.

Since then gold demand has managed to find some calm. Whilst global jewellery demand remains weak with just a 1% increase in Q1 India has propped it up, despite rising gold prices, posting a 16% gain.

The 16% gain isn’t really much to shout about, given it is only the third quarter this decade where demand has come in at less than 100t (92.3t). There is still some wariness in terms of how the next phase of remonetisation will play out, combined with uncertainty over the forthcoming Goods & Service Tax (GST), which is dampening demand somewhat.

We would suggest that there is something to be learnt both at the business and political level when it comes to innovation in the gold market. This is perhaps coming to pass as the WGC’s field research found that not only are consumers gradually adopting cashless payments, but cashless transactions are ‘gathering momentum’. Retailers such as Tanishq reported a ‘quite significant recovery’ in Q1, on account of cashless transactions.

At this point we should issue a word of warning, as we did when India announced its move to cashless and the topic became the point of discussion in economic circles. Whilst cashless is publicised as a way to make economies more efficient, to reduce tax evasion and to prevent other criminal activities it is also there to serve an ulterior motive – as we wrote a few month’s ago:

“A cashless world means a transparent world, which is great if terrorists were the only ones using cash. But they’re really not, so a cashless world means transparent bank accounts which means restricted banks accounts.”

This is perhaps yet another reason why gold demand is recovering in India.

Trivial Sales In Central Bank Demand

Whilst purchases by central banks slowed, they remained robust – especially from Russia and China – and central bank sales remain nearly non-existent and are set to do so.

Quarterly net purchases were 76.3t (a six year low) and a 27% fall yoy. Russia and Kazakhstan were the main buyers in the quarter.

China’s gold reserves still represent just 2% of their total reserves, despite not adding to the reserves since October 2016. The ratio hit 2.4% in Q1, its highest point since the early 2000s and the reason perhaps for no further purchases since 2016. It is also worth noting the pressure their FX reserves have felt for some time having dropped from US$3.2 trillion in January 2016 to US$3 trillion in January 2017.

Peak Gold: Mine Production Likely To Drop

There are many tidbits of information in the WGC’s report about overall mine production in Q1 2017.

Indonesia accounted for the largest impact on the fall in production, thanks to a fall on 8t from its Grasberg region. There were also some areas of growth, however physical gold investors mainly need to be aware of the following summary from the WGC:

“Having plateaued in recent years, mine production will soon enter a period of decline. The production profile of currently operating mines shows a relatively steep drop-off over the next 5 to 10 years. Even factoring in high probability projects (those highly likely to reach commercial production), the fall in production is still significant.”

The negative feeling from the WGC is attributed to cuts in capital expenditure but most importantly the fact that there just aren’t that many new discoveries of gold.

“Inevitably, the supply pipeline will be squeezed…The speed at which production will fall is uncertain. As existing reserves are depleted, the current project pipeline will be unable to replace them fully.

Over the long-term, the global production profile will depend on the trajectory of the gold price and potential exploration upside, particularly the speed with which brownfield exploration can be brought into production”

Conclusion: Buy Physical Gold – Not Making Much More Of It

The news that gold production is falling and the near certainty that production levels will fall in the coming months and years should be enough to encourage investors to buy gold.

Even if political and economic turmoil weren’t a factor in every major country, gold demand would still be pertinent thanks to the issue of peak gold.

However, it is the imminent feeling of uncertainty and growing instability which is driving investors to allocate more of their investment and pension portfolios to gold bars, coins and ETFs.

The motto ‘Stay calm and carry on’ is no longer relevant, it should be ‘stay calm and buy gold’.

********

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.