$39,210 to $184,000 per ounce: Gold’s true present-day value as a reserve currency – VanEck

NEW YORK (January 13) While gold rapidly approaches a once-unthinkable $5,000 per ounce, the real price of gold would be orders of magnitude higher if it needed to back the money already in circulation – with the currencies of some of the world’s most developed economies among the most at-risk, while countries like Russia and Kazakhstan could comfortably adopt the gold standard tomorrow, according to fixed income analysts at VanEck.

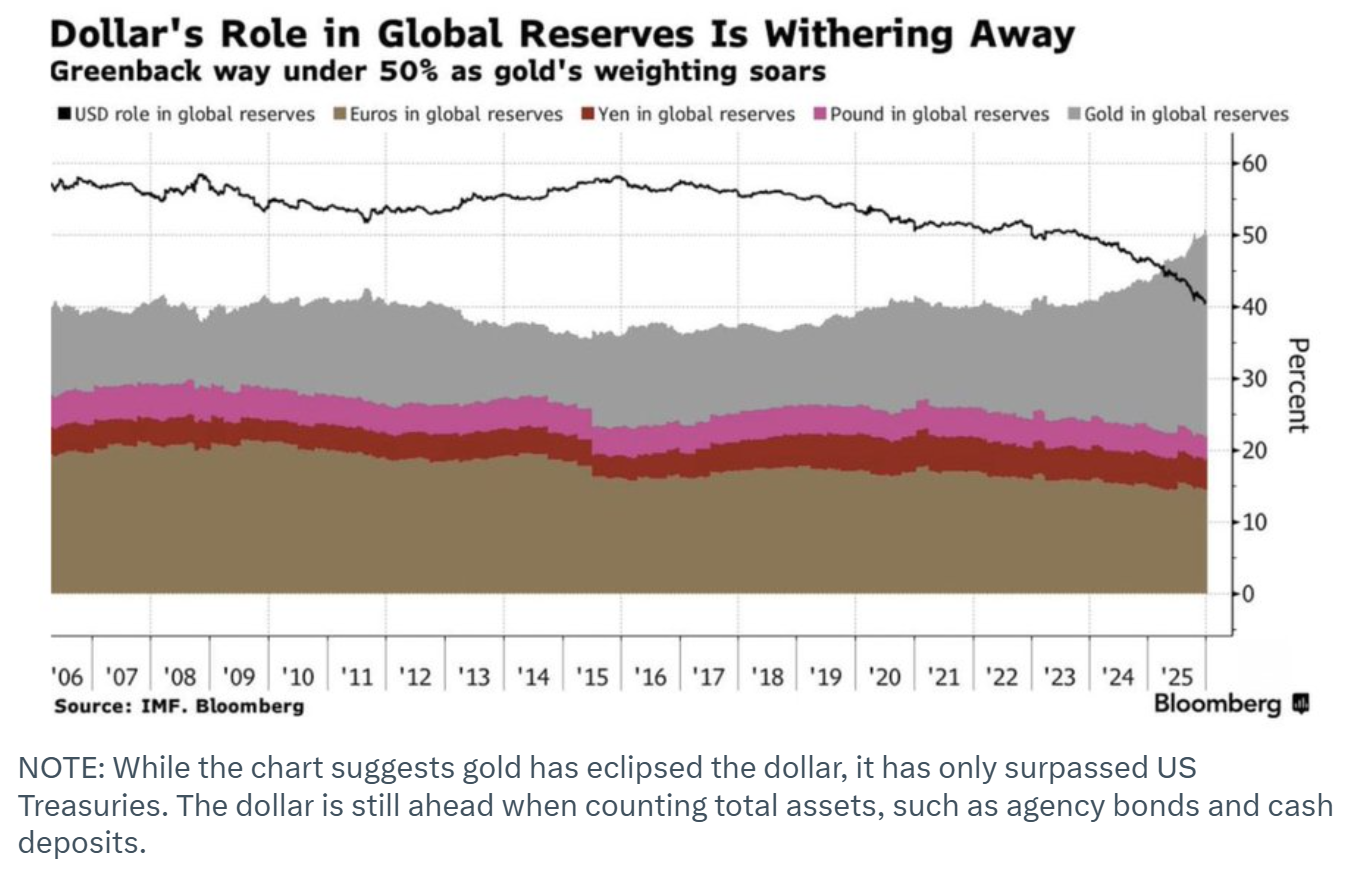

“What is the ‘real’ price of gold?” VanEck’s Emerging Markets Bond team asked in a recent analysis. “Not the price you see on the screen today, but the price if gold were to reclaim its role as the global reserve standard,” Central banks are buying gold at record paces, and questions are swirling about the longevity of the U.S. dollar’s dominance.”

Based on gold’s recent surge as a reserve asset, the analysts believe this question is overdue.

The analysts said this state of affairs begs the question: What would the gold price be if it had to back the global money supply?

“For most of modern financial history, this was not a hypothetical question,” they noted. “Under the classic Gold Standard, paper currency was merely a claim check for physical gold in a vault. That link was fully severed in 1971, moving the world to a ‘fiat’ system where money is backed only by government decree.”

The VanEck analysts posing this question today, not because they believe the gold standard will return tomorrow, but because it serves as what they call the ultimate solvency check. “By calculating the price gold would need to reach to back today's money supply, we can see just how much paper money has been printed relative to the hard asset that once underpinned it all.”

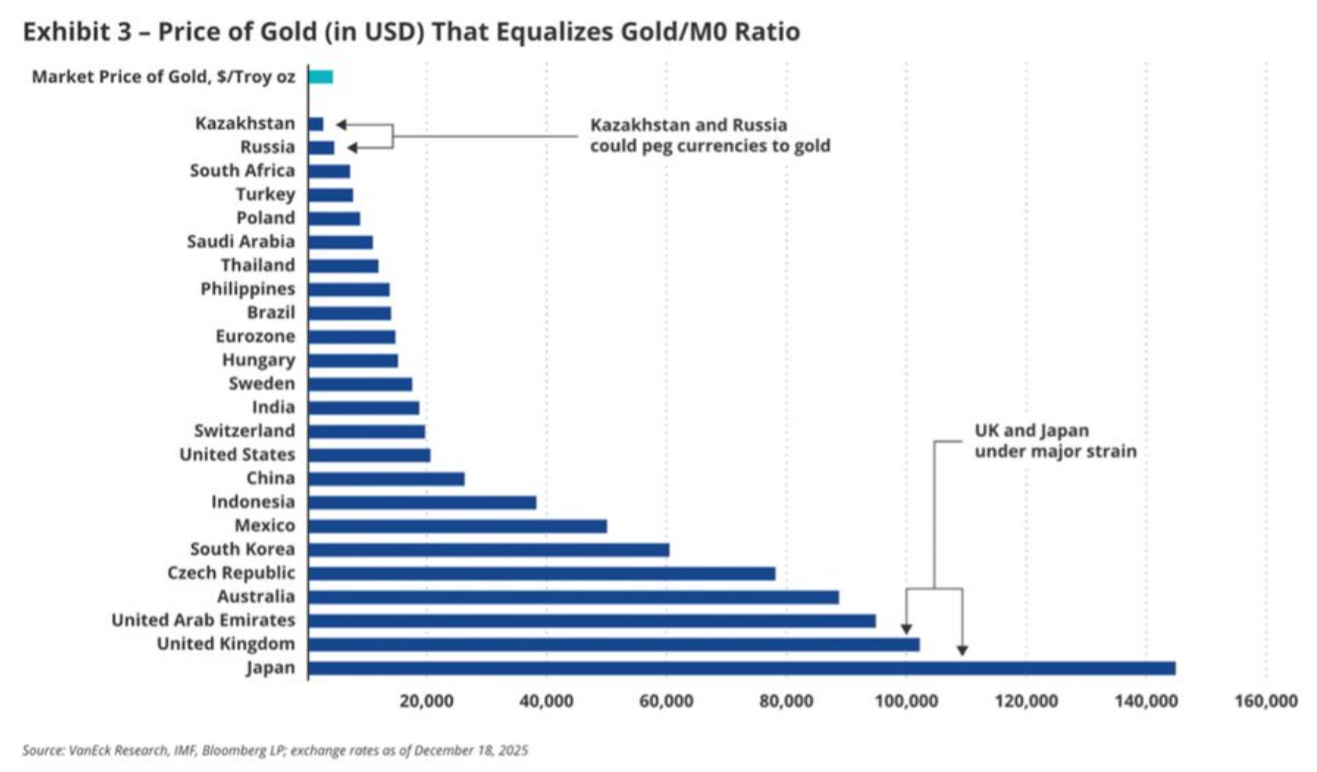

To find this implied ‘reserve price’ of gold, they employ a relatively simple calculation: They divide money liabilities by known sovereign gold reserves.

The analysts used two specific definitions of money for this calculation, because “the definition of ‘money’ keeps expanding during crises.”

First, they calculate M0, or base money. “This is physical currency plus bank reserves,” they said. “In classic bank runs, this is the money people demanded.”

The second category is M2, or broad money. “This adds savings deposits and money market funds,” the analysts wrote. “In modern financial crises, like 2008 or 2020, this is the broader liquidity the system tries to protect.”

When they calculate the implied price of gold based on the money liabilities of the world’s major central banks, weighted by their share of daily foreign exchange turnover, the valuations are very dramatic.

“If gold were to back M0 (Base Money), it would need to trade at $39,210 per ounce,” the analysts said. “If gold were to back M2 (Broad Money), it would need to trade at $184,211 per ounce. These figures represent the price required to ‘cover’ the outstanding money liabilities in a scenario where gold becomes the primary reserve asset again.”

The VanEck analysts warn that while these two figures represent global averages, they do not address the deep disparities between nations. “The ratio of money printed to gold held reveals which countries are ‘levered’ and which are safe,” they said.

The most heavily levered nations include some of the world’s most developed economies, such as the United Kingdom and Japan, which have printed massive amounts of money relative to their sovereign gold holdings. “In a reset scenario, their currencies would be under the most pressure,” they wrote. “For example, Japan's implied gold price for M2 is roughly $301,000 per ounce, while the UK's is roughly $428,000.”

VanEck’s baseline group includes the United States and the Eurozone. “The US implied M2 price is roughly $85,000, while the Eurozone is around $53,000,” the analysts noted.

The third group – the solvent – includes developing economies with large gold holdings relative to their M0 and M1 money supplies. “Emerging Markets like Russia and Kazakhstan arguably have enough gold to back their money supplies at much lower valuations,” they said. “This highlights a shift where certain Emerging Markets are becoming more fiscally defensive than their Developed counterparts.”

Far from an academic exercise, VanEck wrote that these calculations truly matter in 2026 – because the world has definitively entered into an era of fiscal dominance.

“Developed markets are struggling with high government debt, forcing central banks to ‘print’ more money to keep the system liquid,” they said. “As the pile of paper money grows toward infinity, the value of the finite asset, gold, must theoretically rise to keep up.”

The Emerging Markets Bond team was careful to point out that they do not expect the U.S. dollar to “suddenly lose its status as a reserve currency.” Rather, they see a gradual evolution “toward a multipolar world in which the dollar shares that role with gold and the bonds of fiscally disciplined emerging markets.”

KitcoNews