Gold Miners’ Q3’21 Fundamentals

The gold miners’ stocks are surging dramatically, despite the Fed starting to slow its epic money printing. Heavy gold-futures selling exhausted itself leading into this QE taper, paving the way for strong mean-reversion rebounds in gold and gold stocks. This sector’s latest Q3’21 earnings season is just wrapping up, revealing whether gold miners’ underlying fundamentals still support much-higher stock prices ahead.

The GDX VanEck Gold Miners ETF remains this sector’s dominant benchmark, parlaying an early first-mover advantage into an insurmountable lead. Its $14.5b of net assets mid-week ran a colossal 27.5x larger than the next-biggest 1x-long major-gold-miners-ETF competitor’s. Though GDX has blasted 17.3% higher in the last six weeks, gold-stock psychology remains bearish following a violent capitulation shakeout.

Earlier this year traders were warming on gold stocks. Between early March to mid-May, GDX powered 28.4% higher in a solid young upleg. These are well worth trading, earning fortunes for contrarians tough enough to fight the herd. That was the fifth upleg of this secular bull, and its first four averaged awesome 99.2% GDX gains over 7.6 months! How many other stock sectors can fairly-regularly double your money?

But gold’s parallel driving upleg was derailed in mid-June after Fed officials started hinting at future rate hikes and slowing quantitative-easing bond monetizations. That fueled heavy-to-extreme gold-futures selling in anticipation of Fed tightening, a sell-the-rumor taper tantrum. Several bouts of that hammered gold lower, and gold stocks were simply collateral damage. GDX was torpedoed down 27.1% by late September.

They were screaming buys around that capitulation climax, as I explained in multiple essays leading into and shortly after it. But the vast majority of traders are momentum players, they can’t buy low because they refuse to follow sectors when out of favor. But after being tried and tested, gold stocks are rising back to their feet and will be heard. With mounting gains accelerating, what a great time for quarterlies!

Following these fundamental reports is exceedingly-important for speculators and investors. The fairly-rare hard data they offer really cuts through the obscuring and misleading fogs of herd sentiment. That highly-emotional greed and fear is fueled exclusively by gold stocks’ recent technical trends, not how they are actually faring operationally and financially. But these core fundamentals reveal where they ought to go.

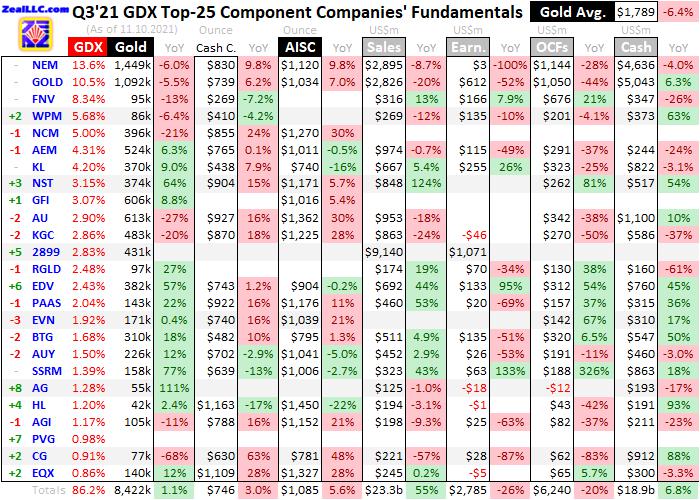

So for 22 quarters in a row now, I’ve painstakingly analyzed the latest results released by the top 25 GDX component stocks. They accounted for 86.2% of this ETF’s holdings midweek, and include the world’s largest gold miners. Their Q3’21 results have mostly been released, with securities laws requiring US companies to report by 40 days after quarter-ends. But Canada allows up to 45, making for some stragglers.

This table summarizes the operational and financial highlights from the GDX top 25 during Q3’21. These gold miners’ stock symbols aren’t all US listings, and are preceded by their rankings changes within GDX over this past year. The shuffling in their ETF weightings reflects changing market caps, which reveal both outperformers and underperformers since Q3’20. Those symbols are followed by their current GDX weightings.

Next comes these gold miners’ Q3’21 production in ounces, along with their year-over-year changes from the comparable Q3’20. Output is the lifeblood of this industry, with investors generally prizing production growth above everything else. After are the costs of wresting that gold from the bowels of the earth in per-ounce terms, both cash costs and all-in sustaining costs. The latter help illuminate miners’ profitability.

That’s followed by a bunch of hard accounting data reported to securities regulators, quarterly revenues, earnings, operating cash flows, and resulting cash treasuries. Blank data fields mean companies hadn’t reported that particular data as of the middle of this week. The annual changes aren’t included if they would be misleading, like comparing negative numbers or data shifting from positive to negative or vice versa.

Despite Q3’s challenges led by those gold-futures selloffs and mounting inflationary cost pressures, the GDX gold miners still earned fat profits. They generally enjoyed growing production, which helped offset lower average gold prices. Compared to the raging inflation the Fed’s radically-unprecedented QE4 money printing unleashed, the gold miners largely held the line on costs. They are still thriving fundamentally!

After decades of intensely studying and actively trading gold stocks to earn fortunes, my enthusiasm for this high-potential contrarian sector hasn’t waned. But I’ve never liked the great majority of the major gold miners. Gold stocks are defined as majors, mid-tiers, or juniors based on their quarterly outputs. The larger majors mine 250k+ ounces per quarter, medium mid-tiers 75k to 250k, and smaller juniors under 75k.

While the larger majors dominate GDX, they chronically underperform. A dozen producing 250k+ ounces in Q3 account for 56.5% of GDX’s total weighting. I wouldn’t touch five of those adding up to 32.8% with a ten-foot pole, due to their long sorry histories of disappointing performance for various reasons. I only have positions in three of these 12 GDX majors, and rarely situationally trade two more. The majors are problematic.

Already operating at very-high gold-production bases, they endlessly struggle to grow their outputs. Their organic growth rarely exceeds depletion, so occasional acquisitions are necessary to temporarily boost production. Yet even when that happens, the massive market capitalizations of most gold majors really retard their stock-price gains. Mid-tier and junior gold miners have superior fundamentals, growth, and upside.

The GDX top 25 collectively mined 8,422k ounces of gold in Q3’21, which climbed 1.1% year-over-year. While that sounds solid, it is really comparatively-weak. Every quarter the World Gold Council publishes the best-available global gold fundamental data in its fantastic Gold Demand Trends reports. They are essential required reading for gold-stock traders, detailing how worldwide gold supply and demand are shifting.

The WGC’s latest Q3’21 GDT recently reported that global gold mined supply surged 4.4% YoY to 959.5 metric tons in Q3. The GDX top 25 only achieved a quarter of that growth, mostly because of collapsing outputs in five majors. Newmont, Barrick, Newcrest, AngloGold, and Kinross reported ugly Q3’21 production falling-to-plunging 6.0%, 5.5%, 21.2%, 26.8%, and 19.9% YoY! That was way less gold mined.

Their total Q3’21 outputs fell 13.1% or 606k ounces from Q3’20! These five struggling majors account for 34.8% of GDX’s total weighting, really hurting this ETF’s performance and potential. Excluding them, the rest of the GDX top 25 enjoyed powerful output growth of 701k ounces which soared 19.0% YoY! That is even understated a bit, because another major Harmony Gold fell out of the GDX-top-25 ranks this year.

It contributed 314k ozs to Q3’20’s GDX-top-25 output total, then bucked the struggling-major trend for a change to produce 414k in Q3’21 that weren’t included in its total. Harmony ranked as 26th this week, just missing the cutoff. Big production growth at major scales is unusual, typically driven by one-off events and never sustainable. Northern Star led the majors last quarter clocking in at huge 64.2% output growth!

But that’s solely because this Australian miner acquired its competitor Saracen during this past year. If these two companies’ Q3’20 production is added together, the merged company actually saw output slump 2.2% YoY in Q3’21. The major gold miners can’t achieve big output growth unless they buy mines or entire companies. And that only masks depleting production for four quarters, as late-2018 mega-mergers proved.

While a handful of smaller major gold miners have consistently achieved excellent production growth, the larger majors are mostly a big drag on GDX’s performance. They command about half its total weighting, which is based on companies’ market caps. That severely hobbles this dominant gold-stock ETF’s upside potential. Speculators and investors can do far better handpicking fundamentally-superior mid-tiers and juniors.

While their smaller market caps relegate them to lesser importance within GDX, that really amplifies their gains when gold is running. Those dozen majors of GDX averaged $15.7b market capitalizations midweek. Newmont and Barrick alone, which dominate GDX at 24.0% of its total weighting, averaged gargantuan $41.4b market caps! Stocks that large are harder to bid higher, having supertanker-like price inertia.

Meanwhile the other 13 GDX-top-25 components averaged $7.0b market caps. And those were heavily skewed by Franco-Nevada and Wheaton Precious Metals. The former royalty company has long been the most-overvalued major gold stock, trading at crazy-high prices relative to the gold it sells and profits it earns. The latter is a gold and silver streamer which is a much-better buy. Their market caps averaged $23.8b.

Without them, the rest of the GDX top 25’s market caps are way smaller averaging just $4.0b. Note in the table this sweet spot is where most of gold miners’ production growth was concentrated! Any given capital inflows as traders return will catapult smaller gold stocks higher way faster than larger ones. While GDX is the go-to destination for gold-stock portfolio exposure, it is burdened by much gold-major deadweight.

Long-term gold-stock price levels ultimately depend on miners’ profitability, which is directly driven by the difference between prevailing gold prices and gold-mining costs. In per-ounce terms these are generally inversely proportional to gold production. That’s because gold mines’ operating costs are largely fixed during planning stages. Their designed throughputs limit the amounts of gold-bearing ore they can process.

That doesn’t change quarter to quarter, and requires about the same levels of infrastructure, equipment, and employees. The only real variable is the ore grades run through the fixed-capacity mills. Richer ores yield more gold ounces to spread the big fixed costs of mining across, lowering unit costs which boosts profitability. With the GDX top 25’s collective gold output growing 1.1% YoY, unit costs should’ve retreated.

Cash costs are the classic measure of gold-mining costs, including all cash expenses necessary to mine each ounce of gold. But they are misleading as a true cost measure, excluding the big capital needed to explore for gold deposits and build mines. So cash costs are best viewed as survivability acid-test levels for the major gold miners. They illuminate the minimum gold prices necessary to keep the mines running.

That slightly-higher output didn’t drive the GDX top 25’s average cash costs lower last quarter, as they climbed 3.0% YoY to $746 per ounce. As I read through quarterly reports, I was struck by the number of times inflationary cost pressures were mentioned. Like everything else, gold-mining costs are relentlessly climbing thanks to the vast deluge of central-bank money printing. Labor, supplies, and fuel were called out.

Nevertheless, the gold miners mostly held the line on costs. Their average was dragged higher by the outlier Hecla Mining, which reported extreme $1,163 cash costs. Excluding this long-struggling miner, the average fell to $724 making for a slight year-over-year decline. The GDX gold miners are doing a better job of realizing efficiencies and offsetting rising costs than most other industries, which is impressive.

All-in sustaining costs are far superior than cash costs, and were introduced by the World Gold Council in June 2013. They add on to cash costs everything else that is necessary to maintain and replenish gold-mining operations at current output tempos. AISCs give a much-better understanding of what it really costs to maintain gold mines as ongoing concerns, and reveal the major gold miners’ true operating profitability.

A few weeks ago before Q3’21’s earnings season, I expected GDX-top-25 average AISCs to retreat on the order of 3.5% YoY due to output growth. I wrote a preview essay explaining that the WGC’s global gold-mining data shows Q3s average amazing 6.7% sequential production growth from Q2s! I cut that in half to be conservative, looking for 3.5% last quarter. The GDX-top-25 output grew 2.9% QoQ despite the majors.

But unfortunately the GDX top 25’s average all-in sustaining costs still surged 5.6% YoY to $1,085 in Q3’21! That proved the highest in the 22 quarters I’ve been working on this research thread. That was certainly disappointing, and the higher AISCs were widespread. Even without Hecla’s outlying $1,450, the rest of the GDX top 25 still averaged $1,065. That reflected the rising impact of inflation on gold mining.

The major gold miner Agnico Eagle had one of the better explanations in its latest quarterly results. They included “given rising prices for many commodities and disruptions to global supply-chains, the resulting cost pressures were gradually being pushed downstream and were starting to be reflected in the prices for a number of goods and services used”. And during Q3 “these inflationary pressures have accelerated”.

Management gave an example of “diesel prices have increased by approximately 20%” just since early August! These inflationary pressures aren’t going away, “While difficult to predict, the Company expects that these price pressures will extend into 2022, depending on when inflation conditions and global supply-chains normalize.” So AISCs are likely to keep clawing higher decoupling from production trends.

That isn’t optimal, as higher costs always erode earnings. But the gold miners are better-positioned than almost any other industry to absorb inflationary pressures with minimal impacts. Mounting inflation fears will really boost gold investment demand, driving prices higher. That will ratchet up the already-fat profits of gold miners. Today they are earning money hand over fist, facing minimal margin squeezes like other sectors.

Subtracting the GDX-top-25 average AISCs from prevailing gold prices yields a great industry proxy for unit earnings. Despite those bouts of heavy gold-futures selling on Fed-tightening fears, gold still fared quite well in Q3’21 averaging $1,789. That was down a modest 6.4% YoY, ending a magnificent nine-quarter streak of higher gold prices. Still gold remained far higher than even those elevated $1,085 AISCs.

Despite being pinched by both lower gold prices and higher costs, that still yielded massive sector profits of $704 per ounce! That remained the sixth-highest ever seen, after the five preceding quarters. The peak was $884 in Q3’20, but for three full years prior to Q2’20 this metric averaged $458. Gold miners are still thriving despite the inflationary cost pressures they face. And gold-price gains should outpace inflation.

Ultimately gold will follow the money, which has exploded under this profligate Fed. In just 20.3 months since March 2020’s pandemic-lockdown stock panic, this central bank has mushroomed its balance sheet by a radically-unprecedented and terrifying 106.2% or $4,416b! And despite finally starting to slow that ballooning with the QE4 taper, another $420b is still coming if the Fed sticks to the timeline the chair laid out.

With vastly more money competing for and bidding up prices on far-slower-growing goods and services, inflation is raging. The more investors experience it in their own lives, and see how it erodes earnings in these Fed-QE-levitated bubble-valued stock markets, the more they will prudently diversify stock-heavy portfolios with gold. So gold-price gains should way-outpace inflation, and miners’ earnings leverage those.

On the hard-accounting front, the GDX-top-25 gold miners’ financial performances were mixed in Q3. Their total sales soared 54.7% YoY to $23.3b, which sounds incredible. But that’s way too good to be true with lower average gold prices and only slightly-higher production. That’s entirely because giant Chinese miner Zijin Mining finally started reporting a few quarterly datapoints in English, including $9.1b of sales!

Having Zijin included in GDX has irritated me for years, not just because its financial reporting is the worst I’ve ever seen. Zijin is overwhelmingly a copper, zinc, and iron-ore miner that has no place in a gold-miner ETF. Assuming the numbers Zijin is reporting are righteous, its gold production accounted for only about 1/12th of its revenues in Q3’21! Ex-Zijin, the GDX-top-25 sales slumped 5.9% YoY right in line with gold.

The bottom-line accounting earnings reported to securities regulators were way weaker, falling 26.5% YoY to $2,785m. They looked far worse without Zijin’s huge $1,071m contribution, plummeting 54.8% YoY to just $1,714m. But the plurality of that came from GDX’s biggest component Newmont, which has underperformed operationally for years. Its earnings cratered a horrific 99.6% YoY to just $3m in Q3’21!

That alone accounted for 40% of the ex-Zijin profits plunge. $571m of that $836m decrease resulted from Newmont writing down equipment and assets at a for-sale project in Peru. A year earlier in Q3’20, other GDX components also reported large non-cash gains exceeding $416m. So the collapse in accounting profits over this past year is heavily distorted on both ends by unusual items, it doesn’t reflect mining operations.

They generated $6,240m of operating cash flows for the GDX-top-25 gold miners in Q3’21, which fell by 19.9% YoY. When digesting all those financials, I didn’t find any obvious explanation why other than lower gold prices. But Newmont and Barrick were to blame, the deadweight commanding nearly 1/4th of GDX’s total weighting. Their OCFs alone cratered $1,261m or 36.5%! The other gold miners fared way better.

Excluding those two perpetually-underperforming super-majors, the rest of the GDX top 25 saw operating cash flows only retreat 6.6% YoY to $4,046m. That’s right in line with the lower average gold prices, no big deal at all. But this entire group’s cash treasuries still climbed up 6.8% YoY to $18.9b. With coffers flush and gold stocks running again, a new wave of mergers and acquisitions is just getting underway.

Leading it was late September’s shocking announcement that Agnico Eagle will soon buy Kirkland Lake Gold! The latter is the best major gold miner by far, with strong consistent production growth and some of the lowest and most-profitable AISCs in the industry. AEM shareholders got a steal, not even bothering to offer a premium for KL. Sadly KL shareholders, which include me, are being robbed blind in this terrible deal.

Since the larger major gold miners can’t grow their massive outputs organically, they have to buy entire companies to maintain production. The biggest beneficiaries will be the smaller mid-tier and junior gold miners. An example is Newcrest just declaring it is buying out Pretium Resources. The longer this gold-stock upleg persists, the more frenzied gold-stock merger-and-acquisition activity will get attracting in new traders.

The gold miners’ strong fundamentals reveal their stocks are still deeply-undervalued. The GDX top 25’s average trailing-twelve-month price-to-earnings ratios ran 30.6x midweek, but that was skewed high by a couple of 100x+ outliers. Without them, the rest averaged just 19.8x. Fully five were dirt-cheap trading at single-digit-P/E valuations, while another eight were in the teens. Gold stocks are super-cheap absolutely!

If you aren’t deployed yet, you should get on that. This sector’s upside potential in coming months and years is huge. These neglected contrarian plays are already earning fat profits and trading at super-low valuations. As gold powers higher on the vast torrents of new fiat money central banks are spewing, gold-mining earnings will amplify gold’s gains like usual. Gold stocks are the best place to be in inflationary times.

If you regularly enjoy my essays, please support our hard work! For decades we’ve published popular weekly and monthly newsletters focused on contrarian speculation and investment. These essays wouldn’t exist without that revenue. Our newsletters draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks.

That holistic integrated contrarian approach has proven very successful. All 1,247 newsletter stock trades realized since 2001 averaged outstanding +21.3% annualized gains! Today our trading books are full of great fundamentally-superior mid-tier and junior gold, silver, and bitcoin miners to ride their uplegs. This week their unrealized gains are already running as high as +87.9%. Subscribe today and get smarter and richer!

The bottom line is gold miners continued to thrive fundamentally in Q3, despite heavy gold-futures selling on Fed-tightening fears. The GDX top 25 modestly grew their gold production overall, even though some larger majors struggled. While costs still rose on inflationary pressures, they stayed far below prevailing gold prices making for hefty profits. These will amplify gold’s gains as its bull follows the money printing higher.

While GDX includes many great gold miners, its upside potential is retarded by deadweight majors that dominate its weightings. They are still consistently failing to grow their outputs from high bases, and their larger market caps exert heavy price inertia. So the best gold-stock gains will continue to be won in the smaller fundamentally-superior mid-tier and junior gold miners. They will far-outperform the hobbled GDX.

Adam Hamilton, CPA

Copyright 2000 - 2021 Zeal LLC (www.ZealLLC.com)

*******