It’s Not As It Appears!

As equities continued to rise during the advance into the 2007 top, I screamed from the roof tops that it was a bear market advance and that the efforts to prop the markets up only served to make matters worse. That certainly proved to be the case as those efforts resulted in the worst financial crisis since The Great Depression. Yet, as a result of the worst financial crisis since The Great Depression, the response to that event was the massive bailouts and even more of the same things that created that event in the first place. Seriously, think about it. Is it remotely reasonable to respond to the worst financial crisis since the 1930’s with more of the same actions that created that crisis in the first place? Does this really make sense? Ever since the rally out of the 2009 low began, I have explained that it is a bear market advance and that the longer the rally extends, the more dangerous it will become. The rally out of the 2009 low has now extended to the point that it is the longest cyclical advance since the inception of the Dow Jones Industrial Average in 1896.

On the surface, with price at new highs and with this being the longest cyclical advance since 1896, how in the world can this be a bear market rally? Yeah, I know, that sounds crazy doesn’t it? Keep reading. I’ll explain. First, let me say that every indication is that the economy and the secular bull market peaked in 2000. You will see proof of that with some very basic, but indisputable evidence presented below. The bear market rally out of the 2002 low was pushed to new highs simply as a result of the liquidity infusions and smoke and mirrors tricks orchestrated by the money masters. The advance out of the 2009 low is Take II on steroids. The confusing concept here is that of a secular bear market with price at a new high. Let’s now examine the supportive evidence that this is a bear market rally. I’m going to show you high level, very basic, but indisputable evidence that further confirms this view.

First, let’s look at volume. In Technical Analysis of Stock Trends, Edwards and Magee write, “Volume goes with the trend. Those words, which you may often hear spoken with ritual solemnity but little understanding, are the colloquial expression for the general truth that trading activity tends to expand as price moves in the direction of the prevailing Primary Trend. Thus, in a Bull Market, volume increases when prices rise and dwindles as prices decline; in Bear Markets, turnover increases when prices drop and dries up as they recover.”

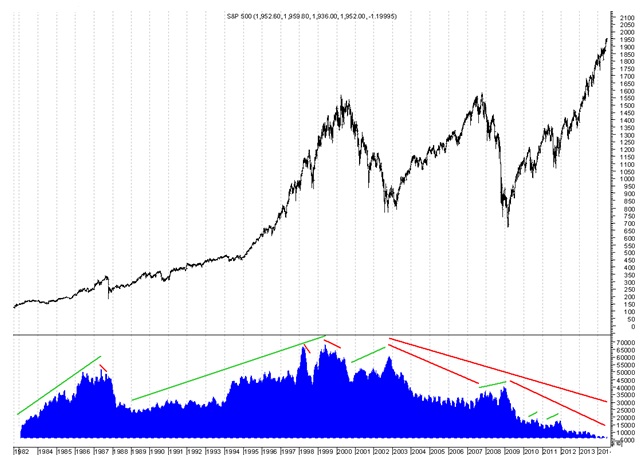

With these volume characteristics in mind, I want to walk you through the first chart below. This is a chart of the S&P500 with volume bars at the bottom in blue. Starting back in 1982, look how volume expanded with price, per the green trend lines above the volume bars, as the secular bull market pushed into the 1987 top. As the 1987 price top was being made, there was a non-confirmation by volume, per the small red trend above the volume bars, which led to the decline into the 1987 low. As the advance out of the 1987 low began, volume was a little light, but by 1989 volume began expanding once again and it continued to do so all the way into mid-1999. There was a small non-confirmation in conjunction with the 1998 top, which again is noted in red. When I say non-confirmation, I’m simply referring to the fact that volume contracted as price moved into the final price high and in doing so, volume did not confirm the higher price high. Following the decline into the 1998 cyclical low, volume again expanded into mid-1999.

Then, once again, as price moved into the 2000 top, the contraction in volume created another non-confirmation, noted in red, which led to the 2000 secular bull market top. I want to stress the point as to how relatively short-term volume non-confirmations were seen in conjunction with the 1987, 1998 and 2000 tops, which led to the declines into the 4-year cycle lows that followed. Please, it is important to note that the volume characteristics from 1982 into the 2000 top were consistent with bull markets, per the Edwards and Magee descriptions above.

Now, note how the volume characteristics changed, following the 2000 top. As price declined into the 2002 cyclical low, volume moved up in conjunction with that decline, as is noted by the green trend line above the volume bars. Then, note the further characteristic change in that the advance into the 2007 high occurred on decreased volume and that volume increased, per the green trend line, as price moved into the 2009 low. Remember what Edwards and Magee said about volume. “.....in Bear Markets, turnover increases when prices drop and dries up as they recover.” But wait, it gets worse. Much worse! Look how the entire advance out of the 2009 low has occurred on increasingly less and less volume and the only expansions in volume, per the green trend lines, have occurred in conjunction with price declines. The price volume characteristics clearly changed in conjunction with the 2000 top and they have since been clearly indicative of secular bear market behavior.

Turning back to Edwards and Magee, they talk about the three phases of bull and bear markets and the related volume characteristics. In regard to bull markets they write, “Finally, comes the third phase when the market boils with activity as the ‘public’ flocks to the boardrooms. All the financial news is good, price advances are spectacular and frequently ‘make the front page’ of the daily papers, and new issues are brought out in increasing numbers. ..... In the last stages of this phase, with speculation rampant, volume continues to rise, but ‘air pockets’ appear with increasing frequency; the ‘cats and dogs’ (low-prices stocks of no investment value) are whirled up, but more and more of the top-grade issues refuse to follow.” While the current advance exhibits some of these characteristics, this quote is descriptive of the advance between 1997 and 2000, per the final volume expansion. Does anyone remember the dotcom bubble, the tech bubble, the Nasdaq bubble and the associated craziness? The key here is volume continues to rise. Obviously volume is not and has not been rising. There was an indisputable change in volume behavior from bullish to bearish in conjunction with the 2000 top. In spite of the fact that price moved to a new high in 2007 and now to yet another new high in conjunction with the longest cyclical advance in stock market history, these rallies have absolutely NOT occurred within the context of bullish volume behavior.

Now I want to present you with another piece of evidence. The Velocity of M2. I know there have been some articles floating around and various discussions about this data, but I have not seen any of those articles that put it in this context. For clarification sake, basically, the velocity of money is the rate at which money is exchanged from one transaction to another. M2 is a category within the money supply that includes M1 in addition to all time-related deposits, savings deposits, and non-institutional money-market funds.

Now, rather than rely on some PhD, economist, politician, stock broker or some talking head on TV to tell us that everything is fine, I ask that you simply apply a little good ole fashion common sense. In light of the volume characteristics presented above and the collapse in the Velocity of M2, is it really believable that we could have a recovering economy or that we could be operating within a secular bull market?

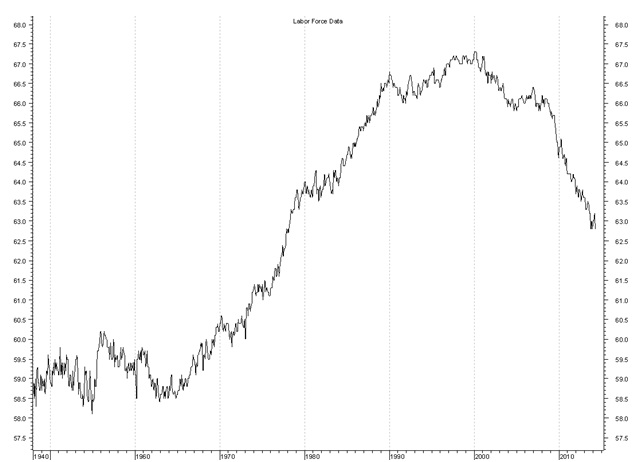

Let’s look at another little piece of data and at another chart that has been floating around. That being, the Labor Force Job Participation rate. Here too, I want to put this chart in context with the rest of this data. The labor force is defined as the sum of employed and unemployed persons and the labor force participation rate is the labor force as a percent of the civilian non-institutional population. I have included this chart below.

Now, considering the volume characteristic, the M2 velocity data presented above, along with the shrinking Labor Force, which has collapsed back to 1977-78 levels, when the population was some 87 million less people in the U.S. than today, is it really believable that such a contraction in the labor force rate could be occurring within a recovery economy and a secular bull market?

I don’t care who says this is a secular bull market or that there is an economic recovery, they are mistaken or they are lying. Secular bull markets occur with rising volume as participation in the stock market increases and there is job growth as well as an increase in the rate in which money changes hands. This should be common sense. It’s really not that complicated. This is not the environment in which we are operating. That environment ceased to exist in 2000 and the money masters have been fighting it ever since. The data clearly shows that this is not a secular bull market and that it is not a recovering economy. No matter how hard one tries to justify the price advance with some wild hypothesis that volume doesn’t matter or that Velocity of Money or that the Job Participation Rate is somehow no longer a factor, if you look at this data collectively and if you are honest with yourself, you really can’t justify it. To try to do so in one’s mind is to play mind games with one’s self in an effort to explain the insanity and the illusion of a bull market and a recovering economy.

Think people! Think! Look at the data. It’s all an illusion…and if you look at the data for what it is, it exposes the illusion. As hard as it may be to believe, the data clearly tells us that we have been operating within a secular bear market since 2000. The reason people are confused by this is that they automatically want to equate higher prices with bull markets and recovering economies and then they try to justify what they see by saying that volume and the other factors no longer matter. Like the advance out of the 2002 low, the advance out of the 2009 low is a bear market rally that has been fueled to new highs simply as a result of the liquidity infusion practices of the money masters. Did the fact that price moved to a new high in 2007 change the underlying issues with the market then? Did it prevent the collapse into the 2009 low? Was the data presented here not also relevant at the 2007 top? Just, as the efforts to compensate for the underlying economic and market deficiencies with liquidity infusions only served to make matters worse and ultimately resulted in the worst financial crisis since The Great Depression, this time is no different and apt to be ever bit as bad, if not worse.

This all said, as extreme as this cyclical advance has become, I have grown increasingly concerned about the extremity of the reversion to the mean, once this cyclical advance peaks. You cannot artificially inflate, manipulate and stretch the natural cycles of a market indefinitely. The reversion to the mean will occur, it always has. The advance into the 2007 top was the second longest cyclical advance in stock market history and it occurred within what I believe was a secular bear market, per the data presented here, but in spite of the efforts to negate that cycle, the reversion to the mean was finally recognized and when it was it was ugly. However, the decline into the 2009 low was purely financial. I fear that we won’t be so lucky this time. The social and political landscape is different. The potential consequences, when this all comes unwound, is scary. Can you imagine a financial crisis as bad or worse than that seen in association with the decline into the 2009 low and this time around we actually see banking failures? Or, what if the benefit checks or the EBT cards don’t go out to what I understand to be approaching nearly 50 million? Add to that the new open border issue with the mass immigration that is taking place and the risk to the system from a financial collapse becomes parabolic. But wait, then we have the new threats from ISIS and even Dick Cheney warning of an even worse event than that of 911. I’m telling you, we are seeing the ingredients for one hell of a mess. Again, the reason I say this is solely based on the extremity of this cyclical advance and knowing market history, we are apt to see an equally extreme unwinding. Knowing this and looking at the news you quickly start to get the picture.

There is however, some good news in all of this. I have gone back to 1896, which is the inception of the Dow Jones Industrial Average and I have identified a set of statistical based common denominators that have been seen at every major top. I call these common denominators my DNA Markers. I used these DNA Markets to identify the stock market top in 2000 and in 2007. I also used other such DNA Markers to identify the housing top in 2005, the commodity and oil top in 2008 and the top in gold in 2011. While I have maintained that the rally out of the 2009 low has been a bear market rally, I have also maintained that it is likely to continue to press higher until these statistical based DNA Markers are seen. I can tell you that at present, these markers are not in place. Therefore, any weakness at this juncture is expected to be temporary and to be followed by higher prices. I can also tell you that given the extremity of this cyclical advance and the underlying technical and economic conditions in which it has occurred, I worry about the possibility of a normal correction being more than the market can bear. In spite of that concern, the statistical based DNA Markers, nonetheless, suggest that this is not likely. Rather, odds suggest that we should see the statistical based DNA Markers present themselves in association with this top, just as they have at every major top since 1896. It is the appearance of these DNA Markers that I continue to monitor in my research letters at Cycles News & Views. Once the setup is in place, the money masters will have lost “control,” or should I say the perception of control, and at that point all bets are off. Literally anything could happen.

********

If you are interested in such research and the developments surrounding the DNA Markers and the associated expectations, that research it is available at www.cyclesman.net.