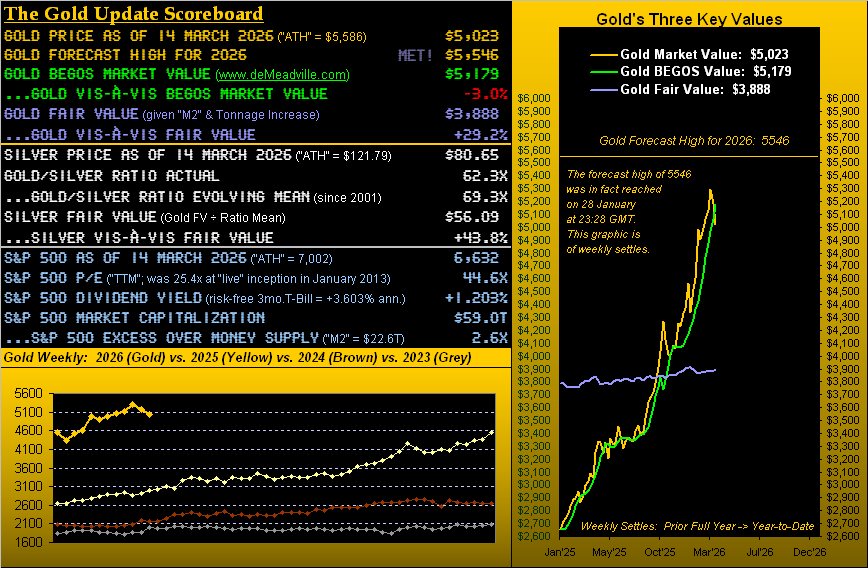

Two Weeks of War Profound; Two Weeks of Gold Gone Down

Gold just recorded a second consecutive down week for the first time since a trifecta which respectively ended this past 24 and 31 October, plus 07 November.

Fast forward to two Fridays ago on “War Eve” (27 February), when Gold settled at 5296, price then proceeding to post a -2.2% net loss through the war’s first week to close at 5181. And now through the war’s second week, Gold recorded another net loss of -3.1% in settling yesterday (Friday) at 5023.

Given the outbreak of war, Gold in decline is contra to conventional wisdom wherein ’tis assumed price instead must soar — which it initially did albeit ever so briefly — in an eight-hour COMEX run from the aforementioned 5296 to as high as 5434 on Monday, 02 March. However, price since hasn’t been higher, indeed recording from the war high of 5434 to this past week’s low of 5014 an encompassing loss of -7.7%. And from Gold’s All-Time High (5586 on 29 January), price today is lower by -10.1%.

“Still, a -10% correction seems like a lot, eh mmb?”

War or otherwise, Squire, Gold has gotten far ahead of valuation. And lest we forget, from September 2011 into December 2015, Gold “corrected” by some -46%. But as our readers know ad nauseam, this is exactly how Gold negatively reacts to geo-political spikes, price now once again lower than prior to the onset (then 5296) of this war by -5.2%. “Who wudda thunk it…” right?

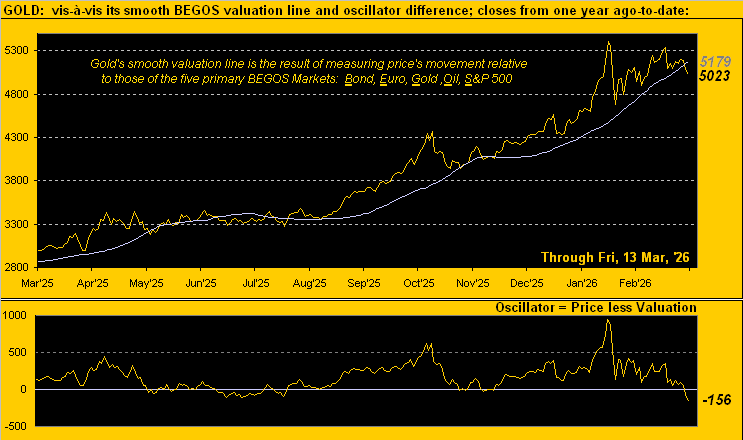

‘Course as we’ve written, regressing the price of Gold to geo-politics is at best an abstract guess. But mathematically regressing Gold to Dollar debasement across five decades (as rightly adjusted for the increase in the supply of Gold itself) is a proper, proven measure. And as thus shown in the opening Gold Scoreboard, price today at 5023 is +29.2% above the broad Fair Value measure of 3888.

Near-term however, per Gold’s BEGOS Market Value of 5179, price is -3.0% low, indeed by some -156 points per the year-over-year chart below, reversion to such mean as inevitably is seen:

Indeed, Gold’s most recent 73-trading-day run above its BEGOS valuation ranks fourth-longest century-to-date, (the longest being just last year for an 88-trading-day stint). But come Gold’s All-Time High (5586), price then was +24.4% above such valuation, a record high-side deviation since 2001; (for those of you scoring at home, the century-to-date low-side deviation was -15.5% on 15 April 2013 in the midst of Gold’s aforementioned -46% “correction”).

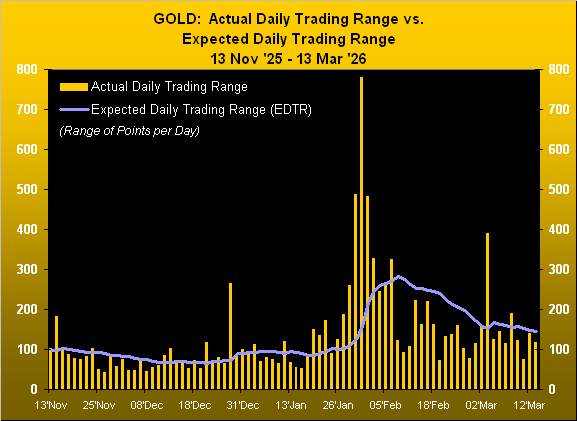

Either way, with back-to-back down weeks for Gold having become a bit of a rarity, let’s next go to Gold’s weekly bars from a year ago-to-date astride the parabolic dots. And clearly there’s little wiggle room for Gold to gain another blue dot of the parabolic Long trend. Present price (5023) is but +51 points above the flip-to-short level (4972) with Gold’s expected daily trading range now 143 points and the weekly 313 points:

Too, as Gold’s uptrend energy weakens, range is narrowing. The following graphic from four months ago-to-date shows us price’s actual daily trading range (bars) versus the expected daily trading range (line). Gold’s actual range has exceeded the expected range just once in the past eight trading days, the expected range itself in decline. “War? What war?”:

Contrary to Gold’s narrowing range, that for the S&P 500 is widening in worry over war’s woes and the potential economic fallout thereto. The S&P having peaked at a record high of 7002 on 28 January, the Index today at 6632 marks a -5.3% decrease. Moreover, through these first 49 trading days of 2026, the S&P’s net decline to this point — whilst only -0.5% — nonetheless ranks fourth-worst century-to-date for any opening 49-trading-day stint. To be sure, through 25 full trading years thus far this century, the S&P has recorded just seven downers … but that as a gentle reminder to you WestPalmBeachers down there means the stock market doesn’t always go up. And as we oft update, the S&P’s price/earnings ratio (again per the opening Scoreboard) is now 44.6x (trailing-twelve months’ method) with a dinky yield of 1.203% versus 3.603% risk-free from the annualized three-month U.S. T-Bill.

Meanwhile, the Economic Barometer — ratchety as ’tis become — still is maintaining an upside bias. 15 metrics came into the Baro this past week, 10 of which equaled or bettered their period-over-period performance. The best of the bunch were February’s Existing Home Sales which beat consensus and had January’s level revised higher. ‘Course the real stinker was the severe downward revision to Q4’s Gross Domestic Product (annualized growth pace) from initially +1.7% to only +0.7%. Ouch…

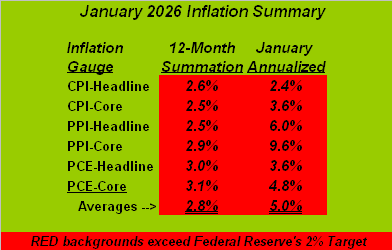

Note therein the Fed head: whilst he steps down from the Chairmanship in mid-May, on the Board of Governors he’s destined to stay. But his departure in May may be timely so as to avoid stagflation’s sway … should it come that way. Below is our completed summary of January inflation with again every calculated category in red, i.e. above the Federal Reserve’s desired target for 2% inflation. Thus, must the Fed raise? Just a passing thought…

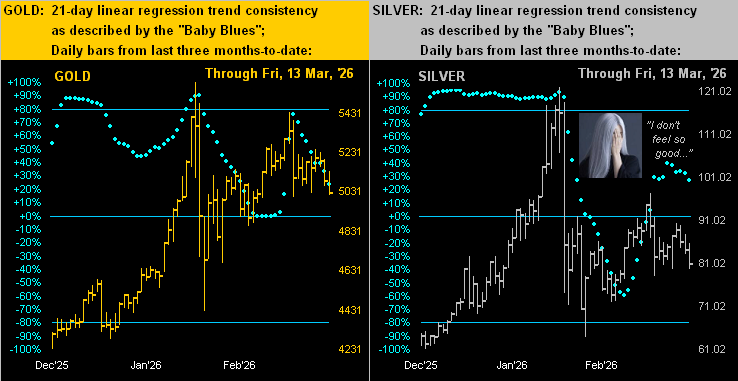

As for the U.S. Dollar, ’tis (as is typical) getting the war bid, the “Dixie” re-achieving the 100 level yesterday for the first time since last 25 November, even as Oil on balance also has moved higher. Thus as we noted earlier, whilst Gold remains in an uptrend, ’tis weakening. Specifically, said trend is the 21-day linear regression direction, which by the panel next on the left is positive given the “Baby Blues” are still above 0%, but waning as the Blues are falling by the day. As for Silver on the right, the rightmost erraticity of her normal “Baby Blues” consistency is producing an uneasy motion sickness: poor ol’ Sister Silver!

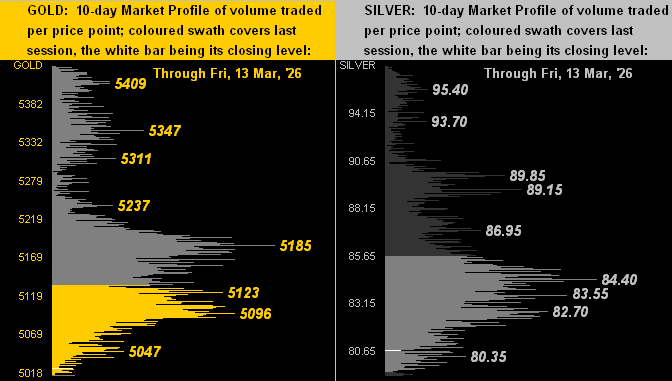

Too, the wartime weakening in the precious metals’ prices finds them nearly at the base of their respective 10-day Market Profiles for both Gold (below left) and for Silver (below right). Notable volume-dominant prices — almost all resistive — are as labeled:

So with Gold on the wane, we go to the stack … (but hardly in vain):

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 5586 (29 January 2026)

2026’s High: 5586 (29 January)

Gold’s All-Time Closing High: 5411 (28 January 2026)

Trading Resistance: notables as labeled in the Market Profile

10-Session “volume-weighted” average price magnet: 5181

Gold’s BEGOS Market Value: 5179

Gold Currently: 5023, (expected daily trading range [“EDTR”]: 143 points)

Trading Support: none notable by the Market Profile

10-Session directional range: down to 5013 (from 5432) = -419 points or -7.7%

The Weekly Parabolic Price to flip Short: 4972

2026’s Low: 4319 (02 January)

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3888

The 300-Day Moving Average: 3706 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

To wrap — warfare an ongoing wildcard — ‘twould otherwise appear we’ll soon see Gold slip sub-5000 and the parabolic trend flip from Long to Short, certainly so were the war to show signs of winding down, even as price presently is already -3.0% below its BEGOS Market Value. Moreover, Gold now being down -10.1% from its record high can inducing buying. But at the end of the broader day — as we regularly say — Gold remains best valued by Dollar debasement. And yes, Gold by Fair Value is overly high and due for further retracement, but ’tis always important to keep some in your basement!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.