What ECB’s Tiering Means For Gold

In a key policy shift, the ECB has recently introduced tiered system of interest rates. This news isn’t of interest only to the banks keeping their reserves at the ECB. In today’s article, you’ll learn about the new instrument of monetary policy, and find out what it implies for the gold market.

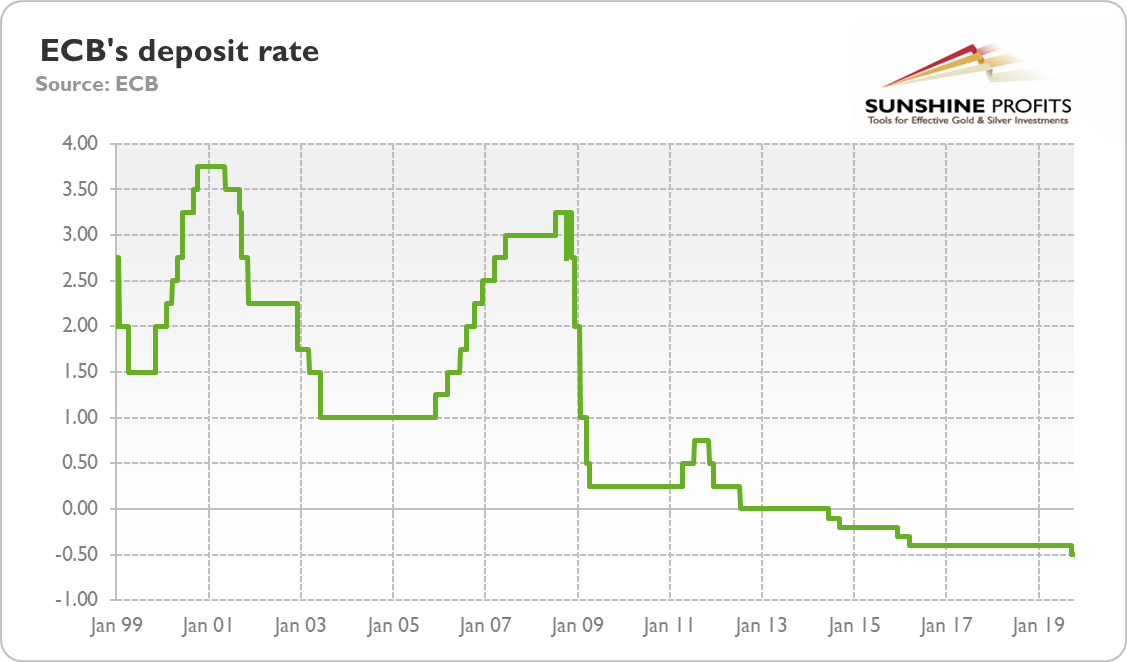

If you think that monetary policy in the United States is crazy, you are right. But in Europe, it is even stranger (and in Japan, it is really insane). As you probably remember, in September, the ECB introduced a package of measures to ease monetary policy further in the face of sluggish economic growth and subdued inflation. In particular, the Governing Council resumed quantitative easing (the bank will be purchasing €20 billion of assets monthly), eased the conditions for TLTRO operations, strengthened the forward guidance strategy, and – the crème de la crème – cut the deposit rate by 10 basis points from -0.40 to -0.50 percent, as the chart below shows. The ECB used, of course, all these instruments already in the past. What is really new is the introduction of the tiering system. How does it work and what could be its consequences for the euro area economy and gold prices?

Chart 1: ECB’s deposit rate from January 1999 to October 2019.

In the ECB’s tiered system of interest rates, a portion of bank deposits, currently set at six times their mandatory reserves, is exempted from the negative deposit rate. In other words, reserves below a threshold bear zero interest, and only excess of reserves above this threshold is subject to negative interest. The idea is to limit the harmful effects of negative interest rates on banks’ profitability. This is why most of the central banks that implemented NIRP have some form of tiering system. For example, due to tiering, the percentage of reserves subject to negative interest rates in Japan is only about 5 percent.

You might ask now why, the heck, introduce negative interest rates in the first place and then implement neutralizing measures? That’s a great question, but not for us, but for a psychiatrist. But our guess is that the ECB used the NIRP to weaken the euro, as it is the only channel through which its monetary policy somehow still works, but the banks were fed up watching their bottom lines turn red, so the ECB tiered the interest rates. Now, everyone is happy.

Really? Not so fast! The tiered system is welcome, but its introduction came too late for a sector hurt by years of ultra-low interest rates. And the relief will be too small, as it would result in annual saving of only about €2-3 billion euros for the entire euro zone banking system, around one third of the total costs of the NIRP that banks would have to bear without the tiered system.

Moreover, investors should remember that the euro area banking sector is heterogeneous, so not all banks will gain to the same extent. As German and French banks have the most reserves, they suffered from the NIRP the most and they will feel now the greatest relief. It means that the policy won’t make its hit to the maximum and that there might be some side effects.

But what is perhaps the most important is that the implementation of tiering system tightened the monetary conditions. The ECB cut deposit rates, but the money market rates rose. Why? Quite simply. Tiering means that many reserves are exempted now from negative interest rates. They are subject to the zero interest rate, and only a part of them bear interest rate at -0.50 percent. Hence, the banks’ weighted deposit rate at the ECB increased from around -0.37 to -0.25 percent. It’s not clear how the tightened monetary conditions are supposed to stimulate economic growth in the euro area. Higher interest rates should support the euro and also the yellow metal on the margin.

However, although the introduction of tiering provides some relief for commercial banks’ profitability and increases the inter-bank interest rates, it extends the possible time of the NIRP in the euro area and expands the room for even more negative interest rates in the future. As banks are now partially shielded from the disastrous effects of the NIRP, the ECB could hesitate less before the next reduction of its policy rate or delay the normalization of its monetary policy.

The sluggish growth combined with lower yields should weaken the euro and gold prices against the US Dollar in the medium term. However, given the ultra-dovish stance of the ECB and unwelcome upward pressure on the greenback, the Fed might be more inclined to follow suit and also adopt a more accommodative stance. It could cut the Federal Funds Rate as early as in October. Thus, if the ECB’s tiering translates ultimately into a more dovish Fed, it should affect gold prices positively.

If you enjoyed the above analysis and would you like to know more about the fundamentals of the gold market, we invite you to read the November Gold Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron

Sunshine Profits‘ Gold News and Gold Market Overview Editor

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

********

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017. He is a board member of the Polish Mises Institute of Economic Education, author of several dozen scientific publications (including in such periodicals as the Journal of Risk Research, Prague Economic Papers, Quarterly Journal of Austrian Economics, and Research in Economics), and a regular contributor to GoldPriceForecast.com and SilverPriceForecast.com. His two books, Money, Inflation and Business Cycles and Monetary Policy after the Great Recession, are both published by Routledge. Arkadiusz is also a certified Investment Adviser, a long-time precious metals market enthusiast, and a free market advocate who believes in the power of peaceful and voluntary cooperation of people.

More from Gold-Eagle