Goldman Sachs raises 2026 gold price target to $5,400/oz as private sector joins central bank diversification strategy

NEW YORK (January 22) The private sector is following the trend set by central banks by diversifying into gold, prompting Goldman Sachs to raise its year-end gold price target by more than 10%.

Just weeks after setting a year-end target of $4,900 per ounce, the banking giant announced on Wednesday that it was raising its December 2026 price target to $5,400 an ounce.

Goldman analysts led by Daan Struyven and Lina Thomas wrote in a note that the upgraded forecast is based on their belief that private investors who bought gold as a hedge against macro policy risks will hold these positions through the end of the year.

The analysts said that, unlike previous hedges which were tied to specific events – such as the November 2024 US election – gold positions taken to protect against risks such as fiscal sustainability are unlikely to be fully resolved this year, and are therefore “stickier.”

Emerging market central banks are “likely to continue the structural diversification of their reserves into gold,” the analysts said, adding that total central-bank buying is expected to average 60 tonnes per month in 2026.

Goldman also expects an additional 50 basis points of Fed easing in 2026, even as Western ETF holdings have increased by around 500 tons since the start of 2025, already outpacing projections based solely on U.S. interest-rate cuts.

The debasement trade is also prompting physical bullion purchases by high-net-worth families and investor call-option buying amid mounting concerns over the long-term monetary and fiscal policy trajectories in major economies, the analysts noted.

Risks to the updated forecast are “significantly skewed to the upside because private-sector investors may diversify further on lingering global policy uncertainty,” the analysts wrote. “That said, a sharp reduction in perceived risks around the long-run path for global fiscal/monetary policy would pose downside risk if it were to cause liquidation of macro policy hedges.”

The diversification trend was already very much on Goldman’s radar in 2025. In their 2026 Commodities Outlook published in late December, the investment bank wrote that gold is the best bet in the entire commodities complex, adding that if private investors join central banks in their diversification, the price could well exceed the $4,900 per ounce base case.

“The US-China AI and geopolitical power race and global energy supply waves drive our key convictions,” they wrote. “Commodity indices have delivered strong total returns in 2025 (e.g. BCOM 15%) because very strong returns in industrial and especially precious metals, which both tend to benefit from Fed cuts, have outweighed modestly negative returns in energy.”

Looking ahead, Goldman Sachs said their macro base case includes “sturdy global GDP growth and 50bp of Fed rate cuts in 2026,” which should support strong commodity returns once again.

The analysts highlight two major structural trends which they believe will drive the outlook for commodities in the coming year.

“First, on the macro side, commodities will likely remain at the center of the US-China race for geopolitical power and for tech and AI dominance,” they wrote. “Second, on the micro side, two large energy supply waves that started in 2025 drive our energy calls.”

Of all the commodities they reviewed, Goldman Sachs is most bullish on gold – and central bank demand is a big reason why.

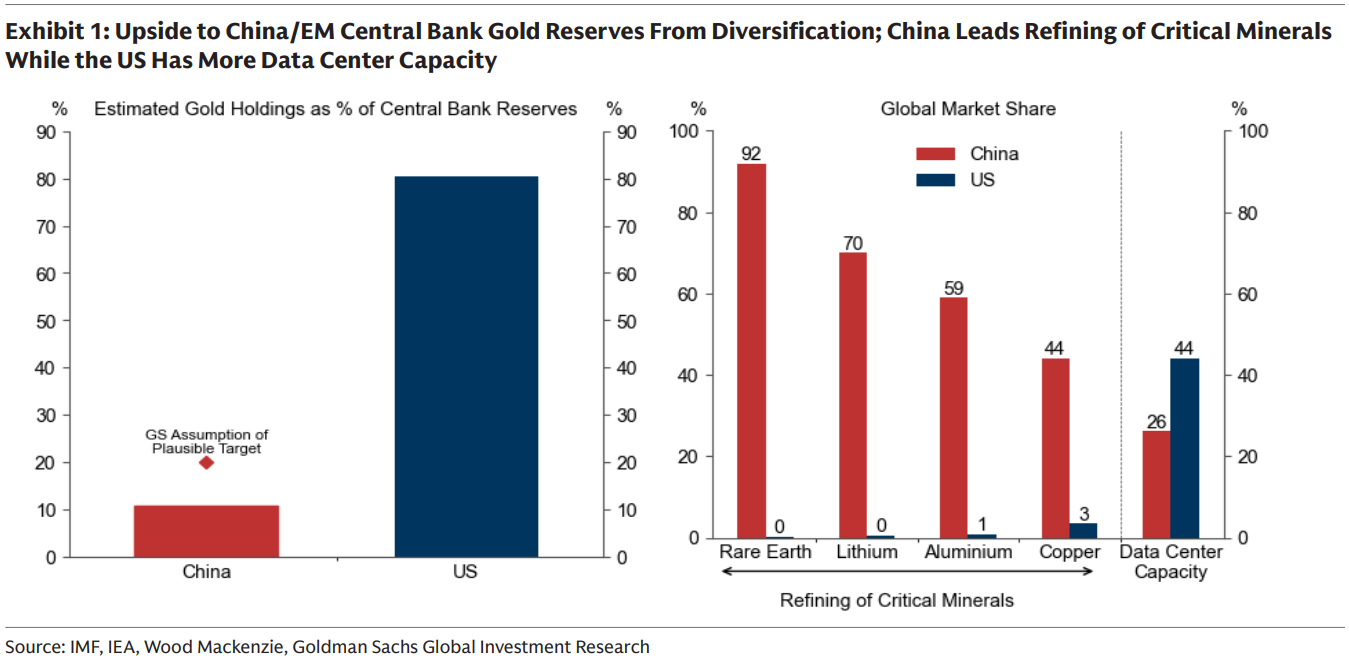

“We expect central bank gold buying to remain strong in 2026, averaging 70 tonnes per month (close to its 66 tonnes 12-month average, but 4 times above the 17 tonnes pre-2022 monthly average), and contribute about 14pp to our predicted price increase by Dec26 for three reasons,” they said. “First, the freezing of Russia’s reserves in 2022 was a sea change in how EM reserve managers perceive geopolitical risks. Second, the estimated gold reserve share of EM central banks such as the PBoC remains relatively low vs. global peers (Exhibit 1, left panel), especially given China’s ambition to internationalize the RMB. Third, surveys show record high central bank gold appetite.”

The analysts also see upside risk to their gold price forecast due to a further broadening of this diversification to private investors - a trend that has already resulted in competition for bullion between investors and central banks, and which has contributed to the multi-year bull market.

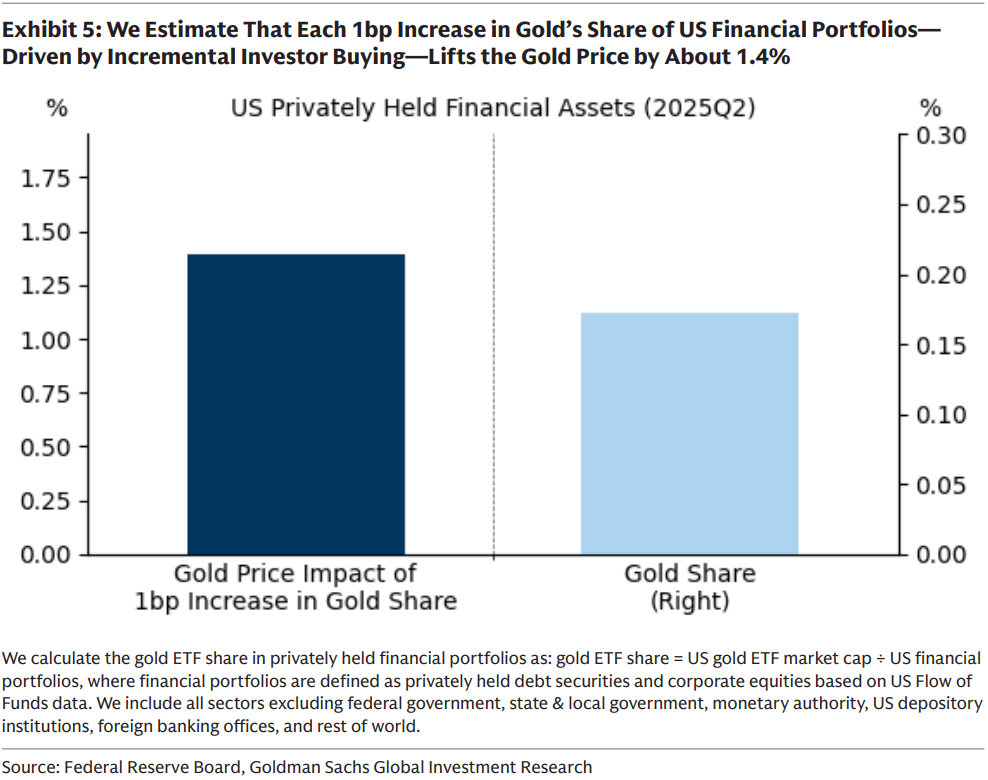

“Gold ETFs account for just 0.17% of US private financial portfolios, 6 basis points below its 2012 peak,” they noted. “We estimate that every 1bp increase in the gold share of US financial portfolios—driven by incremental investor purchases rather than price appreciation—raises the gold price by 1.4%.”

Goldman Sachs also emphasized the insurance value that commodities provide for investor portfolios in the current geopolitical environment.

“Even as gold remains our single favorite long commodity, we see a strong role for broader commodity length in strategic portfolio allocations,” they wrote. “The very high geographic concentration of commodity supply and the increasing geopolitical, trade, and AI competition has led to a more frequent use of commodity dominance as leverage. This raises the risk of supply disruptions, which underscores the insurance value of commodities.”

“Equity-bond portfolios are not well-diversified when commodity supply losses drive both weaker growth and higher inflation as well as strong commodity returns,” the analysts warned.

KitcoNews