JP Morgan says there’s a case against the gold rally continuing – and it’s wrong

NEW YORK (February 17) There’s a reasonable case to be made against gold’s continued appreciation, but that case is still incorrect, according to the senior brain trust at J.P. Morgan.

“Gold has had a ferocious rally over the last five years, skyrocketing over 170%, wrote Kriti Gupta, Executive Director of J.P. Morgan Private Bank, and Justin Biemann, Global Investment Strategist. “There’s a laundry list of reasons why, but the biggest driver may be a new era of geopolitical volatility and fragmentation incentivizing investors to buy the precious metal.”

“Now add on worries about currency debasement, growth, inflation and irresponsible fiscal finances that haven’t been fully reflected in sovereign assets,” they continued. “It’s no wonder the precious metal has been a popular asset for investors during times of stress.”

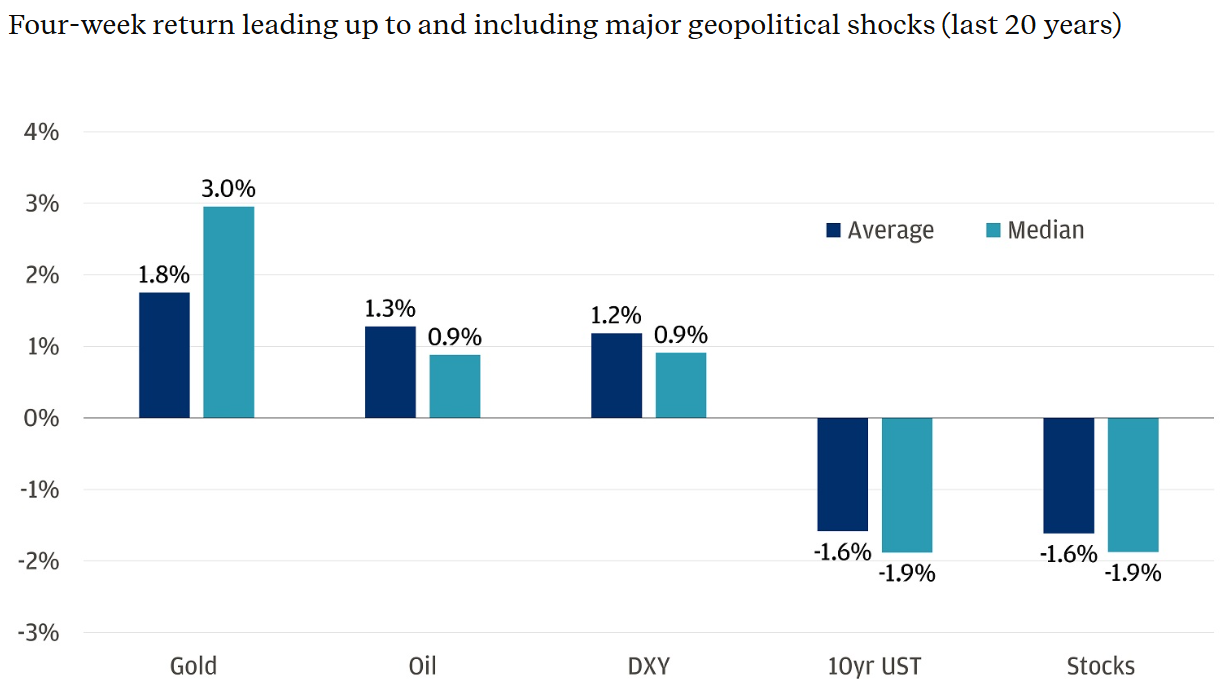

“Gold has averaged a return of 1.8% and a median of 3.0% during major geopolitical shocks, outperforming other asset classes.”

So if gold performs well in times of geopolitical turmoil, and that turmoil isn’t about to resolve itself, this begs the question: What stops gold’s rally?

Gupta and Biemann outline two major areas of risk. First, the possibility that central banks halt the recent years’ buying binge.

“The biggest driver of gold prices has been central banks,” they write. “Net purchases of gold have doubled since Russia’s war on Ukraine began in 2022. Central banks have fueled demand for the precious metal in efforts to diversify reserves away from the U.S. dollar after the United States froze Russian assets.”

The authors point out that outside of the IMF, the top five largest holders of gold are the United States, Germany, Italy, France and Russia. “What if that structural demand from global central banks waned?” they asked. “Or worse, what if they wanted to outright sell the commodity?”

They note that this has actually happened before. “From 1999 to 2002, the United Kingdom carried out a series of public auctions to sell over 50% of its gold holdings and diversify its reserves into foreign currencies,” they said. “During the same time, Switzerland voted to delink the Swiss franc from gold. Gold prices fell 13% in the three months following the United Kingdom’s announcement—a move equivalent to a ~$650 drop in today’s terms. The selling only stopped after several central banks signed The Washington Agreement on Gold to coordinate and cap large, price-moving gold sales. The agreement lapsed in 2019, as central banks largely became buyers of gold, not sellers.”

“In theory, that means sales are still possible. As is plateauing demand,” they wrote. “Rest assured, it’s unlikely to happen. At least, not anytime soon.”

Gupta and Biemann then explain why this is the case.

“As of 2025, gold has made up ~19% of emerging market reserves, relative to ~47% of developed market reserves,” they write. “Among the emerging markets piling into the precious metal, China stands out. Both an emerging market and a competitor to the United States, the country has actively been rotating its reserve assets into gold. Even though China is the seventh-largest custodian of gold holdings in the world, the metal only makes up 8.6% of its reserves according to the World Gold Council. If the trend continues, China has a lot more gold reserve purchases in the pipeline. And it’s not alone: Poland, India and Brazil have also been driving the structural demand.”

As far as G-10 central banks are concerned, the authors say there’s been no indication whatsoever that gold sales are being considered. “Even for the Federal Reserve, it would first require large legislative changes and a major break with over a century of precedent,” they write. “Furthermore, in 2025, 95% of central banks expected global gold holdings to increase, with 5% saying unchanged, and none of the respondents expecting a decrease, according to a YouGov/World Gold Council poll.”

The second major risk to gold’s continued price rally is the possibility that retail investors turn their backs on the yellow metal.

“Don’t forget retail investors,” Gupta and Biemann warn. “They’ve also been flocking to gold. These new buyers are often building a position as a hedge against rising geopolitical risks and macro uncertainty.”

But while this pattern has definitely contributed to gold’s price appreciation, there’s another side to the story. “New investors could drop the metal as quickly as they picked it up if risks die down or another hedge emerges,” they said. “The volatility at the end of January paints a clear picture. Gold shot up 20% in a week before crashing by the same margin in two days. Some investors would point to the episode as an example of short-term investors driving prices.”

To examine this argument, the authors place the current retail involvement into its broader context. “Retail activity is high, but not outrageous compared to history,” they note. “ETF holdings of gold (a good proxy for retail interest) stand at ~100 million ounces, the equivalent of only ~8% of global central bank holdings. It’s still below the record ~110 million ounces recorded in 2020, and while it could increase, retail activity isn’t in a position to set prices over the long term.”

And there are other good reasons for retail investors to hold onto their gold – or buy more.

“In addition to hedging against short-term geopolitical risks, gold is a long-term diversifier,” Gupta and Biemann point out. “It’s an asset that can protect against inflation, outperform during drawdowns and reduce overall portfolio volatility, given its relatively low correlation to other assets.”

In December, J.P. Morgan Global Research said that new demand from Chinese insurance giants and the crypto community will push gold prices higher in 2026.

“While this rally in gold has not, and will not, be linear, we believe the trends driving this rebasing higher in gold prices are not exhausted,” said Natasha Kaneva, head of Global Commodities Strategy at J.P. Morgan. “The long-term trend of official reserve and investor diversification into gold has further to run.”

The weaker dollar, lower U.S. interest rates, and economic and geopolitical uncertainty are traditionally positive drivers for gold prices, and all have played a role in the ongoing rally, and the investment bank noted that the metal has served both as a debasement hedge and as a non-yielding competitor to U.S. Treasuries and money market funds.

J.P. Morgan Global Research’s price forecasts are based on strong ongoing investor demand, along with continued central bank demand, which they project to average 585 tonnes per quarter in 2026.

KitcoNews