5 Things Every Investor Should Know Right Now

Say what you will about last week, it certainly wasn’t dull. The Federal Reserve, seemingly capitulating to President Donald Trump and Wall Street, became just the latest central bank to cut interest rates. Meanwhile, the president escalated the trade war even further, announcing that additional tariffs would be imposed on goods coming into the U.S. from China after another round of trade talks failed to deliver a satisfactory resolution.

Oh, and gold closed out July with a fourth straight month of gains.

Read on for five things I believe every investor should know right now.

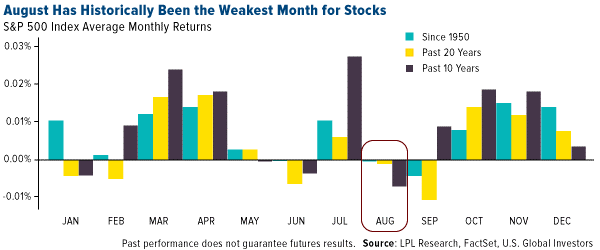

- August has a rocky history. Time to get defensive?

It’s been a good year for stocks so far, with the S&P 500 up about 19 percent as of the end of July. But here at the start of August, it may be time for investors to get cautious, if history is any indication. Since 1950, August has been the worst performing month, giving back 0.05 percent on average, according to LPL Research. It’s also been the weakest month in the past 10-year and 20-year periods.

August wasn’t always such a bummer. Between 1901 and 1951, the U.S. harvesting season made it the best month for stocks. But now that only 2 percent of Americans work in agriculture, August has sunk to the very bottom.

More recently, incidental geopolitical and economic concerns have roiled markets in the eighth month. Think Iraq’s invasion of Kuwait in 1990. Or the Asian contagion in 1997. Or the U.S. debt downgrade in 2011.

The way things are shaping up, we could be in for another rocky August…

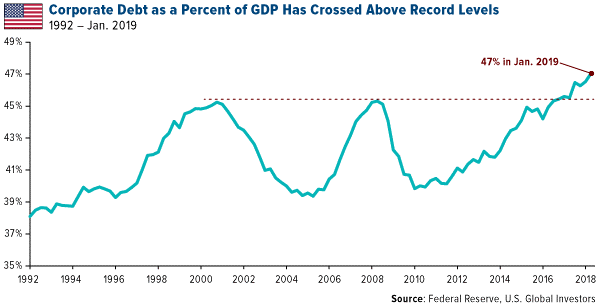

- The Fed capitulates, making the corporate debt bubble even more precarious.

I’ve already shared some of my thoughts with you on last week’s rate cut by the Fed. Lower (and potentially negative!) real and nominal yields here in the U.S. should spur investor demand for more reliable stores of value, such as gold, which I’ll talk about in a moment.

Another consequence of rock-bottom rates—as we’ve seen over the past decade since the end of the financial crisis—is greater debt loads. Corporate debt is already at a historic high as a percent of U.S. GDP, and it’s feared that the Fed’s move, coupled with the expectation of further cuts, could encourage even more risky borrowing. At the end of 2018, corporate debt stood at a whopping $5.7 trillion, two and a half times greater than the $2.2 trillion companies owed a decade earlier.

Even more concerning is the fact that the largest and fastest growing segment of investment-grade debt is rated BBB—which is just above junk status. In May, S&P Global reported that the value of U.S. BBB-rated bonds exceeded $3 trillion for the first time ever, accounting for more than half of the entire investment-grade bond universe.

In the event of an economic downturn, highly leveraged companies could risk seeing their debt downgraded to less than investment-grade, making interest payments more expensive. Lenders that have participated in risky loans could therefore be particularly vulnerable.

And while I’m on the topic of debt, the U.S. Treasury announced last week that its issuance of long-term debt would hold steady at a record $84 billion for the third consecutive quarter. This tops the previous record Treasury issuance, set in 2009, when the country was recovering from the worst economic pullback since the Great Depression. Borrowing by the U.S. government is now on track to exceed $1 trillion for the second straight year. It’s estimated that, by 2024, all U.S. government debt issuance will be used only to pay interest on past debt.

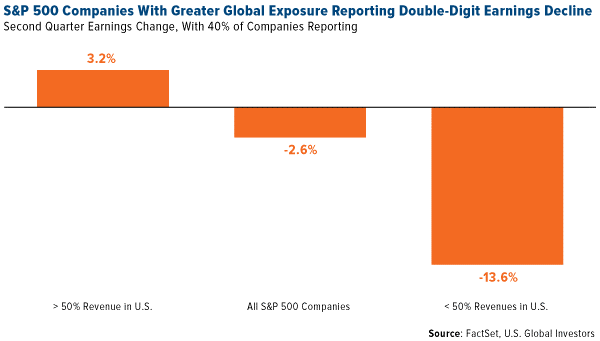

- Trump’s trade war is taking a huge toll on corporate earnings.

Last Thursday, President Trump announced via Twitter that the U.S. would impose a 10 percent tariff on $300 billion of imports from China, effective September 1. This is on top of the 25 percent tariff that’s already in place on $250 billion worth of Chinese-made goods—meaning nearly everything the U.S. buys from its once-top trading partner will now be taxed (and paid for by American importers and consumers, I should add).

I say “once-top” because, as the Wall Street Journal reported Friday, China lost its spot as America’s number one trading partner thanks to tensions between the two countries. In the first six months of 2019, imports from China fell 12 percent compared to the same period a year earlier, while exports fell 18 percent. The total value of bilateral trade, at nearly $290 billion, dropped below that of both Canada and Mexico for the first time in more than a decade.

As you might imagine, this is having a noticeably negative impact on earnings of U.S.-based, multinational companies. According to FactSet, firms that generate more than half of their revenues overseas have seen their bottom line plunge as much as 13.6 percent quarter-over-quarter. That’s compared to a 3.2 percent increase in earnings for companies with less global revenue exposure, and an average 2.6 percent decline for all S&P 500 companies that have reported so far.

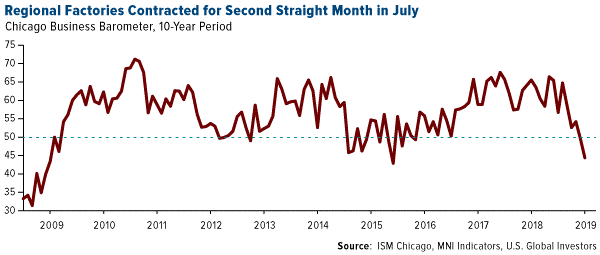

- Tariffs are also hurting manufacturing growth, both here and abroad.

U.S. factories are having their worst start to the third quarter since the end of the financial crisis. The purchasing managers’ index (PMI) posted a 50.4 in July, its lowest reading since September 2009 despite being slightly higher than earlier forecasts. Employment contracted for only the second time in about 10 years, suggesting “the goods-producing sector is on course to act as a significant drag on the economy in the third quarter,” writes Chris Williamson, chief business economist at IHS Market.

The Chicago Business Barometer, often seen as a bellwether of the U.S. economy, fell further below the neutral 50.0 level in July. The indicator touched 44.4, down from 49.7 the previous month, with production falling 22 percent to hit a 10-year low. Some factories are holding tariffs directly responsible for the slowdown, according to the monthly report.

The downturn isn’t confined to the U.S., of course. The Global Manufacturing PMI continued to contract for the third consecutive month in July, falling to 49.3, its lowest reading since October 2012.

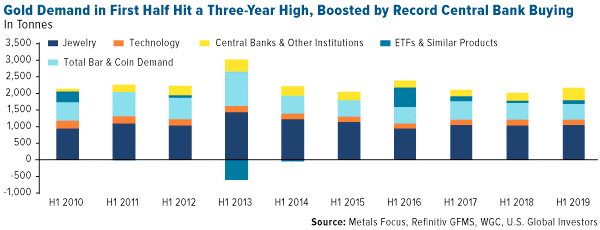

- Gold demand just had its best first half of the year in three years.

Given the considerable risks right now, is it any wonder that gold has performed so well this year? As I write this, the yellow metal is trading above $1,475, up 12.6 percent from the start of January.

Gold demand in the first half of 2019 was its best in three years, climbing to 2,181.7 tonnes, largely due to increased appetite for gold-backed ETFs as well as record buying by central banks. Bank purchases of bullion rose an incredible 47 percent year-over-year in the second quarter, pushing the total amount for the January-to-June period to its highest since central banks became net buyers of gold in 2010. Poland was the top buyer—ahead of Russia, even—with reserves growing 77 percent to 100 tonnes.

Meanwhile, investors added some 67.2 tonnes to their holdings of gold-backed ETFs in the second quarter. This took total holdings to a six-year high of 2,548 tonnes. Among the factors driving demand were geopolitical uncertainty, global negative yields and a rising gold price.

Treasury yields are falling. Could they drop below zero? Stay up to date by subscribing to our FREE, award-winning Investor Alert! Click here!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The Chicago Business Barometer is a weighted composite indicator made up of five sub-indicators, namely New Orders, Production, Employment, Order Backlogs and Supplier Deliveries. It is designed to predict future changes in gross domestic product (GDP).

A bond’s credit quality is determined by private independent rating agencies such as Standard & Poor’s, Moody’s and Fitch. Credit quality designations range from high (AAA to AA) to medium (A to BBB) to low (BB, B, CCC, CC to C).

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC. This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

*********

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].