About That “Inflation Trade”…

An “inflation trade” is possible, but take heed of its shelf life.

With the tariff/trade war drums fading lately, the logical conclusion is “inflation trade upcoming!” and cyclical markets – including, or even especially commodity-related stocks – gaining a bull phase as trade bottlenecks open back up.

The Trigger

Indeed, we have recently been increasingly open to this prospect in NFTRH, since noting a few weeks ago that the Silver/Gold ratio could snap back hard from whatever firm low it makes on the current plunge. A precedent is the 2020 plunge and reversal. The questions now are has the ratio declined to an extreme yet, and is it likely to put on a hard reversal?

I think the answer to both questions is likely yes.

However, I do not subscribe to silver bulls’ insistence that silver has to revert to some imagined upside level simply because it is so depressed in relation to gold. But there is a technical tendency for silver to haul ass nominally and in terms of gold after such relative declines. Silver’s market is not an easy-going market.

A rising Silver/Gold ratio would be the clearest trigger of an oncoming inflation trade. Silver is more inflation-sensitive than gold, has more positive cyclical/industrial utility and has an army of speculators in waiting to drive it higher. Gold is just a heavy barometer of a negative macro with more monetary qualities.

Another important question to consider is whether any coming “inflation trade” will be a grand event such as eternally projected by Team Commodity Super Cycle. Tap the breaks on that, Sparky. It is best to take rotating market phases in chunks, and keep them subject to ongoing analytical updates.

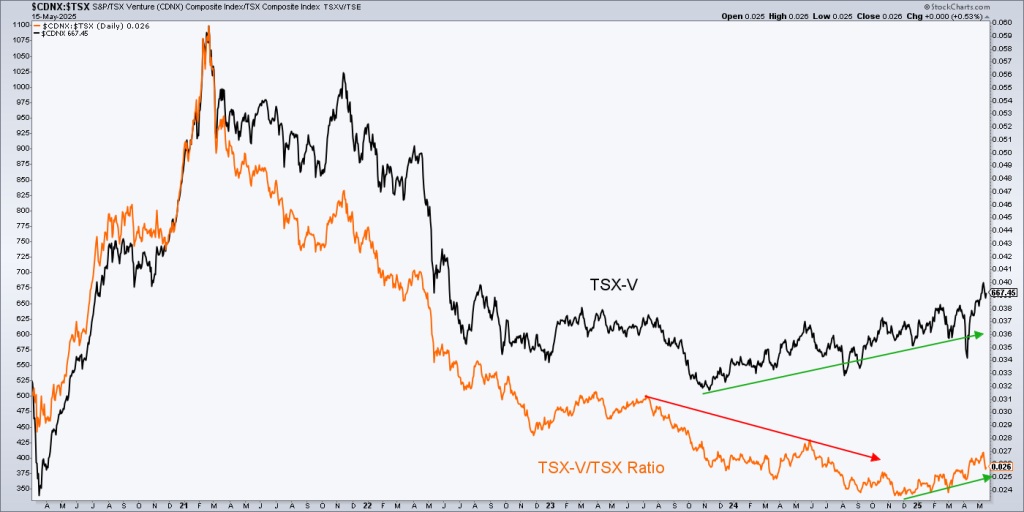

While the macro table appears set for an “inflation trade” (mini or maxi), it is not here yet. Let’s look at the current status of some indications, beginning with the Canadian TSX-V, an index filled with super speculative commodity/resources related stocks.

Da ‘V’ has been grinding higher since late 2023. However, its ratio to the senior TSX index did not bottom until late 2024. In past work we have illustrated how a rising TSX-V/TSX ratio tends to coincide with inflationary phases. The most that can be said of the current situation is that it is indicative of a potential inflation trade in 2025. The larger trend remains down at this time, however.

Commodity indexes/ETFs are going sideways, not yet picking up the baton that TSX-V is trying to hand off to them.

Certain specialty and geopolitically sensitive commodities will go their own way and have been going their own way. But the bulk of the commodity complex is thus far a non-starter.

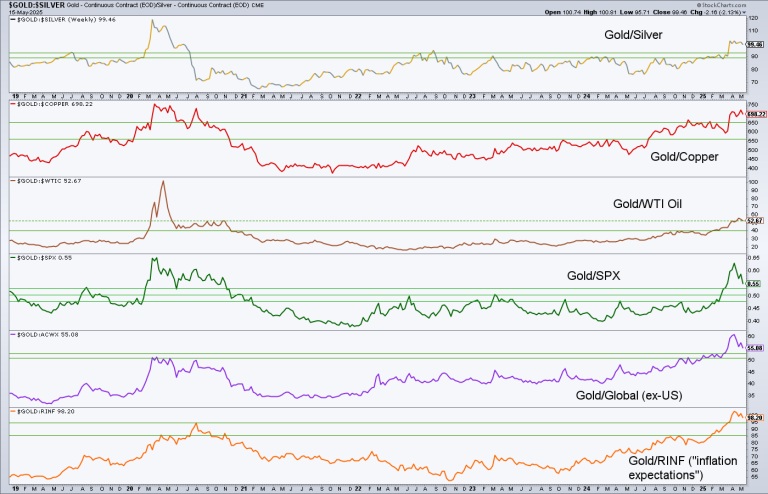

I would be careful about becoming mesmerized by a silver and commodity super cycle Sirens’ song longer-term, however. This weekly chart shows that gold is squarely bullish in relation to silver, commodities, stocks and yes, “inflation expectations”. These ratios are merely in varying states of consolidation/correction.

When gold rises vs. cyclical and inflation sensitive asset markets, the indication is counter-cyclical. Commodities are cyclical assets, no matter how badly lazy analysis wants to lump them in with gold as part of the same basket of “resources”.

Bottom Line

An “inflation trade” featuring a broader group of commodities is possible, even probable. The trigger would be the Silver/Gold ratio bottoming and turning up.

However, the macro has ground out a larger counter-cyclical trend, which would be anti-commodity, anti-stock market and relatively, pro-gold. That is the trend of the last 2 years. At this point, Team Counter-Cycle is merely in correction. Within this various “inflation trades” could gain a bid for a very tradable rally potentially lasting a year or more (the 2007-2008 specimen lasted 1.5 years).

We’ll let this excerpt from NFTRH 862 wrap up the article’s bottom line. The “big and relentless leg up” was the 2020-2021 surge. If past is prologue, any coming new surge could be two things: 1) quite tradable and 2) terminal prior to a broader market liquidation and an obviously counter-cyclical macro.

As to the chart, let’s think about the inflation trades that followed gold in 2001. A big and relentless leg up was followed by a correction before the big spike blowoff as its final act, into Armageddon ’08. If something similar were to happen this time, we might see today’s correction resolve with an upside acceleration into and eventual important high, and whatever coming broad market crash is out in the future. But that rally would be tradable.

For “best of breed” top-down macro analysis and market strategy covering Precious Metals, Commodities, Stocks and much more, subscribe to NFTRH Premium, which includes a comprehensive weekly market report, detailed NFTRH+ updates and chart/trade setup ideas, and Daily Market Notes. Receive actionable (free) public content at NFTRH.com and subscribe to our free Substack. Follow via X @NFTRHgt and BlueSky @nftrh.bsky.social, and subscribe to our YouTube Video Channel.

********