Big US Stocks’ Q2’21 Fundamentals

The US stock markets continue to power ever higher to an endless series of new records. Leading the way are the big US stocks, with extraordinary gains fueled by the Fed’s radically-unprecedented money printing. The winding-down Q2’21 earnings season illuminates how these massive companies are faring fundamentally. While their results were spectacular, their valuations are forging deeper into risky bubble territory.

The flagship US S&P 500 stock index (SPX) enjoyed a very-strong second quarter, surging 8.2% to hit a new record close of 4,298. Fully 18 of those 63 trading days ended at all-time highs, driving the extreme complacency permeating these lofty stock markets. Contributing strongly to these outsized gains was the Fed’s ongoing balance-sheet growth. That ballooned another 5.1% in Q2 proper, annualizing to a 20.3% pace!

Over this past year ending June 30th, the SPX soared 38.6% higher! Remember there was a stock panic in March 2020 on fears governments’ pandemic lockdowns would crush the US economy. With the SPX cratering 33.9% in just over a month, Fed officials panicked and slammed the monetary accelerator to the floor. They haven’t let up since, with $120b of monthly quantitative-easing bond monetizations still underway.

The Fed’s balance sheet has mushroomed an astounding 90.7% or $3,910b over the last 16.6 months since that stock panic! The US central bank has nearly doubled the supply of US dollars during that short span! This wildly-unprecedented hyper-inflationary monetary backdrop must be considered in all stock-market analysis. Stocks should be strong with redlined money pumps spewing vast torrents of new dollars.

That monetary deluge didn’t just buoy stock prices, but fueled anomalously-huge growth in revenues and earnings. The Fed has directly monetized $2,741b of US Treasuries in this same post-panic timeframe, its Treasury holdings skyrocketing 108.6%! The US Treasury spent that newly-conjured money on epic stimulus payments, transfer payments, and salaries. That artificially boosted demand for corporations’ products.

While many Americans struggled through the pandemic lockdowns, many didn’t. An average family of four with an adjusted gross income under $150k received about $11,400 of federal stimulus payments over this past year or so! There were other payments too, like extended unemployment benefits. That torrent of trillions of dollars of extra money was partially spent on goods and services offered by big US companies.

The colossal excess demand generated by all that Fed-supplied Treasury-spent money printing is the main reason supply chains are so overwhelmed. We all have friends who have bought big-ticket toys like cars, recreational vehicles, and boats that wouldn’t have made such purchases otherwise without the big stimulus payments. So realize demand and thus corporate sales and profits are skewed anomalously high.

While the Democrats running the US government really want to send more cash handouts to Americans heading into November 2022’s midterm elections, that is going to be challenging. Congress has to pass laws to authorize such payments, and the Democrats only have razor-thin margins of 50-50 in the Senate and 220-212 in the House. So odds are the coming year’s stimulus will be far smaller than this past year’s.

The emergency pandemic unemployment benefits greatly boosted effective take-home pay for millions of workers too. While minimum wages vary by state, the national average is probably somewhere around $10 per hour. That’s the equivalent of $20k per year. But the expanded federal and state unemployment benefits pushed laid-off service workers’ pay up to around a $35k annualized rate! That’s a lot of extra money.

They naturally spent some of that windfall on goods and services from big US companies. How much excess iPhone demand did Apple enjoy because Americans were flush with free money? How much more stuff was ordered from Amazon? How many extra cars and graphics cards did Tesla and NVIDIA sell over this past year thanks to the trillions of dollars of pandemic stimulus? The answer is certainly a ton!

So as we analyze the epic results the big US stocks reported in Q2’21, realize this is probably the high-water mark that was massively artificially elevated by that epic flood of new money. The Fed’s largesse has unleashed the dangerous side effect of serious universal price inflation. That will erode demand for corporate products and margins for selling them, leaving the big US stocks’ results looking worse going forward.

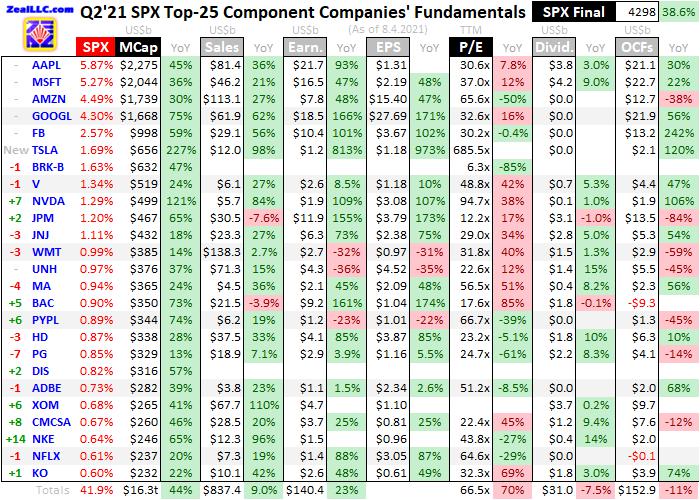

US securities laws require companies to report their latest results within 40 days after quarter-ends. By the middle of this week, 35 of those had passed so the Q2’21 results are mostly in. Every quarter I wade through the latest official 10-Q quarterly reports from the 25 largest SPX companies. Some combination of these popular behemoths dominates nearly all portfolios, including Americans’ prized retirement accounts.

These 25 mega-companies commanded a staggering 41.9% of the entire market capitalization of all 500 SPX stocks at the end of June! The top 25 are bigger than the bottom 441! And the colossal exchange-traded funds tracking the SPX are the largest in the world. The SPY SPDR S&P 500 ETF, IVV iShares Core S&P 500 ETF, and VOO Vanguard S&P 500 ETF had $383b, $295b, and $244b of net assets this week!

This table outlines key fundamentals of these 25 largest companies in the US stock markets. Their stock symbols are preceded by how their rankings within the SPX shifted in the year since the end of Q2’20. After their symbols these companies’ actual percentage weightings within the S&P 500 at the end of Q2’21 are shown, along with their market capitalizations in billions back when that reporting quarter was ending.

Their market caps, as well as their other fundamental data, are followed by year-over-year changes from the ends of Q2’20 to Q2’21. Looking at market-cap changes offers a purer read on companies’ values than stock-price changes, normalizing out some manipulative effects of corporate stock buybacks. Those are done to artificially boost share prices and earnings per share, maximizing executives’ compensation.

Quarterly revenues, GAAP corporate profits, earnings per share, trailing-twelve-month price-to-earnings ratios as of quarter-end, dividends paid, and operating cash flows generated are shown. These key data are also followed by YoY changes. Blank fields usually mean a company hadn’t reported that particular data as of mid-week. Berkshire Hathaway and Disney are keeping their shareholders waiting like usual.

Percentage changes are excluded if they are misleading or not meaningful, primarily when data shifted from positive to negative or vice versa. Unfortunately some companies run goofy fiscal quarters offset from calendar ones. NVIDIA, Walmart, and Home Depot report on quarters ending one month later than normal, while Adobe and NIKE run one month earlier. So these deviants’ latest-reported quarters are included.

The elite big US stocks dominating the S&P 500 reported spectacular performances last quarter! But they sure as heck should have with the Fed nearly doubling the US-dollar supply, and most Americans showered with helicopter-money direct payments from the US Treasury. Those stimmies were quickly spent, unleashing huge demand for the goods and services many of these massive companies produce.

The big US stocks’ total market capitalization soared 44.4% over this past year to $16.3t! That’s naturally a new all-time-record high. But interestingly the concentration risk of too-much capital pouring into too-few stocks moderated slightly. These 25 largest US stocks again constituted 41.9% of the entire S&P 500, which was actually down from Q3’20’s 43.0% peak. The Fed’s inflationary tide is lifting more boats.

One of the main themes in big-US-stock quarterly analysis for many years now has been the increasing bifurcation between the gargantuan mega-cap technology companies and the rest of the SPX. These are very familiar to everyone, with products universally used and stocks universally owned. They are Apple, Microsoft, Amazon, Alphabet, and Facebook. Their average market cap exiting Q2 was an epic $1,745b!

While the next-20-biggest US companies are almost as famous, their market caps averaged a far-smaller $376b. The Big Five tech giants alone accounted for 22.5% of the entire SPX, while the next 20 under them were responsible for just 19.4%. Those mega-cap techs’ quarterly results have been so extreme in this past pandemic year they are heavily distorting the rest of the SPX companies’. So we have to look at both.

While the big US stocks’ Q2’21 results were fantastic, they came from a massively-suppressed base in the comparable year-earlier Q2’20. Remember that was emerging from the stock panic at the height of governments’ lockdown orders. That was certainly peak-fear too, when Americans didn’t yet understand how COVID-19 spread, how lethal it was, and who faced the biggest risks of serious or devastating outcomes.

With tens of millions of Americans sheltering in place at home then, demand for the goods and services provided by many of these companies was relatively-light. That low base amplifies the year-over-year growth numbers reported. So big US stocks’ spectacular Q2’21 results are inarguably a one-off extreme outlying pandemic anomaly. There’s no way they can sustain such blistering growth rates going forward.

All the following comparisons exclude Berkshire Hathaway and Disney from Q2’20 totals since they have not reported their Q2’21 results yet. The SPX top 25’s total revenues soared 19.7% YoY to $837.4b! That magnitude of top-line growth in such huge companies is unheard of, off the charts. And the great majority of it came from the Big Five mega-cap techs, which saw their sales skyrocket an epic 36.1% YoY to $331.6b!

It defies belief that these biggest companies in the world could grow their revenues so much. Not only is moving the needle very challenging given their colossal sizes, but the Big Five were also big beneficiaries of exploding stay-at-home demand during Q2’20’s pandemic lockdowns. Yet these mega-cap techs continue to dazzle and fire on all cylinders, far outperforming the rest of the SPX stocks fundamentally.

This can’t be sustainable though. With average Q2’21 sales of $66.3b, it is probably impossible to keep rapidly growing from such sky-high levels. And with much-smaller or no pandemic-stimulus payments going forward, product demand will be constrained. Odds are that extreme Fed-and-Treasury-funded buying cannibalized significant-to-sizable future demand. That will almost certainly retard sales going forward.

How long until all the people who bought new Apple iPhones and iPads over this past year will feel the need to upgrade? Electronic devices easily perform well for several years or so. Will Americans who just took advantage of the trillions of dollars of free money to buy new stuff on Amazon need to replace those items anytime soon? Probably not for the most part. Pulled-forward demand is ominous for companies’ outlooks.

The next-20-largest SPX stocks only saw their sales grow a comparatively-modest 10.9% YoY to $505.8b excluding Berkshire and Disney. And that number was heavily skewed by oil super-major ExxonMobil. With much of the world economy locked down in Q2’20, crude oil collapsed to an average price of $28.21. But in Q2’21 that blasted 134.5% higher to average $66.16, driving Exxon’s extreme 109.9% sales growth to $67.7b.

All the other huge sales growth among these big US stocks below the mega-cap techs came from much-smaller bases. For example NVIDIA’s soared 83.8% YoY to just $5.7b, as cryptocurrency miners and gamers rushed to snatch up the latest-generation computer graphics cards. Soaring revenues are radically easier to accomplish off smaller bases than larger ones. And they’ll be way less common without stimmies.

As you’d expect with soaring top lines, the bottom-line earnings growth leveraging those sales was much better. The SPX top 25 without Berkshire and Disney saw their hard profits under Generally Accepted Accounting Principles soar 51.9% YoY to $140.4b! That is again astounding coming from enterprises that operate at these colossal scales. Of course Q2’20’s lockdown-suppressed base effect played a big role.

Not surprisingly the lion’s share of this epic earnings growth came from the mega-cap techs, with Big Five earnings skyrocketed a mind-blowing 88.0% YoY to $74.9b! The combination of those trillions of dollars of government handouts and these companies having products consumers and businesses really want to buy fueled astonishing profits. It is mathematically impossible for anything near these growth rates to last.

The next-20-largest US stocks except that pair of feet-dragging shareholder-disrespecting late reporters saw their earnings surge a still-amazing-but-way-less-crazy 24.5% YoY to $65.5b. Being in the financial-newsletter business, I have CNBC and Bloomberg on in my office all day everyday. Many if not most of the Wall Street analysts I saw interviewed attributed this incredible Q2’21 to a strong economic recovery.

But a big fraction of the excess demand generated by the Fed’s money printing and Treasury’s spending is artificial. It either wouldn’t have existed without all that free money or it pulled forward demand from future quarters and years. Again the vast amounts of new goods Americans purchased in this past year won’t need to be upgraded or replaced anytime soon. These extravagantly-fat profits aren’t sustainable.

The raging inflation this profligate Fed has unleashed is another big reason earnings will have to shrink. The prices of most goods and services are surging because of that near doubling in the US-dollar supply since the stock panic. When monetary growth rates far exceed those of the economic output on which to spend money, rising prices are the inevitable result. Relatively more dollars compete for and bid up prices.

Defensive Fed officials keep blaming supply-chain disruptions while insisting this inflation is “transitory”. That’s a red herring to misdirect. Legendary American economist Milton Friedman warned “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” And inflation crushes corporate profitability.

American companies including these largest ones are increasingly seeing surging input costs. They only have two choices on how to handle them, pass them along to customers through higher selling prices or eat them. The latter obviously cuts into profits, but so does the former since price hikes lower demand. Customers buy elsewhere, abstain, or substitute other things as prices get too high for them to stomach or afford.

Bank of America’s research team is doing fantastic work on inflation. One thing it has done is track the mentions of the word “inflation” in SPX companies’ earnings calls since 2003. Those have skyrocketed up about 1100% YoY to a record high! Many dozens if not hundreds of SPX companies warned in Q2’21 that their profits are going to be under pressure going forward due to the higher input costs they are bearing.

So these incredible earnings the big US stocks just reported last quarter are what is truly transitory. They can’t and won’t last. And that’s a seriously-threatening problem with prevailing valuations already deep into bubble territory. Over the last century-and-a-half or so, fair value for the US stock markets averaged 14x trailing-twelve-month earnings. Twice that at 28x is the threshold where dangerous bubble valuations start.

Exiting Q2’21 before these latest results were reported, the SPX top 25 averaged scary TTM P/Es way up at 66.5x! And even at the end of July with most of this last quarter’s profits windfall incorporated into the rolling-four-quarter average, the big US stocks’ P/Es merely retreated to 50.6x earnings. Though both of these were dragged higher by Tesla’s insanely-rich valuation, the big US stocks are still crazy-expensive.

Tesla attracts investors who couldn’t care less about sales and profits, they are true believers that this car maker will electrify and forever change the world. So Tesla exited Q2’21 with an absurd 685.5x P/E, but its epic 813.2% YoY earnings growth from a tiny base slashed that P/E to 364.8x leaving July. Excluding that story stock, the rest of the SPX-top-25 stocks averaged 38.4x and 36.3x at the ends of June and July.

The Big Five mega-cap techs weren’t cheap averaging 39.2x and 38.4x, and the rest of the 20 largest US stocks without Tesla weren’t either at 38.1x and 35.7x. All these valuations are deep into bubble territory, dangerously-expensive levels from which secular bear markets spawn! And all those include the massive corporate earnings generated by those trillions of dollars of money printing and government stimulus payments.

As corporate earnings inexorably decline in coming quarters from excessive demand normalizing and serious price inflation, the shrinking E in the P/E ratio is going to force valuations even higher. That will make the big US stocks look even more overvalued, eventually resulting in the major bear necessary to fundamentally recouple stock prices with underlying profits. These Fed-levitated valuations are seriously scary.

The Fed will fight slowing its money printing every step of the way, as it ignoring all the recent red-hot US headline inflation reports has again proven. The latest CPI and PPI reads printed way up at 5.4% YoY and 7.3% YoY, even though the government heavily lowballs them to mask true inflation! But eventually the price increases from nearly doubling the US-dollar supply will be so extreme the Fed will be forced to act.

That day of reckoning will hit these artificially-inflated stock markets like a wrecking ball. Bear markets emerging from extreme overvaluations are brutal. The last two mauled the SPX down 49.1% over 2.6 years ending in October 2002 and 56.8% over 1.4 years ending in March 2009! The next 50%ish drop in big-US-stock prices is way overdue. Not even this money-spewing Fed can hold off market forces forever.

Rounding out the elite US companies’ Q2’21 results were dividends and operating cash flows generated. Interestingly the SPX top 25’s overall dividends actually fell 7.5% YoY to $31.0b. The mix of stocks in this group contributed, with larger dividend payers Cisco and Merck falling out while smaller ones like NIKE climbed in. The massive ongoing stock buybacks likely contributed too, as Wall Street prefers them over dividends.

While I haven’t tracked stock buybacks among these big US stocks so far, I’m tempted to start. In Q2’21 alone, Apple, Microsoft, Alphabet, and Facebook repurchased a staggering $50.0b of their stocks! No wonder their market caps surged so dramatically with all that buying. One problem is stock buybacks are dependent on earnings and operating-cash-flow levels. If they shrink, so will the capital available for buybacks.

And that operating-cash-flow-generation front was already disproportionally weak last quarter. The SPX top 25’s OCFs actually fell 4.4% YoY to $152.9b! That not only excludes Berkshire and Disney, but the enormous money-center banks JPMorgan Chase and Bank of America which have wildly-volatile cash flows in that business. Yet again that huge bifurcation between mega-cap techs and everything else is clear.

The Big Five techs saw their OCFs soar 24.8% YoY to $91.7b last quarter. But the next-20-largest US companies except for those just-mentioned four saw their OCFs collapse 29.3% YoY to $61.2b! While the big-US-stock mix again contributed as companies entered and left the elite top-25 ranks, operating-cash-flow generation was still way weaker than it should’ve been given that astounding extreme earnings growth.

So make no mistake, as good as these lofty stock markets look they are exceedingly-risky today. As the S&P 500 levitates to endless new record highs directly fueled by vast torrents of Fed money printing, the big US stocks’ valuations are already deep into dangerous bubble territory. That spawns secular bear markets, which tend to slash stock prices in half over a couple years or so. Stock prices eventually reflect profits.

The Fed is fighting this tooth and nail, but can’t stave off the overdue valuation normalization forever. At some point the exploding price inflation unleashed by the Fed’s near-doubling of the US money supply will force its hand on slowing, stopping, and maybe even reversing QE. In the meantime, the money-flood-fueled higher prices will increasingly erode corporate profitability. That will push valuations even higher.

What to do? Investors should start lightening their heavy stock allocations by adding 5% to 10% in gold, along with double or triple that in fundamentally-superior gold-mining stocks. They have colossal upside potential from both this tsunami of monetary inflation and these bubble-valued stock markets rolling over. Gold and gold stocks are the best inflation hedges, and outperform dramatically during secular stock bears.

At Zeal we walk the contrarian walk, buying low when few others are willing before later selling high when few others can. We overcome popular greed and fear by diligently studying market cycles. We trade on time-tested indicators derived from technical, sentimental, and fundamental research. That’s why all 1,223 stock trades recommended in our newsletters since 2001 averaged hefty +22.3% annualized realized gains!

To multiply your wealth trading high-potential gold stocks, you need to stay informed about what’s going on in this sector. Staying subscribed to our popular and affordable weekly and monthly newsletters is a great way. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today while this gold-stock upleg remains young! Our newly-reformatted newsletters have expanded individual-stock analysis.

The bottom line is despite reporting truly-spectacular Q2’21 results, the big US stocks’ valuations remain deep in dangerous bubble territory. They probably just saw peak revenues and earnings growth in this last quarter. The Fed’s extreme money printing nearly doubling the US money supply since the stock panic, and the trillions of dollars of government stimulus payments it financed, fueled unsustainable excess demand.

Americans flush with free cash spent it like drunken sailors, driving record sales and profits. But with the pandemic winding down, that gravy train is ending. That means lower demand for corporate goods and services going forward. That along with serious price inflation eroding profits will push valuations even higher. A bear-market reckoning to normalize valuations is looming, regardless of the Fed’s machinations.

Adam Hamilton, CPA

Copyright 2000 - 2021 Zeal LLC (www.ZealLLC.com)

*********

More from Gold-Eagle