Big US Stocks’ Q4’20 Fundamentals

The US stock markets have soared over the past year, achieving truly-astounding performance. Vast torrents of newly-created money deluged in, catapulting stock prices radically higher. But this epic flood of central-bank-conjured liquidity has left stock prices massively disconnected from companies’ underlying fundamentals. With each passing earnings season, this incongruity grows ever-more egregious and risky.

Exactly a year ago, the flagship US S&P 500 stock index (SPX) was plummeting in a rare stock panic. Traders were scared of the economic impacts from governments’ mounting lockdown orders to fight the emerging COVID-19 pandemic. Their frenzied selling snowballed, hammering the SPX a catastrophic 33.9% lower in less than five weeks! That included a formal stock panic, 20%+ losses in two weeks or less.

Central bankers freaked out, worrying the negative wealth effects from free-falling stocks would trigger a depression. So led by the Federal Reserve, they started creating and injecting trillions of dollars into their economies. Over just 3.0 months after the dark heart of that stock panic, the Fed rushed to print money so furiously that its balance sheet skyrocketed $2,857b or 66.3% higher! That extreme was wildly unprecedented.

As the Fed intended, a sizable fraction of those trillions of dollars found their way into the stock markets. So by year-end 2020, the SPX had blasted a stupendous 67.9% higher from its stock-panic nadir! For the whole year it rallied 16.3%, incredible performance considering the economic carnage from those lockdowns. Another few trillion dollars of emergency pandemic stimulus from the US government sure helped.

But do the fundamentals of the big US stocks dominating the S&P 500 justify these lofty liquidity-deluge-driven prices? The unthinkably-colossal money flows that blasted stocks vertical in 2020 are going to be dramatically smaller going forward. Last year the Fed ballooned its balance sheet a monstrous $3,198b or 76.8%! Now in 2021 this central bank is doing $120b per month of quantitative-easing bond monetizations.

If the Fed can sustain that despite the serious price inflation that epic influx of new money is spawning, it implies $1,440b of balance-sheet growth this year. According to the US Treasury, last year the federal government’s debt rocketed up $4,547b or 19.6%. Like the fed’s balance-sheet expansion, it is hard to imagine 2021’s deficit spending hitting half of last year’s crazy extremes even with Democrats in power.

So the big US stocks’ underlying fundamentals are more important than ever. These elite companies recently finished reporting their Q4’20 earnings season. Most of them run their accounting on calendar years, and the SEC gives US companies 60 days after year-ends to file fully-audited 10-K annual reports. After every quarter I wade through the latest operating and financial results from the 25 largest SPX stocks.

These behemoths effectively are the US stock markets, commanding a massive 42.5% of the entire S&P 500’s market capitalization! That exceeds the collective weighting of the 445 smallest SPX component stocks. Because of their huge size, some combination of the SPX-top-25 companies dominates almost all portfolios including retirement accounts. So investors need to stay aware of how the big US stocks are faring.

The leading SPX ETFs are wildly popular, led by the gargantuan SPY SPDR S&P 500 ETF, IVV iShares Core S&P 500 ETF, and VOO Vanguard S&P 500 ETF. A staggering $334.7b, $255.9b, and $196.4b of investors’ capital was deployed in these colossal investment vehicles this week! With the stock markets just drenched in euphoria and complacency, this is an exceedingly-important time to watch the fundamentals.

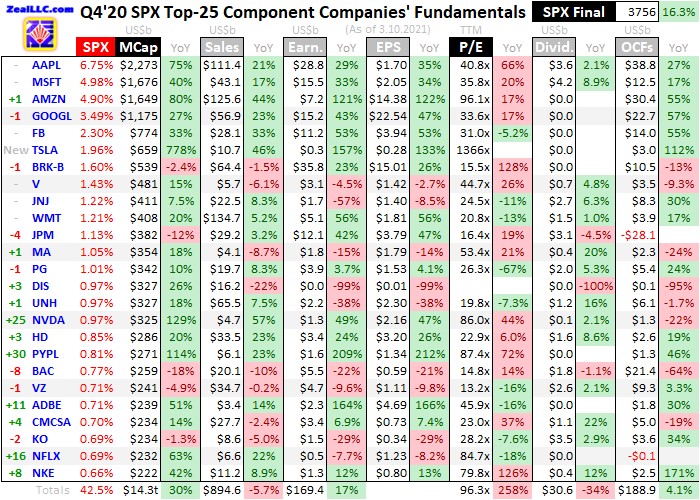

This table outlines key fundamentals of the 25 largest companies in the US stock markets. Their stock symbols are preceded by how their rankings within the SPX shifted in the year since the end of Q4’19. After the symbols these companies’ actual percentage weightings within the S&P 500 at the end of Q4’20 are shown, along with their market capitalizations in billions back when that reporting quarter was ending.

Their market caps, as well as their other fundamental data, are followed by year-over-year changes from the ends of Q4’19 to Q4’20. Looking at market-cap changes offers a purer read on companies’ values than stock-price changes, normalizing out some manipulative effects of corporate stock buybacks. They are done to artificially boost share prices and earnings per share, maximizing executives’ compensation.

Quarterly revenues, GAAP corporate profits, earnings per share, trailing-twelve-month price-to-earnings ratios as of quarter-end, dividends paid, and operating cash flows generated are shown. These key data are also followed by YoY changes. Blank fields usually mean a company hadn’t reported that particular data as of mid-week, but that didn’t happen this time with the SEC’s annual-reporting deadline now passed.

Unfortunately some companies run goofy fiscal quarters offset from calendar ones, making them harder to compare with their peers. This makes no sense with modern automated accounting systems. Adobe and Nike have fiscal quarters ending one month before calendar ones, while Walmart, NVIDIA, and Home Depot report on quarters ending one month after normal. So generally their latest-reported quarters are included.

Percentage changes are left blank if they are misleading or not meaningful, primarily when data shifted from positive to negative or vice versa between Q4’19 to Q4’20. In a quarter where the S&P 500 itself surged 16.3% YoY, its top 25 companies’ results remained incredibly bifurcated. The beloved mega-cap technology stocks continue to enjoy fantastic performances, which the other big US stocks greatly lagged.

Even among these largest US stocks, the Big Five technology behemoths utterly dominate weighing in at a stunning 22.4% of the entire S&P 500. Together Apple, Microsoft, Amazon, Alphabet, and Facebook had a $7.5t collective market capitalization as Q4 ended. That is bigger than the bottom 359 stocks of the SPX! And the incredible performances of these tech giants continue to reveal why they are so popular.

The four largest each had market caps exceeding $1t exiting last quarter, the elite four-comma club. The Big Five’s total quarterly revenues soared an astounding 28.8% YoY to $365.0b in Q4’20! Quarter after quarter it continues to amaze how companies at such vast scales can manage such incredible top-line growth. Eventually their businesses have to slow, failing to find enough new customers to fuel such big gains.

But the contrast between those Big Five mega-cap techs and the rest of the SPX top 25 is stark. The next-20-largest US companies actually saw their total sales plunge 20.5% YoY to $529.6b last quarter. Part of that is due to the SPX-top-25 mix, with high-flying companies including NVIDIA, PayPal, Adobe, and Netflix soaring into these ranks over the past year. They have far-smaller sales than companies they displaced.

Those included the gigantic oil majors Exxon Mobil and Chevron, as well as mega-bank Wells Fargo. But even accounting for these ranking changes, revenue growth for the rest of the big US companies was generally considerably smaller. Eight of the next-20-largest actually suffered shrinkage, despite that huge liquidity deluge. One subset of these elite companies that really stuck out were the payments processors.

Visa and Mastercard have long been in the SPX-top-25 ranks, despite relatively-small revenues and even profits compared to their peers. With trillions of dollars of freshly-conjured cash floating around, people should’ve been buying lots of stuff. Yet these leading payments processors still saw sales decline 6.1% and 8.7% YoY. That is definitely surprising, with bearish implications about the underlying US economy.

On the other hand, upstart Internet payments processor PayPal saw revenues soar 23.3% YoY in Q4’20. That certainly contributed to it having one of the biggest stock-price gains among large stocks. So maybe more payments are shifting away from the traditional processors. My small business has used PayPal for a couple decades now, and it has served us well. But weakening credit-card activity still bears watching.

The Big Five tech giants dominate on the hard earnings front too, as reported to the SEC under Generally Accepted Accounting Principles. Apple, Microsoft, Amazon, Alphabet, and Facebook collectively earned a mind-boggling $77.9b in profits last quarter, which soared an even-more-amazing 41.2% YoY from Q4’19! Again such growth at their scales is astounding, highlighting the winners-take-most nature of technology.

There is a vast profits gulf between these dominant mega-cap techs and the rest of the SPX top 25. The next-20-largest US companies reported $91.5b of earnings, which edged up just 1.7% YoY. And that is actually way overstated, due to Warren Buffett’s huge investment conglomerate Berkshire Hathaway. It had long been the 6th-largest US company, although the newly-SPX-inducted Tesla just usurped that place.

Buffett himself has long railed against accounting rules that require US companies to flush unrealized investment gains and losses through income statements. So though Berkshire reported huge $35.8b earnings in Q4’20, most of those were due to the surging US stock markets. Although that company’s financial reporting is pretty opaque, backing out investment swings yields real Q4’20 profits of merely $2.5b.

That is less than 1/16th of Berkshire’s GAAP number, a tiny fraction! So excluding that company from the rest of the next-20-largest SPX companies, their total earnings actually shrunk 8.5% YoY to $55.7b. Even though some of this comes from the changing SPX-top-25 component mix, this is troubling. If the biggest-and-best US companies outside of mega-cap techs can’t grow earnings in this environment, when can they?

The many trillions of dollars injected into the US economy by the Fed and US government should have helped the big US companies’ customers buy more from them. Yet that doesn’t seem to be the case. So what happens in 2021 and beyond when that vast deluge of monetary liquidity dramatically wanes? Odds are as that epic money printing seriously slows, Americans will pull in their horns really hurting corporate profits.

Lumped all together, the SPX top 25 saw their total revenues slump 5.7% YoY to $894.6b last quarter. And their total GAAP earnings including Berkshire surged 16.7% to $169.4b. But even despite such very-strong profits growth, their valuations soared. Their stock prices rocketed higher way faster than profits, forcing their trailing-twelve-month price-to-earnings ratios much higher. Valuations remain deep in bubble territory.

Overall the SPX top 25 averaged a scary-high P/E of 96.3x, which skyrocketed a meteoric 258.3% YoY! Thankfully that is misleading, because of the SPX’s monster new component Tesla. That manufacturer of electric cars is a cult favorite, attracting in huge amounts of retail capital at least partially financed by the government’s huge pandemic-stimulus payments over this past year. Tesla’s market cap soared 778% YoY!

Tesla enthusiasts couldn’t care less about earnings or any valuation metrics, as they see this company utterly dominating an all-electric future. They aren’t worried about rapidly-growing competition in Tesla’s markets, convinced it will remain the big winner. All that frenzied stock buying catapulted its stock price to a mind-boggling 1,365.7x trailing-twelve-month profits! This is wildly unsustainable, speculative-mania crazy.

If Tesla’s stock price didn’t budge from the end of Q4’20, and its earnings remained constant, it would take 1,366 years for this company to earn back the price traders are paying for it! The long-term historical average for the US stock markets is a 14x P/E, implying a 14-year payback or a 7.1% earnings yield. Twice that at 28x is dangerous bubble territory. Even fast-growing larger tech stocks can seldom stay over 50x.

No matter how awesome its long-term prospects, sooner or later Tesla’s moonshot stock will be forced to re-anchor with its underlying fundamentals. Interestingly even though this company only earned a trivial $270m in Q4’20, among the worst of all the SPX-top-25 components, that wasn’t from selling cars. Tesla earned $401m in regulatory credits, without which it would’ve lost money. This has been the case for years.

Excluding Tesla’s absurd P/E, the rest of the SPX top 25 still averaged dangerous 41.1x TTM P/Es! And there isn’t much of a difference between the Big Five mega-cap techs and the next-20-largest US stocks. The former averaged 47.4x P/Es at the end of Q4’20, while the latter ex-Tesla weighed in at 39.3x. Not only are these super-risky bubble valuations, but they soared 52.9%, 20.0%, and 65.8% YoY from Q4’19.

This massive “multiple expansion” as Wall Street euphemistically calls it reveals that fundamentals had little to do with the huge stock-price gains over this past year. They were instead driven by those trillions and trillions of dollars of Fed money printing and pandemic-stimulus payments! Even in a very-strong US economy, historically about the best stock markets would offer was valuations trading at half these levels.

Fast-growing market-darling tech stocks might be able to sustain 25x earnings, a growth premium for their big numbers. But 47x is crazy, exceedingly precarious. And normal companies with slower growth might be able to hold on to 18x. So 39x ex-Tesla is incredibly extreme. Stock markets have never been able to hold at levels deep into bubble valuation zones for long. That certainly implies a serious reckoning is looming.

To grow into the rarefied ranks of the 25 largest US companies, all these stocks have great businesses they are adept at running. But no matter how good their operating and financial results prove, eventually their stock prices must reflect some reasonable multiple of their long-term earnings trajectory. If these top US stocks’ prices were cut in half today, they’d still be very expensive. So these bubble extremes have to break.

If these exceedingly-lofty stock prices were driven by last year’s epic capital inflows, what happens this year and next as both the Fed money printing and big government spending taper off? That simply has to translate into less stock demand. As the blistering liquidity-fueled stock-market gains slow, then stop, and finally reverse, momentum selling pressure will overwhelm buying. Then prices will start falling back to earth.

With the average big US stock excluding Tesla sporting an extreme bubble 41.1x trailing-twelve-month price-to-earnings ratio, investors have to be very careful here. History has proven extreme valuations dramatically up the odds of serious selloffs, from major corrections approaching 20% to far-more-serious bear markets often cutting stock prices in half with devastating 50%+ total losses. So caveat emptor way up here!

Ominously a major selloff may already be getting underway, despite the near-record SPX highs recently. The six largest US stocks have all suffered sharp selloffs recently, threatening to spill over into broader stock markets. Apple, Microsoft, Amazon, Alphabet, Facebook, and Tesla saw their stock prices plunge 18.7%, 7.5%, 12.7%, 5.2%, 7.0%, and 36.2% on close over the last month or two! Big selling has arrived.

Moving on to the rest of the quarterly fundamentals, the SPX top 25’s total dividends paid plunged 33.6% YoY last quarter to $30.6b. This is mostly a composition thing though, with high-flying new biggest US stocks not paying dividends displacing older companies that do pay them. The Big Five tech giants’ total dividends grew 5.6% YoY to $7.8b, while the next-20-largest SPX companies’ plunged 41.2% to $22.7b.

Operating-cash-flow generation showed that same massive bifurcation between the mega-cap techs and everything else. While overall SPX-top-25 OCFs in Q4’20 excluding banks climbed 4.1% YoY to $188.9b, all those gains came in the Big Five. Their OCFs skyrocketed 40.4% higher to $118.4b last quarter, wildly better than the 27.4% YoY shrinkage to $70.5b seen in the SPX’s next-20-largest big US companies.

While it is easy to see why Apple, Microsoft, Amazon, Alphabet, and Facebook have attracted such vast swaths of investment capital, these stocks are dangerously overvalued even considering their very-strong growth. And the bigger they get, the harder it will be to keep putting up double-digit growth in revenues and earnings from such massive bases. Last quarter the Big Five averaged $73.0b in sales and $15.6b of profits!

It has to be impossible to keep growing mature businesses at such colossal scales by 10% to 20%+ year-over-year quarter after quarter. The numbers are just too large. And when that blistering growth these mega-cap techs have long achieved falters, their stock prices will likely fall hard given their extreme bubble valuations. As their recent sharp drops prove, even these fantastic companies won’t evade major selloffs.

While those trillions and trillions of dollars of new money force fed into the markets over this past year make contrarians look like fools, I remain one. The odds still favor a long-overdue stock bear rearing its ugly head as those vast liquidity injections wane. After decades of studying stock-market history, it is very clear that stock prices can’t stay super-disconnected from underlying corporate earnings at bubble levels for long.

So realize today’s crazy-euphoric and hyper-complacent stock markets remain very dangerous, still at risk of a serious imminent selloff. That may just be a correction approaching 20%, but with valuations so extreme a full-blown bear market exceeding 50% is increasingly likely. Those are necessary from time to time to maul stock prices long enough for earnings to catch up, normalizing excessive speculative-mania valuations.

The classic bear-market strategy is selling stocks and holding cash. If a bear market cuts stocks in half, holding cash through it doubles purchasing power so twice as many shares can be bought back once it runs its course. But cash not only doesn’t appreciate, the Fed’s radically-unprecedented pace of money printing is rapidly eroding the US dollar’s value. This epic currency debasement changes bear strategy.

That naturally leads to much-higher gold investment demand, driving the yellow metal’s price higher as bears ravage bubble-valued stock markets. As gold powers higher on balance, the major gold stocks tend to leverage its advance by 2x to 3x. Since gold has been stuck in a miserable momentum selloff in recent months, it and its miners’ stocks are very beaten-down making this a great time to buy in relatively-low.

Since the Fed can’t artificially stave off the long-overdue bear forever, it is essential to cultivate excellent contrarian intelligence sources. That’s our specialty at Zeal. After decades studying the markets and trading, we really walk the contrarian walk. We buy low when few others will, so we can later sell high when few others can. We can help you both understand these markets and prosper in them, even during bears.

The bottom line is big US stocks’ recently-reported Q4’20 results revealed that US stock markets remain dangerously overvalued deep into risky bubble territory. All the revenues, earnings, and operating-cash-flow-generation growth is still concentrated in that handful of beloved mega-cap techs. There is a stark bifurcation between them and the other largest US companies, which are seeing fundamentals deteriorate.

And neither the Fed nor the US government can sustain the extreme pace of money printing and stimulus spending that catapulted US stock markets higher in 2020. That radically-unprecedented flood of trillions and trillions of dollars is already slowing. As those epic liquidity injections wane, these Fed-goosed stock markets face a serious reckoning as stock prices mean revert back down to some reasonable multiple of earnings.

We’ve long published acclaimed weekly and monthly newsletters for speculators and investors. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. We’ve recommended and realized 1178 newsletter stock trades since 2001, averaging outstanding annualized realized gains of +24.0% over that multi-decade span! Subscribe today to see our trading books full of cheap fundamentally-superior gold stocks.

Adam Hamilton, CPA

Copyright 2000 - 2021 Zeal LLC (www.ZealLLC.com)

********