Central Planning Vs. Economics

We have spilled barrels of electronic ink, making the point that central banks are wreaking havoc. They hurt the poor, the middle class, and the rich. They hurt the wage earners, the business owners, the investors (aka the “rentiers”), and the pensioners. They have variously inflicted rising interest rates, too-high rates, falling rates, and too-low rates. They have imposed perverse incentives to destroy capital and consume wealth.

Those discussions focused on the specific injuries, their causes and effects. An analogy is studying the damage done to the body if it is cut by a sharp blade, bludgeoned by a blunt instrument, burned by a hot flame, or poisoned by a toxic chemical. One can study these things in excruciating detail, without considering one thing.

Cutting or burning the human body is the negation of biology. Biology, as such.

The body works in a certain way, and these attacks negate this functioning. They act against biology. To the extent that they succeed in damaging the body, they render biology inoperable.

Fortunately, medical doctors do not wound or poison their patients. However, economic doctors do precisely that. One reason is that few recognize economic wounds. It is quite controversial to say that all government interference in the market is injurious.

A free market is nothing more than when someone can make something and sell it to someone else at a mutually-agreeable price. This simple idea is under assault from all sides. If the safety of a thing is deemed important, then most people feel that the government should somehow make it safe. The result is a body of regulations to which producers are forced to comply. The manufacture of automobiles is an example.

If a majority of people believe in universal access to the thing, then they cry that the government must guarantee that everyone gets it. Public schools is an example.

If people care about the price of the thing, then they want the government to somehow ensure that everyone pays a good price. Rent control of housing in crowded cities is an example. Or, if they want people to be paid a good price then the government dictates a minimum wage.

Each of these examples is a case of central planning. In central planning, bureaucrats attempt to order the economy by a political process. A political process is the opposite of a market process. That is, to production and trade, which we described like this:

“…when someone can make something and sell it to someone else at a mutually-agreeable price.”

Central planning is more like this:

“…when a bureaucrat, based on political considerations, tells someone what to produce, how to produce it, how not to produce it, who to sell it to, who not to sell it to, the minimum or maximum price.”

It should be obvious why central planning always fails. Production has conditions, and if producers are not allowed to meet this conditions, then they cannot produce. Venezuela has rediscovered what Emperor Diocletian discovered, after he imposed his Edict on Maximum Prices in AD301.

You cannot produce a thing that you are forced to sell below cost.

People call this unintended consequences. Are the consequences really not intended? We believe some people do want the negative consequences that always and everywhere ensue. Others may seem not to want them, yet keep advocating the same thing while wringing their hands that they want a different result. Rather than focus on the alleged intentions of the politicians or voters, we prefer to call it perverse incentives. The consequences of perverse incentives are perverse outcomes.

Congress and bureaucrats cannot create better outcomes by decree. The only power the government has is force. It can prevent someone from making something, or stop someone else from buying it. In regard to safe cars, the government can only outlaw the sale of cars that do not have their mandatory features. They cannot make such features affordable to everyone, but they can prevent some people from buying cars.

The only power the government has in regard to schools is to take away the money people would have used to pay for the education of their children, and thereby prevent private school businesses from offering education services.

The only power the government has in regard to housing is to render it unprofitable to build more units, or even maintain existing units. The only power the government has in regard to wages is to make it illegal to hire someone who produces below the government’s threshold. You cannot pay someone $15 who produces $10 in gross margins of burger.

Wages do not rise because a central planner decrees them to (though the average wage, as reported by labor statistics, may rise because all those who produce below the threshold are rendered unemployable, and hence removed from the statistic). Wages rise as a consequence, when productivity rises.

The idea of a free market is not popular right now. Most people claim to prefer to have safe cars, free schools, affordable housing, and high wages. They feel there is a conflict with free markets, and they trust central planners to somehow deliver the things that free producers would not.

And lollipops.

This is our term for magical thinking. When someone proposes to hike the minimum wage to $15, pay a universal basic income, or give out free college education, we suggest asking a simple question.

“Would you like a lollipop with that, sir?”

Serious economists—we exclude the partisan hacks like Krugman and the socialist tools like Piketty, who prostitute themselves for grants or power—don’t generally advocate lollipops. Except in monetary economics. Thus, we coined the term otherwise-free-marketers. These otherwise-free-marketers can explain why attempts at central planning of cars or wages do not work. But when it comes to money and credit, they revert to central planning.

They variously believe that the central bank is able to control rising prices—now Paul Volcker is being lionized for just this feat—employment, and even GDP (the latest darling idea is that the Fed should target GDP). Lollipops, we say!

These views are not just for socialists. They are advocated by the otherwise-free-marketers. These folks sit on the boards of pro-reason and pro free-market think tanks. They are otherwise-serious economists who don’t grasp something. Dictating the price of credit in the hopes of improving outcomes is just wishing… for lollipops.

The arguments against central planning in those other cases, such as cars, may not be popular, but at least they are well-understood. There are both theoretical arguments (Keith made one in his dissertation) and empirical studies to support the idea that people are more productive, hence prosperous, when they are freer.

The arguments against central planning of money and credit are not popular nor well-understood. We have made many, and will make more. But today, we argue the idea that central planning negates economics as such. Let’s look at why.

Biology studies “...life and living organisms, including their physical structure, chemical processes, molecular interactions, [and] physiological mechanisms…” Cutting an animal’s heart, burning its lungs, injecting cyanide, or putting a bullet into its head attacks life itself. It destroys the physical structure, interrupts its chemical processes, blocks molecular interactions, and renders physiological mechanisms impossible. Attacking an animal negates its biology.

Wikipedia defines economics as the study of “…production, distribution, and consumption of goods and services.” We aren’t entirely happy with this definition, but let’s go with it.

A living organism has structure, processes, interactions, and mechanisms. In order to continue to be alive, these things must operate in a certain way. Injury causes dysfunction, reducing an organ’s capability to sustain life.

An economy also has these things. Its structure, processes, interactions, and mechanisms are working properly when “someone can make something and sell it to someone else at a mutually-agreeable price.” Government intrusion causes dysfunction, reducing someone’s capability to produce and someone else’s to consume.

The central planners play at economics. They have formulas that purport to tell them how to improve outcomes. And of course voters who clamor for safer cars, lower rents, and higher wages. They cannot deliver these things (though they can claim credit for whatever people produce in spite of their interference, and the useless ingredients they force producers to add). They can only block the production of cars, the construction of housing, and the hiring of workers.

For all their economic calculamation (to coin a word as ridiculous as the notion of central planning), they are not doing economics. They are negating economics. The way a Viking negated biology by stabbing a spear into someone’s belly.

It’s bad enough when they calculate the temperature that a food truck BBQ smoker has to be. It is incalculably worse when they calculate what the interest rate must be.

Market Report

We apologize for missing a week. We continue to be very busy developing the business of offering a yield on gold.

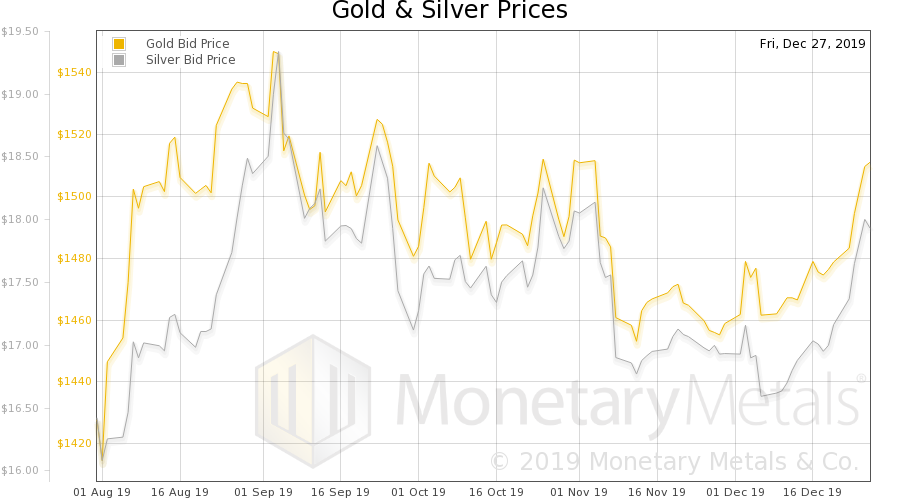

This prices of the metals rose $35 and $0.82. But, then, the price of a basket of the 500 biggest stocks rose 62. The price of a barrel of oil rose $1.63. Even the euro went up a smidge. One thing that did not go up was bitcoin. Another was the much-hated asset in the longest bull market. We refer to the US Treasury.

The spread between Treasury bonds and junk bonds narrowed this week. It is now close to its post-crisis low. While many would cheer this cheapening of the cost of credit to below-investment-grade issuers, we note two things. One, this enables them to borrow more to spend more and thus add to GDP. Two, this is not a recommendation of forcing down the cost of credit to marginal borrowers. It is a damning indictment of GDP as a measure.

Whatever the word is, when there is an increase of borrowing to consume wealth, “growth” is not that word.

Yet this is our world. This is held up as proof of a strong economy.

Keith had a bizarre encounter on social media. He said that when the government borrows, it adds to GDP. An otherwise-free-market economist chimed in to say that it does not, and said that transfer payments are not included in GDP. Indeed, but if the government doles out $1,000 to Joe Six-pack, and Joe buys $1,000 worth of beer, that adds to GDP. Next, this otherwise-free-marketer quibbled that well Mark Millionaire spends less. It went round and round.

And then it suddenly became clear. They cannot admit that borrowing to consume adds to GDP. For if they do, they concede the case against Fed GDP targeting. So to head that off at the pass, they have to deny this fact.

How many of the companies rated below investment grade are zombies—which the Bank for International Settlements defines as profits < interest expense? It is not sustainable to borrow more to pay some of the interest expense. Not even if the interest rate keeps falling.

This is just another mechanism of capital destruction. Though new capital is being produced by productive enterprises, capital is finite. No one can say when this process will blow up. But we can be certain that it will.

Let’s look at the only true picture of the supply and demand fundamentals of gold and silver. But, first, here is the chart of the prices of gold and silver.

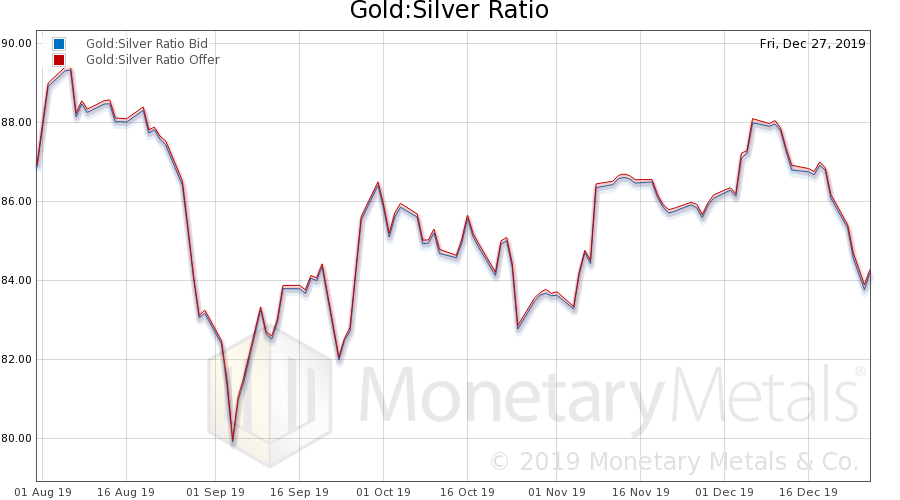

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). The ratio dropped this week.

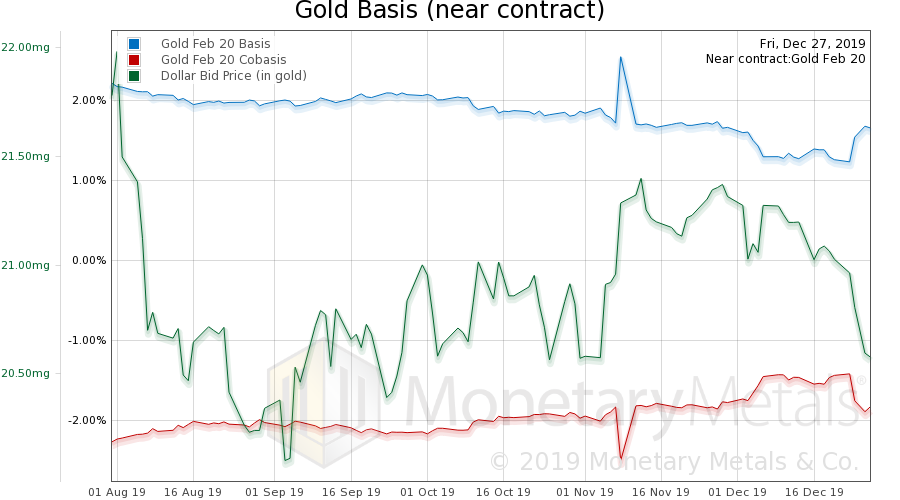

Here is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold.

With the big drop in the dollar (which the muggles see as a rise in the price of gold), we observe a drop in the scarcity of gold to the market. They are selling more gold metal, at the new, higher price.

Nevertheless, the Monetary Metals Gold Fundamental Price—the price at which metal would clear, if it weren’t for leveraged speculators in the futures market—was up $10 over the past two weeks, to $1,480.

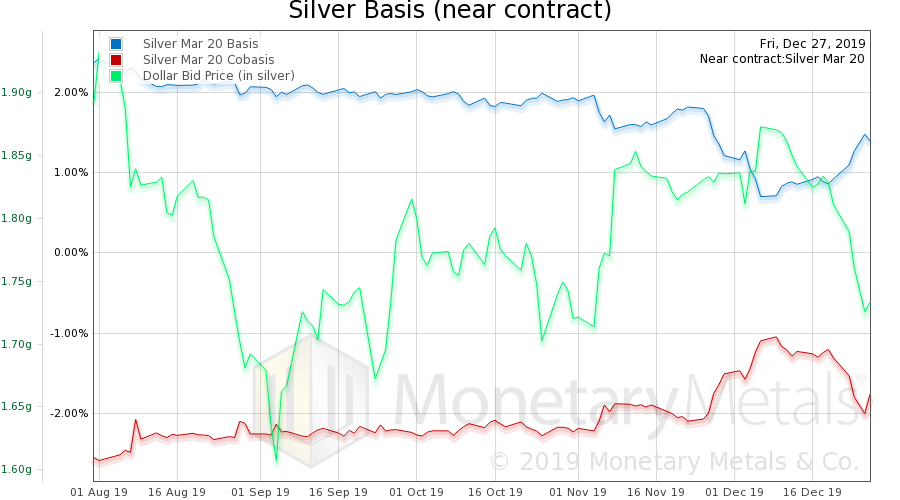

Now let’s look at silver.

The same thing happened in silver, the dollar dropped (i.e. price of silver rose) and more people were happy to trade silver in exchange for more of those slips of paper that people yet call money.

The dollar, as measured in silver, fell a lot, but the cobasis did not fall so much. So the Monetary Metals Silver Fundamental Price rose 43 cents, to 17.35.

© 2019 Monetary Metals

********

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.