Clearing The COMEX Decks

While not the only consideration in forecasting price, it's always important to note the current COMEX contract balance. As the FOMC meets again this week, let's look under the hood to see whether or not positions are at extremes versus recent history.

As you know, this has already been a strong year for COMEX Digital Gold. Price ended 2019 right at our forecast of $1520, and it has already met our 2020 forecast of $1750-1800. See more here: https://www.sprottmoney.com/Blog/gold-and-silver-2...

So is that it? Will price now fall through the remainder of the year? Last Friday's U.S. jobs report certainly brought many of the perma-bears out of hibernation, with rushed forecasts of steep price drops ahead. However, a sharp drop in COMEX prices is usually caused by a wash out of overly-exuberant speculators, many of whom had placed unusually large and aggressive positions. Taking the short side of these trades is almost always a bullion bank trading desk. Thus, when Spec positioning gets crowded long, Bank positioning is always heavily short.

To determine whether or not the COMEX trade is getting crowded and due for a "wash-and-rinse" cycle, we usually consult the CFTC and CME-issued market data. The three key items are:

• the daily COMEX contract open interest reports

• the weekly Commitment of Traders reports

• the monthly Bank Participation reports

Let's look at all three to see where we stand on a relative basis versus history and price.

First up is total open interest. After peaking at an all-time high of 799,541 contracts on January 15 of this year, total COMEX gold open interest has consistently fallen. In fact, there's even some speculation that Banks are quickly exiting this market after taking an absolutely disastrous beating on March 23 and 24: https://www.reuters.com/article/us-health-coronavi...

As of Monday, total open interest has declined all the way back to just 469,893 contracts. From the January peak, that's a drop of over 41%...and this at a time of rising prices, overt QE∞, and market volatility! Perhaps The Bullion Banks really are rapidly exiting this fraudulent sham of a digital derivative market?

But for this post, it's more important to note that the total COMEX gold open interest has retreated back to levels not seen since early June of last year. And where was price back then? It was just beginning its rally that began on May 28 at $1280 and continues unabated today. Thus, from a total OI perspective, the decks have been cleared.

Now let's turn to the CFTC-generated Commitment of Traders report. If total open interest is down, then you can expect Spec positioning to be low, too. And it is. In fact, total Spec positions are also the lowest seen since early June of 2019.

On the most recent legacy CoT report, the "Large Speculators" were NET long about 219,000 COMEX gold contracts. That may sound like a lot, and it is. However, it's nowhere near the all-time high of 353,649 contracts shown on the report surveyed February 18, 2020. Additionally, a Large Spec NET position of 219,000 contracts is the smallest reported since June 18, 2019. And where was price that day? About $1345...a full $380 lower than where it is as I type.

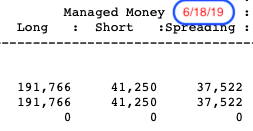

Perhaps you like to dig into the weeds and prefer the "disaggregated" CoT report? OK, then, let's compare the "managed money" positions from that same June 18, 2019 report versus the most recent. As you can see below, this group of traders is actually holding a smaller NET position now than it was a year ago...again with prices nearly 30% higher. There's no "Spec bubble" here:

Finally, let's check the Banks' self-reported positions as shown in the latest, CFTC-generated Bank Participation Report. This monthly report alleges to summarize the positions of the 4-5 largest U.S. Banks trading on COMEX as well as the 20-25 largest non-U.S. Banks.

If you understand the COMEX, then knowing that total OI and Spec positioning is the lowest in a year should lead you to believe that Bank positioning is also relatively low...and it is. After peaking at 225,111 contracts NET short back in January, the total Bank NET position is the lowest seen since last June AND almost identical to every June since 2016. See below:

• On 6/7/16 and with price at $1247, the combined Bank position was NET short 133,296 contracts

• On 6/6/17 and with price at $1297, the combined Bank position was NET short 176,487

• On 6/5/18 and with price at $1302, the combined Bank position was NET short 132,788

• On 6/4/19 and with price at $1329, the combined Bank position was NET short 141,028

• Last Tuesday, with price at $1734, the combined Bank position was NET short 134,326

So, when prices inevitably resume their 2020 rally, you need to know that "the decks have already been cleared" in terms of Spec and Bank positioning as well as total contract open interest. As such, it's time to re-assess and adjust our price goals for 2020. Since this bull market began on May 28, 2019, price has generally moved up in $100 increments, stopping each time at the associated $80 level...meaning $1380, $1480, $1580 and so on. See for yourself:

Thus, it's reasonable to expect that once price clears $1780 later this summer, a move toward $1880 will follow, with perhaps even a peek at the old all-time highs near $1920 before another pullback and consolidation.

So, what's the purpose of this post? Price may do just about anything in the short term and in the aftermath of the FOMC meeting on Wednesday of this week. However, there is no truth to the notion that the COMEX positioning is "extreme" and "due for a washout". In fact, the opposite is true, and the potential clearly exists for another rally to new 2020 highs in the weeks ahead.So, what's the purpose of this post? Price may do just about anything in the short term and in the aftermath of the FOMC meeting on Wednesday of this week. However, there is no truth to the notion that the COMEX positioning is "extreme" and "due for a washout". In fact, the opposite is true, and the potential clearly exists for another rally to new 2020 highs in the weeks ahead.

About Sprott Money

Specializing in the sale of bullion, bullion storage and precious metals registered investments, there’s a reason Sprott Money is called “The Most Trusted Name in Precious Metals”.

Since 2008, our customers have trusted us to provide guidance, education, and superior customer service as we help build their holdings in precious metals—no matter the size of the portfolio. Chairman, Eric Sprott, and President, Larisa Sprott, are proud to head up one of the most well-known and reputable precious metal firms in North America. Learn more about Sprott Money.

The views and opinions expressed in this material are those of the author as of the publication date, are subject to change and may not necessarily reflect the opinions of Sprott Money Ltd. Sprott Money does not guarantee the accuracy, completeness, timeliness and reliability of the information or any results from its use.You may copy, link to or quote from the above for your use only, provided that proper attribution to the source and author is given and you do not modify the content. Click Here to read our Article Syndication Policy.

*********

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.