Divide And Conquer – American-Style

It was several months ago in the midst of heated and widely-accepted civil disobedience, looting, and civic trespassing by members of Antifa and the Black Lives Matter movement that I opined that the “demonstrations” (as opposed to “armed insurrections”) in cities like Portland and Seattle were not symptomatic of left-vs-right, white-vs-non-white, or liberal-vs-conservative divides cleaving American society with butcher-like finality. I said then and I say again now that these blatant examples of unlawful social unrest were (and are) the direct result of the fiscal and monetary policies of the banco-politico cartel and their precision-like and very purposeful implementations. The result is a bifurcated economic divide between those that “have” and those that “have not”. As the brilliant humourist George Carlin once said “It’s one big club and guess what? You ain’t in it.”

In four days, the most powerful nation on earth installs a new Commander-in-chief, amidst a battle-zone Washington backdrop with the National Guard and the military displaying a presence never before seen at a presidential inauguration. In fact, one of those lame media sources was complaining that it was a “sad state” when celebrants are vastly outnumbered by armed security lest that dastardly throng of “deplorables” attempt another assault.

As a former resident of the U.S., I see a nation that now has three two-level chess game being played out with one contest between the polarized masses (Antifa, BLM, anti-trump, pro-Trump) and the second and much more important contest being between those fortunate members of “the club” (the “haves”) and those destined for eternal exclusion from “the club” (the “have-nots”). Make no mistake, the far more insidious contest is the latter because integral to the maintenance of the status quo in America is the surgical division of the “have-nots” while creating a “Divide-and-Conquer” narrative pitting one side versus the other. The mainstream media (particularly CNN) cannot go ten minutes without pounding the drum for a second Trump impeachment and conviction, an event that would prevent the disgraced leader from ever again seeking Federal office and which would eliminate his pension and his security staff. The sad reality is that the media cannot see the forest for the trees and by way of the Trump obsession and hatred, they play right into the hands and pocketbooks of the banco-politico cartel, mesmerized by symptoms yet ignorant of causes. When they allowed the corporate elites to gut America’s middle class by exporting the manufacturing sector to China and Mexico, they were inviting an equal and opposite reaction. All in the name of “globalization” and now it has returned home to bite them squarely in the backside.

It was one year ago today that I posted a picture of the CNN Fear-Greed index sporting a near-historic 97 reading for “Extreme Greed” and while the number is somewhat subdued today at 60 (“Greed” without the “extreme”), I find that astonishing given the deflationary headwinds that now prevail. In fact, I find myself in the same quandary today that I was in last January where monetary policy was decidedly bullish for precious metals but where the technical action for the shares was tentative at best. I opted to stay way from the big miner ETF’s (GDX and GDXJ) ultimately re-entering on March 16th (GDX sub-$20) in what was my best call for 2020 but here in January of 2021, there are two conditions combining to create a formidable headwind – the long overdue rebound in the USD index and the overvaluation in the broad stock markets.

Now, there are those precious metals gurus out there that have been calling for $5,000 gold and $400 silver since 2002 with dozens upon dozens of junior mining recommendations now in the graveyard of broken dreams and failed expectations. I do not aspire to join that group which is why I keep the number of companies I cover down to less than half a dozen because close attention to the few yields far superior performance than peripheral attention to the many.

My bullish case for the commodities sector as a group and precious metals as the centrepiece lies in my use of history as a roadmap for asset and sector allocation. The main argument for inflation being proffered by the analytical community for 2021 and beyond is central bank policy initiatives couple with fiscal stimulus. Massive increases in the supply of currency units the world over chasing finite supplies of goods and services can only result in a reaction in the cost or price of those goods and services. That is econ-101 right from the textbook. However, from a demand-supply standpoint (assuming finite money supply growth), there are two different types of inflation: demand-pull inflation (like 2002-2011) saw voracious Chinese demand for commodities like iron ore and copper pull prices higher and cost-push inflation (like the 1970’s) where restricted supply creates shortages (oil) resulting in higher input costs that in turn are reflected in inflated end-user or consumer prices.

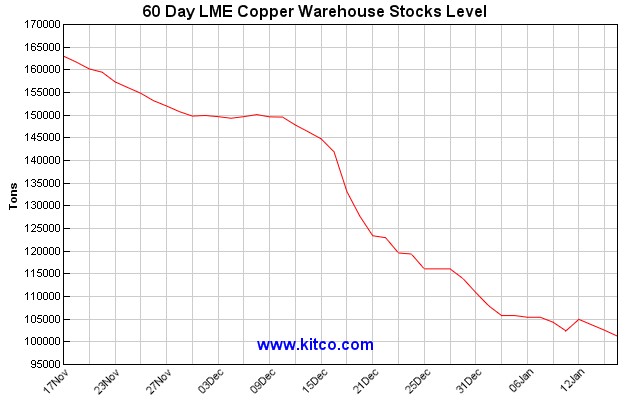

While the pandemic has seemingly caused a deflationary decline in demand, the offsetting fiscal and monetary stimulus handed out by the central banks and their government puppets has largely wound up in elevated stock and real estate prices, the latter being the ultimate collateral for the member banks. However, once the stimulus effects dissipate, demand must naturally soften so demand-pull inflation is unlikely. On the other hand, the globe is now running a very real risk of a disruption in the supply chain for all commodities including iron ore and particularly copper, where LME inventories are plummeting to 5-year lows.

The result is that assuming the vaccine is effective (and that is an enormous “if”), the normalization of global demand is going to be challenged by the supply problem. Even if it takes longer for the global economy to recover, the supply disruption is going to create dislocations around the globe resulting in ultimately higher prices everywhere. That brings us to the short-term outlook for the precious metals and the commodities sector.

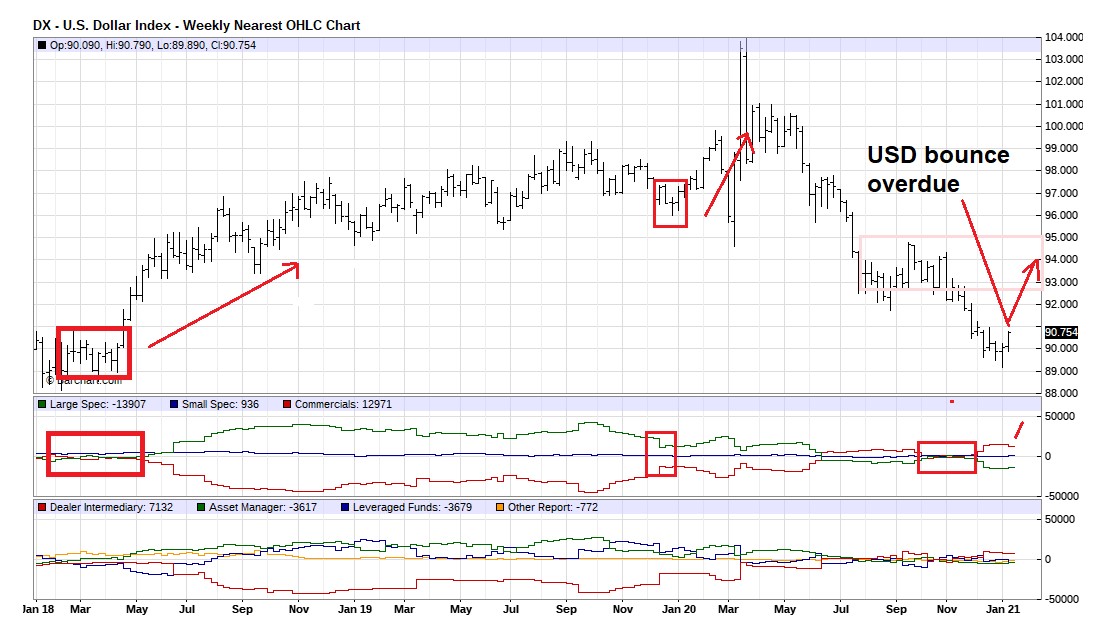

The short-term pricing structure is being dominated by the USD Index where the recent COT report shows a lob-sided long position held by managed money versus an equally lob-sided position held by the commercial traders. On Friday, the USD had a sharp rebound and the result was a $24 drop in gold, a $.97 drop in silver, a $.063 drop in copper, and a $1.42/barrel drop in crude oil. I see the potential for a move to 93-94 for the USD Index which would invite even more algo-driven computer bombings in the commodities pits for at least the next two weeks and while the inauguration week might see the return of the U.S. dollar rout, rebounds usually take longer.

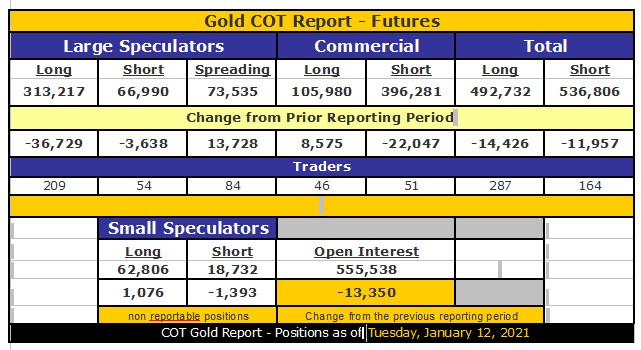

As for the gold and silver arena, I have spoken about the Commercial trader short position being in the historically hostile 300,000-plus rage for what appears to be an eternity and I commented last week after that Friday’s USD $78 crash that the COT would undoubtedly see Commercial short-covering “of substance” along with a purge in the massive long position held by Large Speculators (350,000 contracts). Well, one look at this week’s COT and now you know why the regulators turn a blind eye to bullion bank interference in the Crimex futures pits: there is just too much money on the table.

Given the rout we just went through this past Friday, in everything, expect the Commercials to have covered even more which is bullish looking out a few months but it can take weeks of Spec long liquidation and bullion bank short covering before a tradable bottom appears. Is this what I expected once 2020 tax-loss selling ended? The answer is “yes” as to the move in the HUI from under 300 to over 325 but “no” as to the mid-January crash to 284.

The gold chart looks less-than-friendly with major support now at USD $1,775 and that big oppressive downtrend line sitting at USD $1,950. If the USD rally persists next week, we could see a test of support in a hurry.

Silver WAS in better technical shape than gold but now that the 100-dma at USD $25.14 has been breached, there is a little support at $24 but much larger support at $22.50 and again, it appears to be all USD-related.

We remain in a period of strong seasonality for precious metals and the miners and as there is no argument about the strength of the fundamental case for gold producers given the extraordinary vault in free cash flow, that argument is largely falling on deaf ears. To the extent that investors could care less about the extraordinarily weak fundamentals for companies like Tesla, where free cash flow is non-existent, one has to ask at what point do prices start to reflect anything fundamental? Like the rest of you, I see that tweets out there where portfolio managers and newsletter writers keep asking why the miners are acting so poorly, given the profits they are generating, and the only answer I can muster up is this: we better pray that the action in the miners is not a barometer of future metals prices. We better pray that the historical “lead indicator” status of gold and silver mining share prices is a “fake-out” brought about by temporary pandemic-related aberrations in price behaviours. For now, I am going to lay blame at the foot of the USD dollar “crowded trade” altar and when the current bounce exhausts itself, I will reassess. If the bear market in the USD resumes and our metals fail to rally, I will be forced to reduce exposure across the board.

In the interim, rabbit’s feet, four-leaf clovers, salt-over-the-shoulder, and Midnight Masses are in order stacking Lady Luck and the other relevant deities on our side. And add Jack Daniels as a back-up...

Disclaimer

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

********