FOMC At Center Stage

Below are the Opening Notes and Bond Market segments from last Sunday’s edition of Notes From the Rabbit Hole, NFTRH 530. Jerome Powell was actually more firm than I expected. Atta boy Jay! Aside from my prognostication the more important stuff (IMO) begins at the 4th paragraph. That is where I put on my tin foil hat and tell what I think. It does seem to dovetail with what we saw today out of the Fed chief.

Opening Notes: FOMC at Center Stage

It is likely that the Fed is going to raise the Funds rate on Wednesday because this is a confidence game and a Fed suddenly showing weakness and doubt could exacerbate the market’s already frayed nerves. As a side note the 76% reading of CME futures traders expecting the hike to happen has not changed in the last few weeks.

But US and global authorities can read charts and as a person with some short positions I am well aware that they have people who can read charts as well. It’s not complicated; the market (SPX) needs to hold here or it could be an express (or possibly a slow moving) elevator to SPX 2100.

So I am guessing that we get the hike but we also get language that will talk of ongoing economic strength with some soft patches. They will talk about standing ready to adjust policy as needed and they will not talk much if at all about inflation as a concern. They may even mention a recent decline in inflation expectations, which would be code for ‘it’s just a moderate situation right now but if this thing rolls over and liquidates we are going to eventually attempt to inflate our way out of it’. Notice the words “eventually attempt” in my theoretical response?

Inflation is what the Fed does, after all. But it needs periodic deflationary episodes in order to keep the racket going. I will stick with my original view that the Fed is not adverse to a market correction or even a bear market. It is exactly what is needed to reload the next inflation gun.

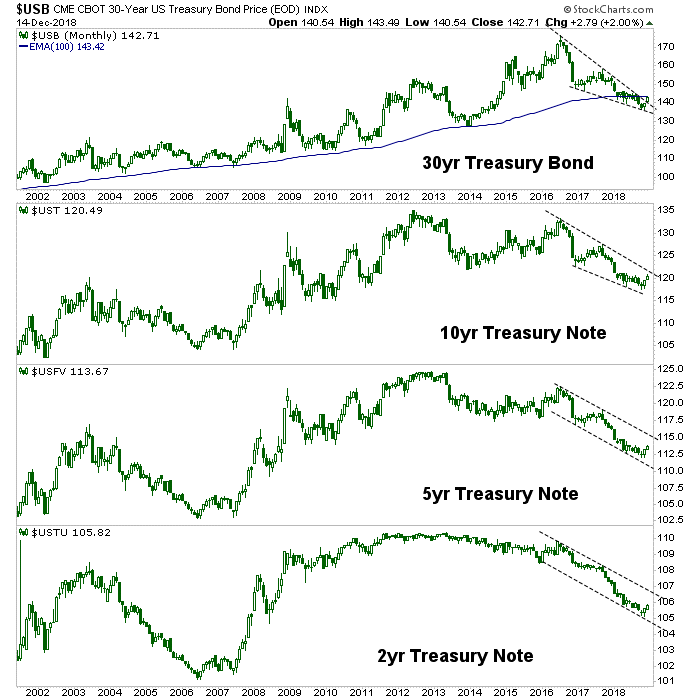

The “BOND BEAR MARKET!!!” stuff ran very hot on this cycle as the 30 year yield broke the Continuum’s limiter (monthly EMA 100) before failing over the last few weeks (to the surprise of many, but not us ;-)). As I have noted previously, in my opinion the Fed does not want a bond bear (breakout in yields) or its running mate, a breakout in inflation expectations because the Fed is an inflation machine. But it has inflated against this pleasant continuum of declining yields over the decades that has encompassed the entire training of most of us as market participants.

I am not saying that a red dashed line is the be all end all of market analysis. But it is a marker that we have used in NFTRH since 2008 in order to correctly interpret the macro situation. My interpretation today is that the Fed has countered the cost-push inflationary pressures that by definition are injected through fiscally (political) stimulative policy by withdrawing liquidity until something breaks. Ironically, that has involved raising the Fed Funds interest rate and withdrawing QE, which theoretically would raise long-term yields. But when something breaks, the risk ‘off’ herds buy the bond driving yields down.

Bond Market

Let’s flip the yield over and take a look at the long bond and its monthly EMA 100. It is no coincidence that the bond broke down after Trump – and all that fiscal policy to follow – was elected. The Fed was hanging out there with a QE bloated balance sheet and an abnormally low Fed Funds rate. I believe this was an untenable situation for the Fed.

Again, if you buy the theory that the bond market has been a funding mechanism of sorts for the very long-term inflation operation, the Fed would not want to see that mechanism destroyed. Look at the decline in various bonds since the election. ‘Enough is enough!’ (one might imagine) says the Fed. Tin foil hat affixed, I say that the Fed wants to slow the fiscal reflation, which came along inconveniently after the Bernanke Fed had unleashed epic and historically experimental monetary policy upon the markets. Let it sink in a bit, fiscal (political) vs. monetary (Fed) and think about Trump vs. the Fed.

NFTRH.com and Biiwii.com

More from Gold-Eagle