Gold: America The Bubble

America itself has become the largest bubble in economic history. The progression of bubbles from equities, to corporate credit, classic cars, Da Vincis to bitcoin, have expanded in scope and risk becoming an insidious process. Today, almost every asset class is up thanks to our central banks, led by the Fed, printing enormous amounts of new money such that their combined balance sheets topped $20 trillion or one third of the world’s GDP, after purchasing their respective government debt in massive amounts. Now, a second massive injection of liquidity is to hit the markets with the largest tax overhaul in the United States expected to boost the economy and further extend the market’s winning bull run. Dow 50,000? Possible, since we believe the stock market no longer is a discounting mechanism but a manifestation of the world’s biggest bubble. Keynes would be proud.

Consumer confidence is at 17-year highs, unemployment at 4.1 percent, a 17-year low. Oil soared to 4-year highs. Surprisingly, the US stock market’s performance is overshadowed by bitcoin mania, surpassing the Dutch tulip bubble, dot.com bubble and even the tech bubble. Greed has pushed valuations even higher. Of concern is that while the ultra loose policies have finally boosted activity, the revival has awakened long-dormant inflationary pressures.

Debt, Debt And More Debt

After almost a decade of low interest rates, a borrowing binge pushed debt and asset prices to record levels. This voracious appetite for debt lies at the heart of this boom which will end in a bust. Governments are now a larger share of the economy, thanks to an increase in public borrowings. US government debt alone is the world’s largest at $14.5 trillion. As a result, most central banks serve as major creditors to their respective governments, posing a problem particularly when rates turn-up, creating a spate of losses and sovereign debt crises. The low interest rates also forced investors to chase returns on riskier credits. Markets have become addicted to low rates and like any addiction, needs lower and lower rates in higher doses. Although blue-chip companies such as Microsoft and Apple have balance sheets choking with cash, they raised even more debt taking advantage of the ultra-low rates. Corporations added a whopping $1.4 trillion of debt last year.

But now, US treasury yields are at their highest since March amid central banks’ promises to tighten. Yet complacent investors have ignored the threat believing that the minuscule rate increases last year and asset sales would be offset by the Republican tax cut. And under departing Fed Chair Yellen’s promise to “normalize “, the Fed’s balance sheet still stands at $4.4 trillion after a $6 billion or 0.14 percent reduction. Normalization it seems will take at least a decade at this rate.

Having pursued monetary laxity, governments saw their debt loads soar to the point that the debt in bubble-prone United States has grown from $10 trillion to $20 trillion in less than a decade such that today their debt to GDP is over 100 percent (before entitlements). Put another way, US debt is equal to its entire annual economic output, worse than many Latin American or European countries. Instead of needed cuts in spending and entitlements, the Republicans instead chose sweeping tax cuts, and financing the revenue shortfall by adding more debt, a recipe for disaster as they try to print their way to prosperity.

And tellingly, the US dollar suffered its worst annual performance in 14 years declining by some 12 percent and in fact is lower than when Trump was elected. Trump’s recent musings raised fears of a “stealth” currency war, angering and unnerving allies, pushing the greenback lower. A lower dollar however will help boost the US economy but also revive the inflationary fires because no one yet has taken the punch bowl away.

Inflation Is Back

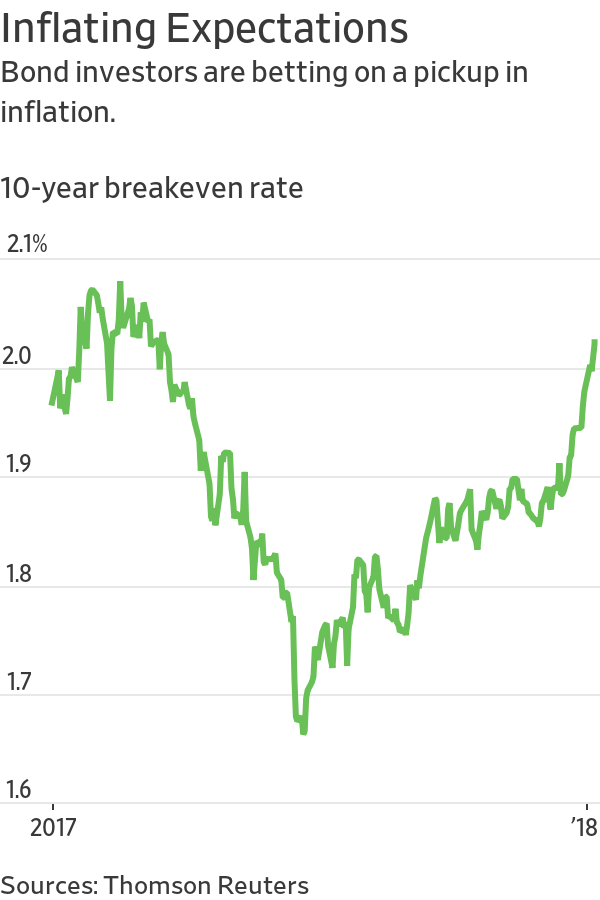

While the US stock market rose almost 20 percent last year, Europe did even better, with a 27 percent gain on hopes for a continuation of the global boom. While no doubt there is a need for a short-term market correction, we believe that markets will continue to ignore the systemic risk imbalances and excesses caused by the greatest bubble ever. The bubbles will get even larger. Commodities are at three-year highs as investors pour money into everything from oil to copper. Gold topped $1,300 an ounce just when the central banks gave up on inflation. History shows that a resurgence in inflation follows a series of bubbles. Like the seventies, we are at the beginning of the inflationary cycle.

America has fallen further behind their economic rivals, particularly in the Far East because they emphasized consumption rather than investment. Looming trade disputes with Japan, China, South Korea and even Canada will test Trump’s “America First” policy, made worse if there is a government shutdown.

And just when inflation is declared dead by our central bankers, we believe inflation is back. A leading indicator, commodities are at three-year highs as both hurricanes and now cold weather roil the commodity markets, not too dissimilar when the anchovies went missing off the coast of Peru which helped push inflation to double digit levels in the seventies. Energy is at four-year highs on Middle East woes and the ultimate indicator, the stock market, posts yet another all-time high.

Who Will Pay The Piper?

America’s consumption binge is the root of the problem and the alchemy of debt-financed deficits allows them to spend their way to prosperity. Simply America’s economic expansion was a giant experiment in the reliance on credit. Yet like others before that have tried to do so in the past, the US thinks it is different this time.

American consumers’ voracious appetite to keep spending for homes to cars to bigger flat screen TVs allow its trading partners to sell them goods and services in undervalued currencies. Money flowed into the United States. This recycling arrangement worked for some time but the flow of funds recently shifted when America introduced negative interest such that foreigners became reluctant to subsidize dollar-denominated assets. China’s vast $3.3 trillion of reserves has already shrunk by one trillion dollars from their peak. And with lower energy prices, the Middle East players have dumped dollars to fund widening budget deficits. America’s vulnerability is the linkage between its deficits and the rest of the world and noteworthy is that America’s creditors are the same players that are being targeted by Trump as currency manipulators or economic rivals. As such, there is a huge dollar overhang, ripe for a correction. This avalanche of dollars is an accident ready to happen.

A larger danger is that the exponential increase in the budget and tax cuts must be financed because Americans have little savings and are heavily reliant on foreign savings. We remain concerned that foreigners who financed America’s debt clogged financial system will resist holding an ever-increasing share of their wealth in US securities and demand higher rates to pay for America’s bills. Foreign investment in US equities alone, as a percentage of GDP has more than doubled from below 15 percent before the 2008 financial crisis to more than 35 percent today. Recently 10-year US treasuries spiked to their highest level in a year on fears that the central banks of China and Japan might scale back their Treasury purchases.

The keystone to US financial hegemony is the US dollar’s role as the world’s reserve currency, the source of America’s power. It allows America to print money with which to pay its bills, to control the international payments system (SWIFT) and impose sanctions. Nonetheless, America’s creditors have a vote on dollar interest rates, because America consumes much more than it produces and owes abroad much more than it owns. In a currency war, the avalanche of dollars could turn on a dime or a tweet. Two-thirds of the world’s assets are denominated in a debt-based fiat currency, issued by a country whose leaders are seen to be debasing that currency. The central banks of China and Russia have recently diversified their foreign reserves with this in mind, lessening their exposure particularly with America’s penchant to use sanctions to further its goals. Also America from time to time has threatened to block its financial rivals from using the SWIFT clearance system. China recently set up an alternative clearing system, no doubt hedging their bets. The US rejection of Jack Ma’s bid for US based money transfer MoneyGram International is the first of many volleys in the financial war for supremacy.

Bitcoin’s Popularity

Kings once had the unalienable privilege of coin issuance. Those who tampered with money were put to the death. Today with a computer, you can print your own tender, make a huge profit, and for some, achieve billionaire status. Certainly, times have changed. It is of no coincidence that the arrival of bitcoin is at the apex of distrust in fiat currencies. In fact, we believe it is the implicit debasement of legal tender today that has given rise to the crypto-makers.

Bitcoin’s volatile rise from zero to $20,000 and then $10,000 belie its role as a store of value. It hinges on cash flow to the owner and the only return is via a rise in price. Unlike gold, equities, bonds or even real estate, it has no intrinsic value. The real risk though is regulatory. To date, the Securities and Exchange Commission (SEC) have resisted the creation of crypto-ETFs notwithstanding that the CBOE and the CME are creating future contracts on bitcoin. In Canada, the OSC too has not approved ETFs, notwithstanding retail demand. We believe that a crack in the dam has already been detected since over-the-counter ETFs trade at a whopping 50 percent premium. Therein lies the crux of the matter. Regulators cannot protect investors from risk; they can only make them disclose. Obviously, there is risk but there would be even more if investors resort to the unregulated shadow markets. It would be better then for regulators to approve cyber-currency ETFs and other type products as long as the risks are disclosed.

Governments also view digital currencies as threats to their fiat currencies and policies. Ironically, we believe that the creation of synthetic ETFs and/or derivatives would allow the hedging of positions which would protect investors from these risks. Those derivatives then would likely prove to be the beginning of the end for crypto-currencies because only then, would there be sellers. To date crypto currencies have experienced buying demand but very little selling, until now.

Gold Still Rules

There are alternatives. Gold historically was a storm warning for global financial markets. When the seas were calm amid sunny optimism, gold was a non-performer. However, when economic or geopolitical tensions heated up, gold always garnered attention. Noteworthy is that gold has defied interest rate hikes and record market euphoria, rallying to its highest level since 2010, reversing a three-year downtrend. We believe, the jump in gold prices above $1,300 an ounce reflects both fears for the dollar and concerns about the consequences of rising public debt.

Gold was once an effective haven for capital inflows but today the stock market, bonds or even bitcoins serve as surrogate havens. That is to change. On the horizon is a beggar thy neighbour currency war, which America has already launched with the depreciating dollar. Ten years past the collapse of 2008, we believe currency devaluation is to be third and last desperate leg in the central banks’ economic arsenal, joining deficit spending and lax monetary policies. And amid the decline in American influence, geopolitical shifts of tectonic scale have occurred with elections looming in Italy, Germany’s Grand Coalition government and Brexit’s big hit will come from not the exit but the damage to the British economy as it leaves the EU and of course, there are the Middle East uncertainties. China and Russia too have stepped into the vacuum left by America’s newfound isolation taking full advantage of weakness in the West beset by protectionist agendas. Moreover, there is the threat of a trade crackdown. Slapping tariffs on your creditors would trigger a trade war and financial penalties. Gold will be a good thing to have.

In almost half a century, under a fiat system of floating paper currencies, America’s financial positon has deteriorated as debt rose causing a series of bubbles followed by busts. Before that, gold was a haven because the amount of credit creation was limited. Governments abandoned the gold standard in the seventies, replacing gold with a fiat currency, the US dollar. The greenback was a suitable replacement as the centre pin in American financial hegemony. However, a decade of man-made flood of dollars to avoid the Great Recession caused such a global glut of capital that cheapened the purchasing power of the dollar. We thus believe that investors will rethink the benefits in seeking refuge in dollar securities or crypto currencies created out of the thinnest of air. Amid the decline in American influence, its rivals are creating an alternate financial global architecture leaving the dollar’s orbit. All this suggest that times are a changing.

Gold is The New Global Currency

Like bitcoin, gold shares the distrust of fiat currencies but, unlike bitcoin, gold is accepted as the medium of exchange by all countries. Gold is an alternative to money, better than bitcoin because it retains intrinsic value. In addition, the total gold supply is limited at 180,000 tonnes while global money proxies are unlimited in size and scope. We believe that the fear of widespread currency debasement will provide the underpinnings for a $2,200 gold price with 18 months, particularly since the Chinese now control the physical gold markets.

Investors continue to ignore the largest bubble in economic history. We believe they would get better returns from gold than the interest bearing securities of the governments who run the printing presses. When the US dollar goes, interest rates will rise, bond prices and the market will collapse. Overvalued US treasuries will then give way to a financial tsunami. Gold is a hedge against the chance that the world’s central banks will prove no better at preventing high inflation than they were stopping another period of stock market exuberance. Gold is the final boat to rise. It is not so different this time.

Recommendations

Gold mining shares have been in a trading range despite a robust third quarter. Still, gold shares have lagged bullion but we believe that the significant underperformance of gold stocks is at an end.Expectations are for the fourth quarter to be much the same but margins have improved as cost cutting has more or less reached its limits. By-product metal prices also helped and some gold miners have begun unveiling exploration programs. Gold too has edged higher on a weaker US dollar.

First, the gold miners will benefit from a higher gold price and as it approaches $1400 an ounce, will spike higher. Gold technically has to fill a $200 gap and we can see spiking periods ahead which will cause a rush into better leveraged gold shares that have based for three years now.

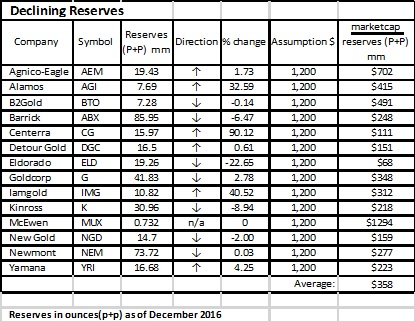

Second, we believe that the in-situ value of mines has not been reflected in stock prices averaging under $400 on a market cap per ounce of reserves basis. While not all ounces are alike, we believe that the gold miners’ major asset is in the ground. And while there has been a lack of exploration, the in-situ ounces in the ground are the cheapest in decades and will become more valuable particularly since there is a consolidation within the mining industry facing declining reserves. Agnico’s $163 million bid for the exploration assets of Canadian Malartic joint venture from Yamana is a reflection of the need to fill a pipeline of development projects. Exploration is the mining industry’s lifeblood and it could take three to ten years to develop with project economics at $1200 often in the low double digits. Third, low risk jurisdictions are increasingly important as it affects economics and the growing mood of nationalization makes ounces in the Americas trade at a premium.

We thus believe the gold miners are fundamentally undervalued. We continue to like senior Barrick Gold for its low market cap per ounce of in-situ reserves, quality mines together with an excellent management group. Agnico Eagle is favored for its growth pipeline as well as B2Gold, which has shown both execution and an excellent track record of growing ounces. Exploration vehicles such as McEwen Mining are favoured particularly for its most recent acquisition of the Black Fox assets, which will give it a third-leg and make McEwen a player in the prolific Timmins camp. We also like our recently financed Aurania Resources, a grassroots exploration play in Ecuador managed by Keith Barron, co-founder of Fruta Del Norte, the next big gold producer.

Agnico Eagle Mines Ltd.

Agnico Eagle continues its growth by acquiring the other half of the exploration assets of Canadian Malartic for $163 million which consists principally of the Hammond Reef project with a potential M&I resource of 5.4 million ounces at an average grade of 0.86g/t. Agnico Eagle recently raised their production guidance this year to exceed 1.6 million ounces with expectations that organic growth will top 2 million ounces in a couple years. Agnico Eagle has eight operating mines in Canada, Finland and Mexico and an enviable development pipeline including Amaruq open pit, which will take advantage of Meadowbank’s infrastructure in Nunavut by 2020. We continue to recommend Agnico Eagle.

Barrick Gold Corp.

Barrick Gold shares traded sideways despite reporting a solid third quarter at an all in sustaining cost of $772 per ounce, significantly below the $900 an ounce average of its peer group. Free cash flow in the fourth quarter was more than $400 million. In addition, Barrick will focus on four development projects, Laguna Norte, Turquoise Ridge, Gold Rush and Cortez Hills Deep South which will add more than one million ounces a year in 2020. Barrick's balance sheet continues to get better with $2 billion in cash and an undrawn $4 billion credit facility. Barrick and the Government of Tanzania are quietly negotiating an agreement to allow the operation of Acacia’s Tanzanian operations. Investors are hopeful that saner heads will prevail as Barrick is one of the major employers in Tanzania. Barrick's near term focus is on developing its 85 million ounces of in situ reserves and the focus on cash flow generation means that it will not be dependant on outsiders or another mountain of debt to finance these projects. Longer term, there are still ounces to come from Pascua-Lama and Alturas. We like the shares here.

B2Gold Corp.

B2Gold shares produced a record gold output of 630,000 ounces last year. B2Gold is a mid-tier player expected to produce about 935,000 ounces this year due to a full year’s contribution from long-life Fekola in Mali. Fekola is a company builder and was commissioned late last year to produce 400,000 ounces at a cash cost of only $350 an ounce. B2Gold’s Nicaraguan operations lagged but there are plans to boost those ounces. Fekola and Otjikoto are among the lowest cost producers contributing to a solid production profile. Masbate in the Philippines was a solid contributor and because of its fast growth profile, we expect B2Gold shares to get a rerating. Buy.

Eldorado Gold Corp.

Eldorado Gold shares are up from the lows on hopes that they have solved the metallurgical problems at its Kisladag Mine in Turkey. Metallurgical tests are continuing and the high-pressure grinding option while expensive, might work. Near-term negotiations continue with the Greek Ministry of Energy and Environment but there have not been any new developments. Eldorado's problem is that while they generate solid cash flow, its core assets face both political and operational challenges. The Greek operations with 22 million of in-situ resources are stymied and Turkey remains a problem as long as Kisladag metallurgical uncertainties go unaddressed. Eldorado shares are cheap and its balance sheet is solid but the shares are simply a hold here. The company will spend about $70 million in sustaining capital and $245 million in development but there is no near term cash flow from Skouries, Tocantinzinho, Certej, and Perama.

Kinross Gold Corp.

Kinross Gold’s eight mines generated $320 million of adjusted operating cash flow with solid contributions from Fort Knox, Tasiast, Kupol, Round Mountain and Bald Mountain in Nevada. Kinross’ Tasiast Phase 2 and Round Mountain Phase W feasibility studies clarified uncertainties and Kinross possesses better visibility of prospects down the road but larger capital needs are required. Construction at Tasiast and Round Mountain begin this year running down Kinross’ one billion dollar cash hoard and liquidity of $2.5 billion. We prefer B2Gold here.

McEwen Mining Inc.

McEwen Mining continues to build the Gold Bar project in Nevada which is to replace El Gallo Silver mine in Mexico as it transitions from oxide to sulphides. Gold Bar is to produce 65,000 ounces at a capex $60 million. Also, the company has acquired the Black Fox complex in Timmins for $35 million which will be critical when McEwen ships ore from Lexam’s Paymaster and Davidson-Tisdale to the Black Fox facilities which establishes a third leg. Black Fox had others spend a whopping $350 million on this 2,400 tpd producer including a tailing pond and $150 million of tax pools. At El Gallo in Mexico, a mobile crusher will extend that mine’s life. We like McEwen Mining down here with a solid balance sheet, no debt, rising production profile and large US following.

Newmont Mining Corp.

Newmont generated nearly $500 million in free cash flow, which was double the previous year’s quarter as this miner focused on margins. All in cost was $943 in the third quarter and Newmont produced 1.3 million ounces. Guidance was maintained. Last summer Newmont paid down its convertible notes improving its solid balance sheet. Newmont’s South America operations were affected by weather but Merian achieved record production in August. At Yanacocha, production guidance was maintained. About 70 percent of Newmont's production is located in the United States and Australia. Newmont has about nine projects which will add would 2 million ounces over the next five years, needed to improve a flat production profile. As such, we prefer Barrick here.

Yamana Gold Inc.

Yamana Gold is scraping the barrel and sold its half interest in Canadian Malartic exploration to Agnico Eagle for $163 billion as well as hedging 40 million lbs of copper production. Yamana is saddled with $1.7 billion of debt and cash flow is needed from its six mines, just to service its huge debt load. Yamana recently issued a senior $300 million note due in 2027 as it attempted to give itself breathing room. Cerro Moro in Argentina is on schedule and on budget and is expected to be in production this summer. Nonetheless, we prefer B2Gold here, which has a better balance sheet and growth prospects.

John R. Ing

More from Gold-Eagle