Gold Forecast: Leading Economic Indicators Support Impending Recession

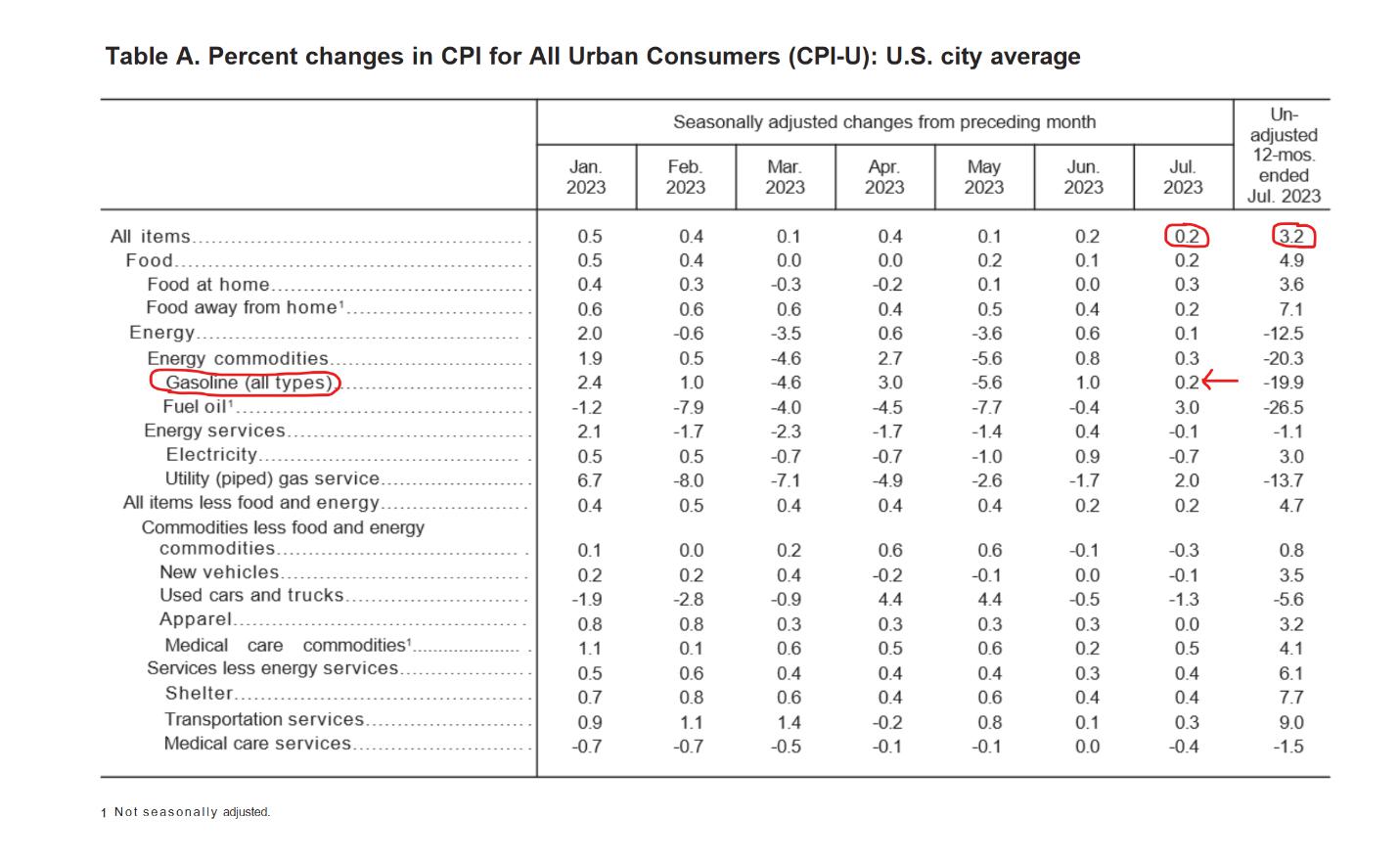

CPI came in within expectations at 0.2% for July and ticked higher to 3.2% year-over-year.

CPI came in within expectations at 0.2% for July and ticked higher to 3.2% year-over-year.

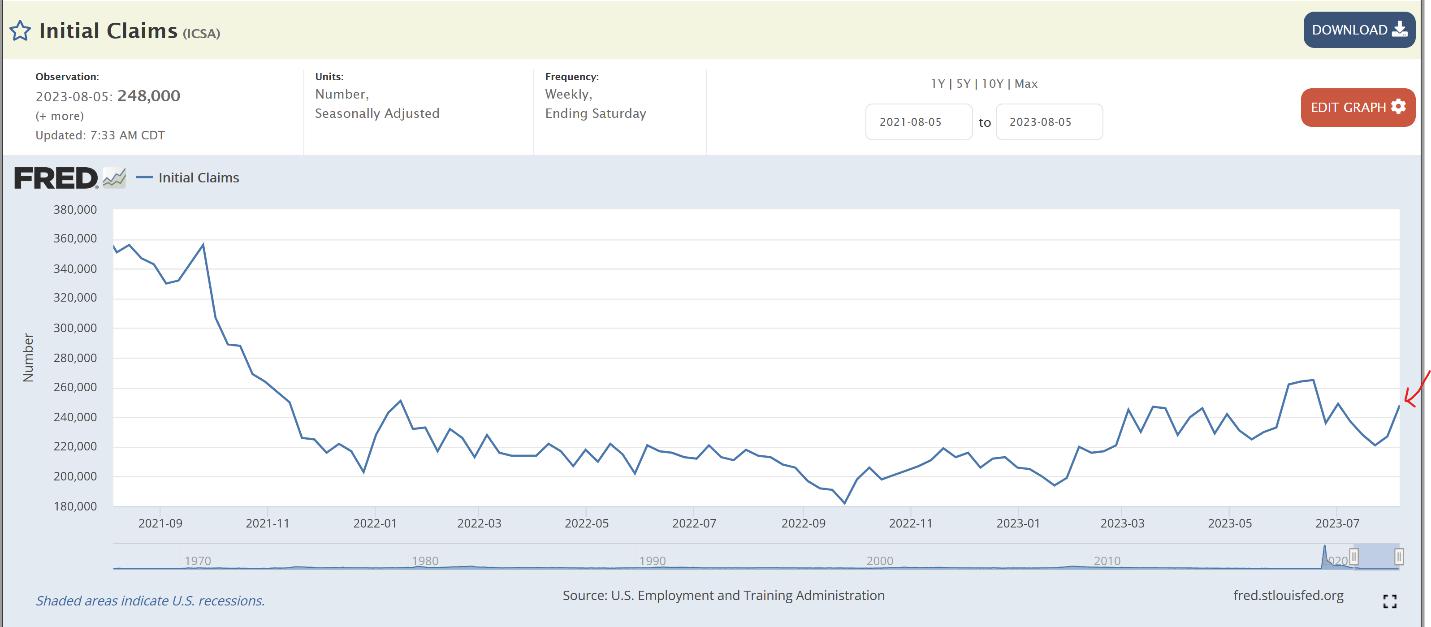

Initial jobless claims were higher than expected at 248,000 versus the anticipated 231,000.

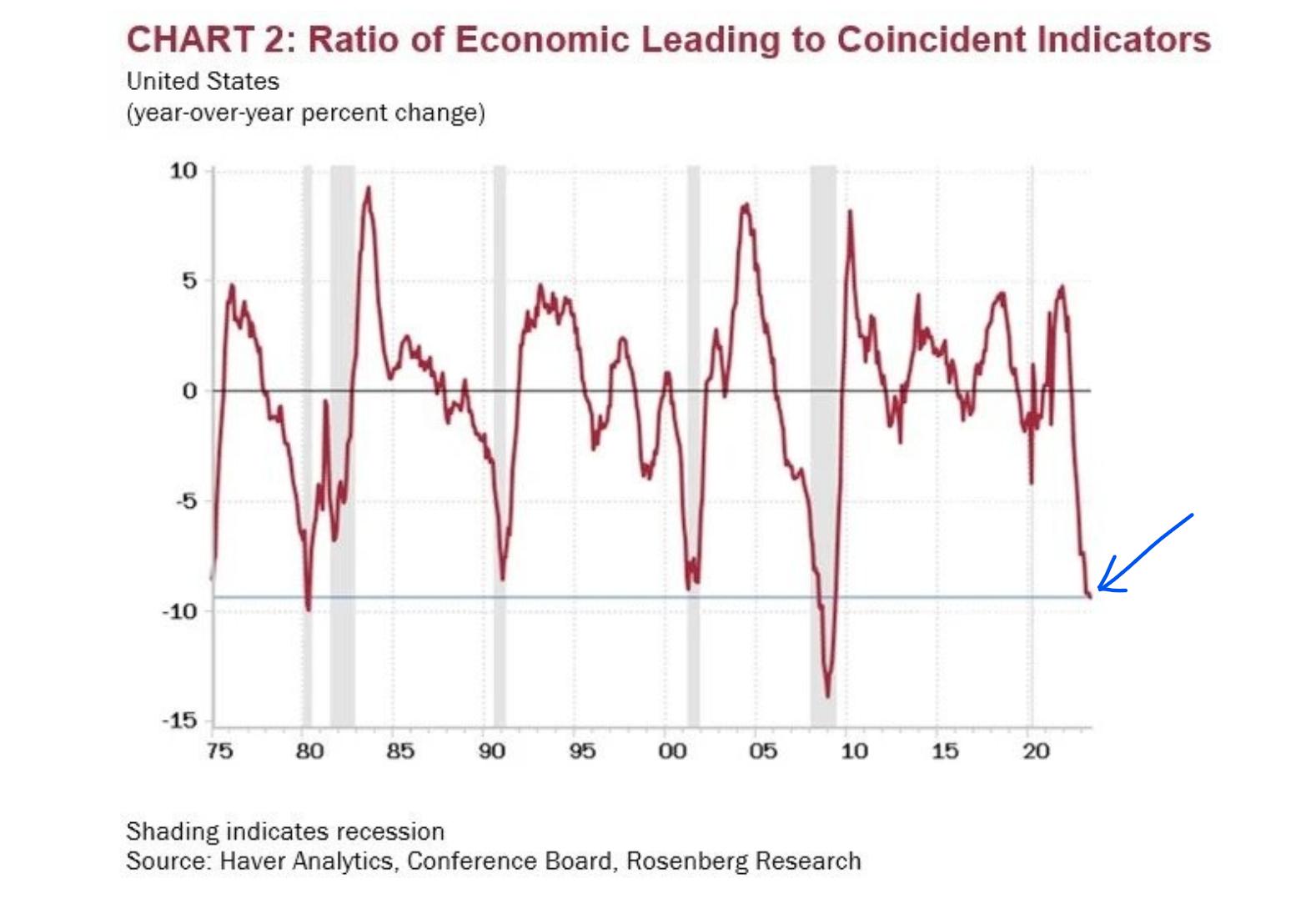

The current divergence between economic indicators supports a major turning point and impending recession.

Crude oil prices could shoot higher if Ukraine continues to target Russian transport vessels in the Black Sea.

CPI Update

I was surprised inflation was just 0.2% for July, given the 0.4% forecast predicted by the Cleveland Fed. Gasoline was up 0.2% for the month, which was lower than expected. I suspect energy prices could jump in August.

source: https://www.bls.gov/news.release/pdf/cpi.pdf

Initial Claims

Weekly jobless claims jumped to 248,000. This is a crucial data set I’ll be watching over the coming months. A breakout above the 265,000 high set in June would establish an uptrend and support a recession.

source: https://fred.stlouisfed.org/series/ICSA

Economic Indicator Divergence Signals Recession

In Q2, the coincident index was up +0.8% (annual rate), but we have a massive divergence with the leading index, which contracted by -9.3%. Deviations like this only happen at major economic turning points, according to David Rosenberg:

In Q4 2019, the coincident index was up +0.3% while the leading indicator contracted -3.3%.

In Q4 2007, the coincident index rose +0.6%, but the divergence was apparent as the leading indicator had collapsed -8%.

In Q4 2000, right ahead of that recession that nobody saw coming, the coincident index rose +0.6% while the LEI was down -7.6%.

In Q2 1990, the index of coincident indicators expanded by +2% but was invalidated by the -2% slide in the leading index.

In Q4 1979, just ahead of the back-to-back recessions, the coincident indicator expanded +0.6% when the LEI plunged -9.4%. That divergence was nearly identical to now.

In Q3 1973, the coincident index was up +2.6% but was not ratified by the -6.0% slump in the leading index.

Source: https://www.linkedin.com/pulse/im-turning-soft-david-rosenberg.

Ukraine Update

Over the weekend, a Ukrainian naval drone, loaded with almost 1000 lbs. of TNT, targeted a major Russian oil tanker, “the Sig.” Peter Zeihan suggests that these long-range maritime drones hold groundbreaking implications, presenting a risk to vital assets in the Black Sea.

The Black Sea is paramount for Russia’s maritime transport, exporting approximately 3 million barrels of crude oil daily and substantial volumes of ore and grains. Ukraine has issued a two-week notice for civilian ships to leave the area. After this period, any vessel entering or exiting Russian ports could become a target.

It remains unclear whether Ukraine can repeat its success, but if it does, Russia could lose its dominance, potentially disrupting 3 million barrels of daily oil production. August could mark a significant turning point, potentially triggering chaos across energy markets.

Commodity Update

GOLD- Gold continues to slip, and there is no telling when or where prices will stabilize. It all hinges on interest rates (see bottom panel). Worst case scenario, prices could revisit the $1830 area in September to complete a C-wave.

Note: During the third quarter of last year, 10-year Treasury yields surged from 2.6% to 4.0% pushing gold lower by $200. If the 10-year rallies to 5.0% (currently 4.0%), that could be the catalyst that takes gold down to the $1830 C-wave target.

SILVER- Silver is near-term oversold, and we are within striking distance of the June low. If prices break lower, my best guess for support is around $21.25.

PLATINUM- Platinum undercut the June low, but I’m unsure if that’s enough to trigger a bottom. Prices would have to close above $960 to support a low.

GDX- Miners are looking for support near the June lows, but at this point, I don’t think prices will hold. Ideal support comes in around $26.50 if prices break decisively lower.

WTIC- Oil is attempting to breakout above resistance around $83.50. Near-term prices are overbought.

Conclusion

The divergence between economic indicators is highly supportive of a recession. I have no idea when it starts, but I’m confident it’s coming.

Precious metals may languish into September, but once long-term yields peak, I expect a powerful wave III rally to new all-time highs.

*********

More from Gold-Eagle