Gold: How Many Zeros Are Enough?

With the pandemic disrupting lives and the global economy, government borrowings have climbed ever higher. US unemployment is nearly at Great Depression levels and a summer of civil unrest raises the stakes in an upcoming US election already lost in the wreckage of Covid-19 with more than 120,000 fatalities to date.

We believe the Covid-19 pandemic is the seminal event of our generation, which will have a massive global and geopolitical influence. True, despite nearing half a million deaths globally, many more lives will be lost, particularly in the US where incoherent measures, easing lockdowns, and the lack of leadership have resulted in the failure to contain or even suppress the virus. True, the virus respects no border, political stripes nor economic strata, yet governments have declared victory prematurely and reopened their economies, more for political reasons. Mr. Trump may be finished with the virus, but the virus is not finished with us. And true, in the post-pandemic world we’re not returning to where we were, it is to be the “never normal” instead.

United States of Infection

Indeed, history shows that these seminal events set off chain reactions, aftershocks and trends that we only see afterward. We believe that the pandemic’s aftershock will have economic, political, social, and military affects, particularly with the US – China relationship at historic lows. The economic policy response has been massive and global, uniting the world against a common foe with central banks throwing everything but the kitchen sink, including draconian lockdowns. The bailouts keep piling up, billons, trillions, there are not enough zeros. A trillion or two here and tens of trillions there. Significantly, the shock has disrupted global supply chains and trade, at a time when economic activity is now at its weakest since the Great Depression, exposing the interdependence of countries who are insourcing everything from ppe to cars to phones to semiconductor chips.

While the 2008-2009 financial crisis was mainly a financing problem in Wall Street, this time it is an economic problem with global casualties. The UN has calculated the pandemic has wiped out $8.5 trillion of global output, replaced by some $10 trillion of government bailouts. To be sure, the economic fallout from the coronavirus has raised the risk of sovereign defaults, particularly in those developing countries which lack the savings and institutions, which are now in terrible financial shape. Then there is the eurozone with its chronic debt problem between the northern and southern members made worse by Germany’s top court’s intransigence as it ruled that the ECB exceeded its mandate when it unleashed its bailout scheme, setting up a constitutional crisis in the European Union.

A worse thought though is the collapse in trust in America, recklessly deconstructing its own framework. In becoming the world’s largest debtor, after decades of cheap money, the United States has seen a collapse of trust in its economic and social make-up, exposing the country to fragmentation while its finances will be severely hit as the pandemic accelerates. The failings of capitalism, polarisation and racial inequality have robbed America’s moral standing. Ironically a new era of protest and a broad radicalised electorate appears to be fueling the force that could actually change the system. Nonetheless, despite the stock market’s rebound, retracing more than half of the coronavirus sell-off, harder times are ahead once the economic hardship from the pandemic materializes in the coming months or years.

Debt Trap

The pandemic has laid bare many unpleasant truths about the United States that we know exist but markets prefer to ignore. Too long America took for granted the longest economic expansion on record, financed by a large debt, denominated in a currency they can always print, ensuring they would never become insolvent. But now, the United States has weaponized this currency and despite its financial edge, its big spending today limits their options. The world faces a global recession, maybe worse than the Great Depression and although the world is much more interconnected, deglobalisation and the pandemic have weakened confidence in the United States and the dollar, just at a time when US exceptionalism has run its course.

In fighting the pandemic, the White House has put opening up the economy a priority, ahead of science and certainly guaranteeing a virulent second wave of Covid-19. But it is not only in the fight against the virus, but in the effort to resurrect the economy in time for the November elections, the White House has racked up record amounts of debt skewing the stimulus to households over businesses. It is politics at all costs, including the abrogation of long standing geopolitical relationships in favour of an “America First” policy. Trade wars and demonizing China, no doubt resonates in key electoral states, but drives a wedge between nations, ending decades of cooperation. This polarizing action is not dissimilar to the protectionist environment that worsened the Great Depression. Of concern is that the “beggar thy neighbour” mercantilism did not work then and won’t today.

Today, America’s isolation measures won’t help them when they need help with their finances. Sadly, it is politics that trumps all, which makes it the 1930s all over again. It is not so different this time.

For the past few decades, the United States built a consumption economy based on the service sector. Today consumer spending accounts for 70 percent of US economic growth. After the 2008-2009 financial crisis, the financial sector was given a boost as rounds of quantitative easing (QE), and near zero interest rates helped inflate asset prices and resurrect the economy, however the cuts also cut the returns on debt, which penalized savers as yields evaporated widening the wealth gap. And, as investors chased returns, property and the stock markets were the main beneficiaries of this easy money as Wall Street became easy street, bypassing Main Street.

America became the envy of many as everyone chased the American dream. But the dream was both elusive, non-inclusive and debt dominated. And soon, America began running larger fiscal and current account deficits financed by ever larger pools of foreign capital, much of it from Asia who had a surplus of savings, and of course dollars. There is no way to know how much debt is too much. The key is that the US can get away with a lot economically as long as it remained politically credible. Noteworthy, is that it took 6 years after the 2008 crash, for unemployment and the economy to get back to 2008 levels, in contrast to the Great Depression, which took 23 years. To be sure it won’t take a few months as the ostrich-like investors are hoping for. It might take years, maybe decades, a lost decade or even a lost generation. November will be very important.

Two Nations

Amid the divisiveness of the material, racial and political climate, Mr. Trump has resurrected his old scapegoat, demonizing China. After a drawn out trade war that left both countries weaker, the White House has escalated tensions between the US and China, beyond trading verbal blows over the pandemic, making technology markets a key source of friction. In an attempt to curb US ownership, Mr. Trump ordered the government’s pension fund to no longer invest in index funds, which included Chinese companies. And in a further move that raised the stakes in this new Cold War, the White House threatened to revoke Hong Kong’s special status.

And in this financial war, currency is to be the next pawn and as China’s renminbi has fallen against the greenback, unwittingly producing another advantage for China, particularly at a time when both sides earlier pledged to avoid competitive devaluations. Yet, in weaponizing the dollar, Trump makes it easier for the world’s second largest economy to export its way out of the Covid-19 slump, something the Americans can’t and need. China too has turned inward, becoming a massive consumer to its demographic weight of 1.4 billion people, rather than just a producer with export-led growth. Will American multinational giants in a tit-for-tat move be blocked from the world’s largest market?

With little trust between the two, President Trump’s actions of decoupling from China and ending decades of mutual dependence, risks backfiring as the ratcheting up of hostilities emboldens China’s leadership. For example, rather than an earlier cooperative relationship, China instead called Trump’s bluff, throwing down the gauntlet with the national security law on Hong Kong. The trade deficit with China has grown even wider as US exports collapsed, but Chinese imports rebounded reflecting the desynchronisation with the world still mired in a health crisis. And not surprisingly the Phase 1 trade deal is stillborn and part of a long list of contention. Of deepening concern is that Beijing is also threatening to “weaponize” its position as the world’s largest creditor and the global hegemon has chipped away at America’s financial hegemon status. America’s game of chicken could hurt both sides.

A further example is China flexing its financial muscles, paring its huge $1.3 trillion dollar holding of US debt of a total $3.1 trillion of foreign exchange reserves and abstaining from recent treasury auctions. Both China and Russia have converted some of their vast dollar holdings into gold in a diversification move. China is also creating a digital version of the renminbi which could internationalize the currency and Chinese banks’ total assets now rival those of American and European banks, financing champions Alibaba, Meituan and Tencent (ATM). This group is among the world’s giants, having set up digital wallets rivaling, bypassing and competing with America’s big banks. China’s vast investment and trade network is its backbone and helps internationalize the renminbi, aiding the “Belt and Road” initiative modeled after America’s “Marshall Plan”. China also suspended debt repayments for 77 developing countries using its soft financial power, enhancing its reputation and boosting its global standing.

China plans a “Big Bang” to give impetus to its financial markets, opening its markets and access to the mammoth $131 trillion bond market that is twice the world’s GDP. The US Senate passed a bill that may blackball Chinese listings but already direct Chinese investment has fallen from $45 billion in 2016 to a paltry $3 billion, at a time when both countries need investment. Chinese companies listed on foreign exchanges have a global market cap of almost $2 trillion and almost all will list on Hong Kong, one of the world’s leading exchanges. Both countries are losers. At the same time, the Hong Kong Stock Exchange will offer futures and options on 37 of MSCI’s equity indices, cementing Hong Kong as a major financial centre despite the current brouhaha. Hong Kong is one of the world’s largest equity market and home to 420 hedge funds.

The Thucydides Trap

Of importance is that Covid-19 portends change. The status quo before the pandemic won’t return as the “never normal” reshapes our institutions, political systems, and globalism itself. For the latter part of this century, America has been ascending and dominant as the world’s leading nation. But today the pandemic will most likely change the world order and ensure that the balance of the century is likely to be an Asian one, as the late 20th century was an American one. Ironically, it is America’s destruction of its own institutions, abrogation of agreements as part of the “America First” polarization and response to the virus that jeopardizes its primacy. It will be remembered as a turning point. History will show that it was not that the Chinese sent face masks or airlifted ventilators, or the virus, but that they had the savings and financial wherewithal to step into the vacuum left from an isolated America.

Amid the escalation of tensions between Beijing and Washington, nations are left to choose between the US and China. For example, Mike Pompeo, US Secretary of State recently chastised ally Australia for choosing to join China’s Belt and Road programme aimed at building infrastructure across Asia, and so threatened to push Australia out of the US “Five Eyes” intelligence sharing partnership. Canada too, the United States’ closest ally was also threatened of being ousted. Left unsaid, what would happen if America’s traditional allies opted to support the Chinese and not the US? Or in the race for a vaccine, what would happen if the Chinese discovers one or two vaccines?

For some time we have noted that the new cold war between the two superpowers has uncanny similarities to earlier periods when rivalries between established and rising powers eventually led to war. In fact, Professor G.T. Allison of Harvard observed that in the Thucydides Trap, over the past 500 years of history, when a rising power threatened to replace the established power, that in 12 of the 16 cases, the end result was war. Only in four of those cases, there was no war. We believe that the Covid-19 pandemic has changed the world and that in the “never normal” world, countries are facing inward for self-sufficiency and that the virus not only changes trends, but accelerates them. Of concern, is what little there is between them, can these two superpowers escape the Thucydides Trap?

Chicken in Every Pot

Herein lies the problem. To avoid a depression, central banks have stepped into the breach and backstopped their respective economies in a “chicken in every pot” promise, ironically used in Hoover’s 1928 presidential campaign. Central banks have and proposed to buy government bonds and corporate shares on an unprecedented scale, using their balance sheets as they did in the financial crisis in 2008-2009, but this time the global economy is on life support.

The Fed again has led the way, with the fiscal bazookas of four and now five rounds of quantitative easing (QE – to infinity). The Fed also pledged to purchase investment grade corporate bonds as part of their support of the debt markets, again using its balance sheet but now the portfolio holds bankrupt Hertz bonds. Britain, Japan and eurozone countries soon followed, pledging to buy $6 trillion plus worth of assets between them. The Fed has even backstopped the commercial paper market, further distorting the market by pushing borrowers into longer dated paper, creating a vacuum and funding problem.

While the big spending measures are viewed as temporary, governments are running history’s biggest budgetary deficits as they hand out checks to their citizens and businesses. Fiscal and monetary policy has become one. Yet in becoming an instrument of the government, turning debt and borrowings into money, the Fed’s mammoth money creation is not dissimilar to what has happened in many Latin American countries, Zimbabwe or Weimar Germany.

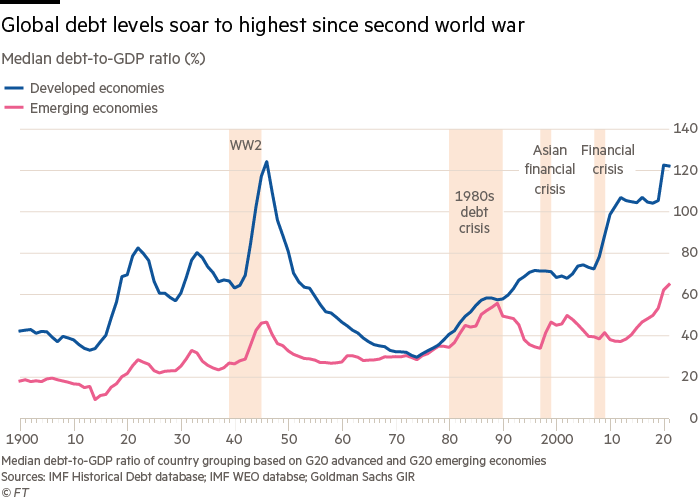

On the face of it, there is almost $3 trillion in stimulus to support the US economy on top of the $4.7 trillion of budgetary spending announced before the pandemic hit. Because some of the stimulus programmes has been spent, the Democratic-led House passed an additional round of up to $3.5 trillion of stimulus spending for a total spend of almost $10 trillion or 50 percent of GDP, rivaling the government expenditures at the height of World War II. Soon this massive supply of debt will dwarf asset purchases. Debt has become so cheap that issuances have swamped central bank intentions with debt levels over 130 percent of GDP according to the IMF, far above the crisis levels of 2008. Already the taxpayer through their central banks will be on the hook in purchasing up to a third of the debt to fill the vacuum left without the traditional check writers like China. Someone is to discover that money does not grow on trees.

Ponzi Scheme

And, few care because we are told the US dollar is deep in liquidity and after all, is the world’s dominant reserve currency mandated in the Bretton Woods Agreement in 1944 that pegged the dollar to gold. When the dollar became the bedrock of the world’s financial system, the rest of the world followed, fixing their currencies to the dollar. However all good things must past, and after two decades of excess money printing to pay for the Vietnam War and the “Just Society”, the system fell apart and the United States was forced to sever the gold linkage in 1971, devaluing the dollar to give the economy a boost. Of course, inflation soon followed with Paul Volcker stopping the slide into hyperinflation. Since then, the Fed has become the ring master and without the discipline of gold, the Fed printed more cheap dollars funding Japan, Germany and China who recycled their excess dollars in a quid pro quo move into America’s debt securities.

Simply put, America’s prosperity and profligacy was financed by the world in a Ponzi scheme, of borrowing dollars to close their financing gap, financing the purchases with newly minted dollars. The plan was almost too perfect. When foreigners finally balked at financing America’s spendthrift ways, the Fed simply replaced those foreign dollars with dollars printed from its balance sheet. However, the Trump presidency has taken America to a place it has never been. Since 2007 (before the last crisis) the Fed’s balance sheet has exploded from $800 billion to almost $7 trillion, and over the next 18 months is expected to top a whopping $12 trillion or almost 50 percent of America’s GDP, double the 2008 financial crisis. America’s debt at $26 trillion is the largest in the world.

Hostage to the Printing Press

Those days are over. Therein lies the weakness or Achilles heel of America’s financial hegemony. Until the last decade, America was content to use the dollar and its financial markets as the world’s ecosystem to promote trade, prosperity, influence and to finance shortfalls. America and the world prospered. But in the aftermath of 9/11, America chose to weaponize its influence, sometimes imposing sanctions, sometimes blocking others from dollars and sometimes threatening to change the world order. And despite a shrinking share of the world’s gross domestic product, the dollar’s supremacy depended more upon America’s economic and military might, as well as the strength of its institutions and agreements. But it is the abuse of this strength that the Trump administration has undermined the dollar’s status as the dominant global reserve currency. The mismatch changed when America took advantage of its financial powers, to impose sanctions on Russia, Iran, Iraq, and Venezuela or started trade wars with allies and restricted countries from the American dominated SWIFT payment system.

America is isolated. America is mired in a health crisis, economic and political crisis. Lacking in savings, the United States is heavily dependent upon foreign flows of capital to finance its massive deficits particularly given the government’s huge financing needs. A reduction in foreign flows has forced the Fed to fill the shortfalls with newly printed dollars, resulting in a recent steady deterioration in the dollar which is at its lowest since January.

And while America flexed its financial muscles, others such as China, Russia and the Middle East players have started to build alternate payment systems, even replacing SWIFT, the global payment system supported by America. Then with the collapse in oil and the fraying of ties with ally Saudi Arabia, oil once priced in dollars is now priced in renminbi, roubles and yen. It seems in the post pandemic era, the world is entering a post-dollar era as the markets balk at financing a nation that spends twice as much as they bring in, and tells the world they don’t need them. It is not so different this time. To hedge against the deterioration of the world’s reserve currency, investors instead have migrated to other hard assets, like gold.

Inflation is Back

Central banks have relegated inflation as a relic of the past. Simply put, inflation is the consequence of too much money chasing too few goods. All this leads to our belief that once the lockdowns ease and, thanks to the unprecedented boost in fiscal and monetary measures and the decimation of the supply side, the pandemic will lead to double-digit inflation. Trump’s trade wars also brought forward deglobalisation, which has already increased costs, yet another inflationary input. And in the “never normal” climate to come, there will also be upward pressure to increase the value of former poorly paid “front line” labour, leading of course to more inflation. Ironically, lawmakers after providing unemployment benefits of $2.2 trillion to 40 million plus out of work Americans, almost two-thirds of the recipients made more money than they were making before the crisis. As a result, lawmakers are considering a bonus to lure those workers back. To be sure, the costs of stemming the widespread unemployment are high but the major problem is how to wean the US economy and its workers off the support measures who have become addicted to the largesse. Reopening will also have high costs with yet another spending blowout likely, even before the upcoming electoral chaos of November.

Because of America’s exploding deficits and the lack of foreign funding, the Fed keeps finding new and improved ways to print dollars. Quantitative easing allowed the bank to purchase vast quantities of government and corporate debt with money borrowed or printed. Then taking a page from the Democrats, adopted Modern Monetary Theory (MMT) which conveniently allowed the Fed to print money with impunity providing unlimited funding, under the guise that the consequential economic recovery will pay for the stimulus package – a sort of reworked supply side argument. Like other radical experiments, quantitative easing, supply side and now MMT, no one speaks of the cost, only the rationale. The cost? Higher inflation, more debt and a debased currency. The dollar days are doomed.

And most likely, since inflation is one of the few and easy ways for governments to cut the public debt burden, we expect a new age of “austerity”, increased taxation on taxpayers, yet another inflationary input. Finally in the never normal climate, the American people will elect an inflationary president and Congress in November, as there is no appetite for austerity and more hardship. That will be good for gold, but bad for the dollar.

Gold Is an Alternative to Money

The current administration views the Covid-19 pandemic through rose coloured glasses, as it eases the lockdown, while the virus deaths continue to spike. Similarly then, investors’ rose coloured lenses see an economic recovery whilst half the population is unemployed. And, despite record amounts of debt, the government believes they can always spend more. These rose coloured views are wrong. Politics are at play and thus the rosy outlook.

Most important, it is wrong to dismiss the pile of debt and that the savings, which lent to governments, companies and now handed to households will remain intact. The surge in debt that drove rates down, fuelled a stock market boom and widened the wealth gap, has left taxpayers and households paying interest on a debt that keeps piling up, while the government prints its obligations away. This cannot last. A collapse in the dollar, stock market and bond market is the new reality. It doesn’t take rose coloured glasses to show that gold is a barometer of investor anxiety – it will be a good thing to have. Gold’s rally is built on fear.

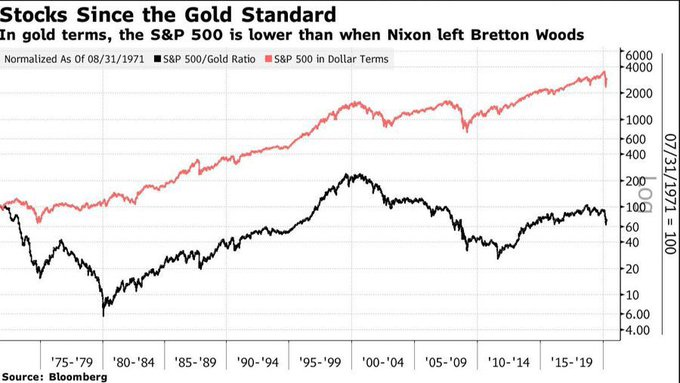

We believe that the steady erosion in the value of the dollar and gold’s uptick is a sign that the market is worried that the Fed has lost control in its ability to manage the nation’s needs. Gold is priced in dollars and recently hit an eight year high. The rise in gold can be seen as a devaluation of the dollar. Gold has also posted record highs in other currencies. Since year end, gold has risen almost 13 percent in terms of dollars outpacing stock markets. That revaluation has further to go. Central banks led by Russia and China have been a big buyer of gold. Global broad money supply (M3) or stock of money has soared to an estimated $90.4 trillion and that is before the recent massive stimulus programmes.

The US has a serious problem with its deficits and overvalued dollar. If they continue to print money, whether by economic stimulus or to stave off corporate bailouts, the fear of currency debasement and consequential inflation will undermine the dollar. The Fed remains the largest holder of gold. If gold is a finite currency, its value not just against the dollar, but euros and yen too should rise in value. The total gold supply is some 170,000 metric tonnes. Scaling the money supply today and deflating by the gold supply, the price of gold would be in excess of $15,000 an ounce. We are not so optimistic but continue to view $2,200 an ounce as a reasonable near term target.

And there are technical reasons for gold posting new highs. The gap between the physical and future markets is closing as the bullion banks, such as HSBC and Scotia Mocatta have exited the market, after taking millions of losses. The bullion banks were often on the “short” side of the market and instrumental in capping the physical market with an onslaught of futures contracts on the Comex, the futures exchange. Their net short positions to hedge positions in London blew up when Swiss refineries closed down because of Covid-19 and at the same time there was a surge in physical gold demand, which caused a spike in the gold price. Bullion bank players, HSBC took a $200 million loss and Scotia Mocatta started in 1684 closed down with a $160 million writedown by Bank of Nova Scotia. At last, the physical market without the future overhang saw a pickup in demand as the Shanghai Gold Exchange, now the largest physical player in the world saw record demand. Covid-19 has unwittingly disrupted the supply chain of the market and today there is a solid underpinning to the market. This bull market has just begun.

Recommendation

The Covid-19 pandemic triggered closures of mining operations but much of the protocols were temporary. In the uncertainty, the major producers also drew down their credit lines producing balance sheet flexibility. Others like Lundin Gold, Osisko Mining and Great Bear issued equity to shore up their balance sheets. As the panic subsided, the majority have reopened their mines and changed guidance but the impact won’t be seen until the second quarter numbers. The first quarter numbers were good due to the higher gold prices and most recorded free cash flow and stronger balance sheets.

Deal making was light as miners focused on their operations. The Chinese were the exception with Shandong buying distressed TMAC and Zijin buying Guyana Goldfields, who were plagued with start-up problems. However, while gold prices flirted with $1,700 an ounce close to an eight year high, more consolidation is expected as producers focus on reserve replacement. It is cheaper to buy ounces on Bay Street than to explore. The mid-tier players are also expected to bulk up, feasting on the non-core assets of the bigger miners. Exploration spending has yet to edge up but we expect a pickup driven by the need to boost reserves.

Among the seniors we like Barrick Gold and Agnico Eagle for their excellent management, healthy reserves and balance sheets. We also like B2Gold and Lundin Gold for a rising production and reserve profile. Potential takeover targets are Centamin and Eldorado. Junior developers like McEwen Mining are favoured.

Agnico-Eagle Mines Ltd.

Agnico had a decent quarter generating free cash flow. Agnico lowered their capex from $740 million to $690 million, and drew down a $1 billion revolver as a precautionary move, likely to be paid off as they ramp up production. Nunavut is its key strategic platform with Meliadine and Amuruq joining Meadowbank. Flagship LaRonde keeps on giving, with the West area having potential at depth and the expansion at LZ5 (zone 5) paying off. At Kittila in Finland, the mine expansion was delayed because of Covid-19, but operations in the midterm could continue at 2,000,000 tonnes per year rate. The four year expansion could boost ounces by 60,000 annually. We like the shares here.

B2Gold Corp

B2Gold generated free cash flow and retained annual production guidance of 1,000,000 ounces at AISC of $800 an ounce. B2 Gold is virtually debt-free with $200 million of cash. Flagship Fekola mill expansion is on track and to be completed later this year. The sale of the Nicaraguan mines lowered B2Gold’s cost profile. Hedges on fuel resulted in a book loss, Fekola’s AISC was $519 an ounce, Masbate $908 an ounce and Otjikoto $850 an ounce in the first quarter. We like B2Gold`s production profile here.

Barrick Gold Corporation

Barrick had a solid quarter, continuing its string of successes. Barrick produced 1.22 million ounces in the quarter with a solid contribution from Nevada Gold Mines, Barrick`s sixth Tier One mine. Barrick also resumed exports from the long idled Tanzanian operations after the protracted government settlement negotiated by Barrick. With that stalemate settled, a new one surfaced as the Papua New Guinea (PNG) government threatened not to renew the joint venture license in a shakedown move so popular today. Consequently the mine was shutdown and the playbook of protracted negotiations will begin. Nonetheless, Barrick’s other operations are fine with Nevada on track and the Latin American operations much better. Key for Barrick is a now rock solid balance sheet and cash flow generation. From a peak at $12 billion, net debt has been slashed to less than $2 billion with cash and equivalents at $3.3 billion and a $3 billion undrawn credit facility. With quality core mines in Nevada, Africa and Latin America, excellent management and huge cash generating capability, Barrick is a buy here.

Centerra Gold Inc.

Centerra generated free cash flow of $77 million from the Kumtor mine in Kyrgyz Republic, Mt Milligan in British Columbia and from the Öksüt Mine in Turkey which just came on stream producing almost 5,000 ounces. Centerra plans to spend $32 million on brownfield projects and Öksüt is about 95 percent complete. A new life of mine 43-101 is expected in the second half at Kumtor, which should boost reserves over the midterm. At current levels, we prefer more growth oriented B2Gold with a safer geographic risk profile.

Eldorado Gold Corp.

Eldorado maintained guidance of 520,000 – 550,000 ounces at an AISC between $850-$950 an ounce despite a temporary Covid-19 closure. Eldorado ended the quarter with $400 million of liquidity against total debt of $635 million. At Efemcukuru in Turkey, production was lower due to grade. At Olympias in Greece, the mine had the highest output in 18 months but costs remain a problem. At Lamaque in Québec, operations were restarted but grade was lower. Eldorado plans to mine the Triangle deposit, building a decline to be processed at the Sigma mill, to be completed in 2022. Nonetheless, Eldorado is a mid-tier player in need of some good news from Greece which is either its potential future or an albatross. At current levels, the shares are a hold as the Greek assets are not reflected in Eldorado’s share price. Hold.

IAMGold Corp

New CEO, Gordon Stothart reported a so-so quarter with improved output from Rosebel in Suriname, but lower output from Essakane operations. However, production was down slightly and costs were up. Westwood was put on care and maintenance though in need of a redesign. Guidance was lowered slightly to 685,000 – 740,000 ounces this year at AISC between $1,195-1,245 per ounces, one of the highest among its peers. While IAMGold talks up its healthy reserves at 16.7 million ounces, this is due more to inclusion of Côté Lake, the off and now on again project. The company is to spend $45 million on engineering but details and capex are missing. We are skeptical that this project will ever get into production because of grade, costs and continuity questions. Nonetheless, IAMGold has a stellar balance sheet with $829 million in liquidity against $419 million of senior debt but with an ill-advised $170 million forward gold sale (Côté Lake). Many Chinese companies have kicked the tires but passed because of their asset and cost profile. We agree. Sell.

Kinross Gold Corporation

Kinross` three core mines, Paracatu in Brazil, Kupol-Dvoinoye in Russia and Tasiast in West Africa had a good quarter, generating $110 million of free cash flow from 567,000 gold equivalent ounces. At Tasiast, labour problems surfaced and despite a three year labour agreement negotiated last year, the walkout will hurt output. Although Kinross is continuing with the Tasiast expansion with contractors and an agreement with the government is a go, Kinross had to double the royalty payments. Nonetheless, capex was reduced slightly and their balance sheet is good. However, Kinross’ exposure to Russia and Tasiast in Mauritania ensures that the political risk is higher than its peers. As such, we prefer B2Gold here.

Kirkland Lake Gold Ltd.

Kirkland had an excellent quarter producing 330,000 ounces at AISC of $770 an ounce. Importantly they generated about $190 million of free cash flow, allowing them to end the quarter with $530 million of cash and no debt. Kirkland`s purchase of Detour was timely producing 92,000 ounces at AISC of $1,108 an ounce, offset by stellar high grade Fosterville in Australia which produced gold at only $313 an ounce AISC. The key was that Kirkland was able to buy Detour with paper, extend its short reserve life by almost 5 times while generating huge cash flow. Kirkland’s other core asset, Macassa performed well and the shaft expansion was resumed in April. Kirkland has wisely allocated the Holt complex, Cosmo and Union in Australia as non-core assets, focussing on its three core mines. We like Kirkland here.

Lundin Gold Inc.

Lundin Gold is in the midst of developing Fruta del Norte (FDN) in Ecuador, the richest gold mine in the world. Although commissioned in February, Covid-19 caused a work stoppage. Annually Lundin will produce 350,000 ounces at AISC under $800 an ounce. Newcrest of Australia recently upped its stake in Lundin, and we believe that the Lundin family will harvest their stake in opportunistic fashion. As such with both production and reserve upside, and with little downside risk (FDN almost fully built), the shares are an attractive buy for the eventual takeout.

New Gold Inc

New Gold is one of the few gold miners that can lose money at today’s prices. Cash costs in the quarter increased due to lower grades (again) and higher capex spending. New Gold produced 103,000 gold equivalent ounces from Rainy River and New Afton. Part of the reason for higher costs is New Gold’s habit of reporting gold equivalency (gold/copper), which in our view the ratios can be misleading. Rainy River still doesn’t work and is mostly copper, New Afton reported more dilution. Blackwater in British Columbia was sold for $190 million cash or $20 an ounce allowing New Gold to monetize a capital intensive project. The company has again lowered guidance. Costs were higher. Still, this did not bother the Ontario Teachers’ Pension Plan which invested $300 million in a strategic partnership, allowing New Gold freedom to refinance its heavy debt load at $750 million. While we do not share OTPP’s optimism and would not pour good money after bad money for a mine that can’t make money at today’s prices, the shares are an option on higher gold prices and we believe that this miner is being dressed up for sale likely to a major looking for cheap ounces. Hold.

Newmont Corporation

The world’s largest gold producer reported a strong quarter producing almost 1.5 million ounces generating $611 million of free cash flow. Guidance still stands at 6 million ounces of gold per year and Newmont ended the quarter with total liquidity of $6.6 billion, including $3.7 billion of cash and an undrawn $3 billion credit facility. Newmont also completed about 80 percent of its $1 billion share buyback to offset the Goldcorp acquisition. With 12 operating mines, Newmont is focusing on turning around Goldcorp’s problem assets, including Eleonore, Cerro Negro and Musselwhite. Newmont will spend about $1.4 billion, delaying the Tanami 2 expansion project. We believe that while Newmont is a cash machine, they still have their hands full digesting the Goldcorp assets. In the interim, we prefer Barrick here.

John R. Ing

Please refer to the Legal Section of our website (maisonplacements.com) for our Research Disclosures for an explanation of our rating structure at https://maisonplacements.com/research-reports.

*********