In Gold We Trust

Since the narrowly averted implosion of the financial system in the fall of 2008, we are now in the 7th year of global monetary policy experimentation. Although the Federal Reserve stopped its “quantitative easing” program last year, other central banks are now stepping into the breach. On a global level, central banks will create more irredeemable money this year than ever before.

Balance sheets of major central banks in percent of GDP

Sources: Bloomberg, Federal Reserve St. Louis, SNB, Incrementum AG

With the introduction of negative interest rates in what are supposedly hard currency areas, monetary policy has set yet another, hitherto unthinkable record. This attack on the cultural heritage of money, which is justified with the goal of creating greater general prosperity, is clearly in conflict with any sort of economic common sense. These policies are thus also contrary to our fundamental economic convictions, which are rooted in the Austrian School of Economics.

The promised self-sustaining recovery by means of magical monetary policy elixirs is again conspicuously absent this year - the situation is increasingly reminiscent of the comedy “Groundhog Day”. It is noteworthy that the annual déjà-vu in terms of growth disappointments hasn't yet resulted in market participants recognizing that the nature of the crisis isn't cyclical, but systemic.

It is therefore all the more astonishing that the loose monetary policy that has been practiced for seven years running now, is being copied everywhere. This is a case of a theory attracting all the more support the less it is able to withstand empirical testing. Thus economic output in the US declined by 0.7% in the first quarter vs. the same quarter of the previous year. As can be seen in the following chart, growth expectations continue to disappoint.

Gradually decreasing growth expectations

Sources: Bloomberg.com, Federal Reserve, Incrementum AG

Regular readers of this gold report, which has been published for the past nine years, already know that we believe that the examination of the current monetary system is central to any profound analysis of the gold market. In recent issues, we have in this context extensively discussed the struggle between deflationary and inflationary forces. This conflict, which we have dubbed “monetary tectonics”, is very important for investors.

In said struggle, disinflationary forces have clearly had the upper hand since 2011. In the past 12 months, we were able to observe a textbook example of systemic instability – i.e., of monetary tectonics in action. The price of crude oil declined by more than half within just seven months. Many analysts have attributed this solely to underlying supply and demand factors, which is in our opinion a deficient explanation. All industrial commodities, as well as every paper currency, have lost enormous ground against the US dollar over the same time period. In our current dollar-centric monetary system, this concurrent devaluation of all commodities is a disinflationary earthquake.

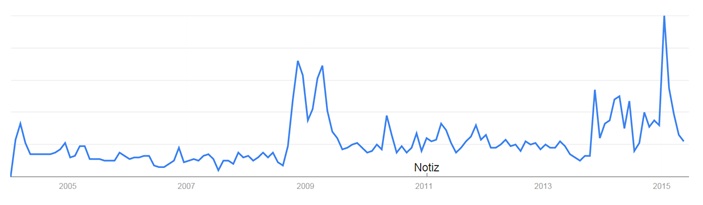

As a consequence, the trend of slowing price inflation rates accelerated further and culminated in a bout of scaremongering propaganda in the media about the allegedly acute threat of falling consumer prices. Even in Germany, traditionally a stronghold of inflation concerns, a never before seen fear of deflation began to spread in early 2015. This successfully paved the way for a quantitative easing experiment amounting to EUR 1.14 trillion. As can be seen on the chart below, Germany-wide searches for the term “deflation” exceeded even the peak recorded in 2008.

Google trends: Germany-wide searches for the term “deflation”

Source: www.google.de

In our last report, we wrote: “Should the inflation trend reverse, excellent opportunities in inflation-sensitive investments such as gold and gold stocks will emerge.” Since then, the gold price has been able to hold up quite well despite the disinflationary tsunami; other inflation-sensitive assets – as was to be expected in such an environment – were sold heavily. From today's perspective, the portents for a turning point in the inflation trend have changed dramatically, inter alia because commodities are trading at much lower price levels in the meantime and base effects will affect price inflation rates even if commodity prices should stagnate.

Considering how recent the monetary near-death experience of 2008 is, it is astonishing how quickly a “this time it's different” mentality has returned. Since much of the speculation in the gold sector has evaporated in recent years – which can be seen in the large decline in ETF holdings – it now appears as though practically all market participants have lost faith in gold. Similar to how many a bon vivant on his deathbed – this is to say, at that moment when his familiar world threatens to be obliterated – seeks his last refuge in God, a great many people became devoted disciples of gold during the last financial crisis, when the threat of systemic collapse loomed.

Since this danger seems to have been averted for the time being due to the life-supporting measures taken by central banks, gold is no longer seen as a necessity by these “disciples in extremity”. In this environment, a positive assessment of gold strikes many market participants as anachronistic, almost pitiable.

Total ETF volume (in millions of ounces) vs. gold price

Sources: Bloomberg, Incrementum AG

The declining interest in gold is also reflected in the strong reduction of gold price volatility. The current market phase reminds us of a German saying that could be loosely translated as “tranquillity breeds strength” which is also applicable to financial markets. Times of tranquillity are times in which strength is gathered prior to the emergence of a strong trend. Even though we did not expect such a long-lasting corrective phase, we definitely do not share the opinion of many analysts that a new secular gold bear market has begun in 2011.

What is the reason for our unbroken confidence in gold? Our predilection for gold is primarily based on our understanding of monetary history. At the moment, it appears as though faith in the omnipotence and infallibility of central banks is at an all-time high. This goes hand in hand with new record highs in stocks and especially government bonds. According to Jim Grant, who describes the price of gold as reciprocal of the credibility of central banks, this is inter alia a likely explanation for the somewhat directionless performance of the yellow metal. Should the omnipotence of central banks be questioned by the markets, it could cause a fundamental change in perceptions and help gold regain its former respect and reach new heights.

In addition, our analysis is reinforced by a comparison of the current situation with that of the last great bull market of the 1970s and how it ended. There is a fundamental difference: back then, the Fed tried to end the trend of rising price inflation with restrictive monetary policy, today central bankers around the world are trying their best to create accelerating price inflation. The stronger the systemic desire for rising prices becomes, the more creative and radical the actions of policymakers become in order to attain this goal.

“I do not hesitate to say that although the prices of many products of the farm have gone up […], I am not satisfied. It is definitely a part of our policy to increase the rise and to extend it to those products that have as yet felt no benefit. If we cannot do this one way, we will do it another. But do it we will.”

US president Franklin D. Roosevelt, October 23, 1933

The constantly applied artifices of banking and currency policy have in the meantime become a necessity in order to artificially lengthen the lifespan of the fiat debt money system. Due to the latent potential of extreme money supply inflation, not just infinite credit growth, but also the associated rapid, sharp contractions thereof, it no longer represents a sound basis for the economy, but rather evokes connotations of an earthquake-prone region, in which a tectonic plate fault permanently threatens the achievements of civilization. As a result, the economy has in the meantime degenerated into a political construct, in which the principal objective consists of anticipating exogenous interventions as well as possible and exploiting them for oneself.

It seems strange to us that after seven years of unconventional central bank policy, there is no debate as to whether these measures have any effect at all, resp. whether the situation wouldn't actually be better without QE. The narrative of rising asset prices and a relatively painless way to supposedly sustainable growth is barely questioned.

Unconventional monetary policy is justified by an emergency situation and is only temporary. Or is it not? How simple is the often-promised return to “monetary normality” really? In this context, Japan is an example that proponents of monetary policy experiments would rather not look at too closely. The country is a “model student” of highly aggressive monetary policy. Zero interest rate policy has been de facto in place there for almost 18 years. Every attempt to hike rates came to grief within a few quarters and had to be rescinded again in embarrassment.

Japan thus demonstrates that the monetary policy measures held to bring salvation for many years already have failed, and an exit remains out of sight. Due to the zero interest rate policy, the government was able to amass such a huge amount of debt that a significant increase in interest rates has become illusory for good. If one asks Western monetary policymakers why the prescribed medicine has failed to have a sustainable effect in the land of the rising sun over the past two decades, the cynical explanation is that not enough of it has been taken.

Should inflation expectations rise sustainably in the course of the aggressive reflation program, it has to be assumed that bank deposits will be withdrawn step by step and shifted into alternative investments. Japan's gold demand, which has already tripled last year from a very low level, increased significantly. It is no coincidence that gold in yen terms is trading only slightly below its all time high. We are convinced that the gold price in yen terms will continue to rally significantly in the years to come.

Gold price in JPY

Sources: Federal Reserve St. Louis, Incrementum AG

The sweet, contagious poison of currency devaluation has now – after Japan – also spread to the euro area. The expectation of a European dose of monetary aphrodisiacs has on the one hand led to a sharp decline in the euro's exchange rate (from USD 1.40 to USD 1.04), as well as to a rally in European stock markets and a (final?) once-in-a-century rally in government bonds. We find this reminiscent of a classical crack-up boom. It gives us pause that the temporary, weak economic recovery resulting from the devalued currency tends to be lauded and is barely criticized. If the debasement of a currency could promote wealth and prosperity, Zimbabwe and Venezuela would have to be at the top of the world's economic rankings and Switzerland at the bottom. As is well known, the exact opposite is actually the case.

Readers of our annual report know that we analyze gold primarily as a monetary asset and not as a commodity. In our ninth “In Gold we Trust” report, we will therefore once again take a sober look at the big picture and analyze the gold sector in a holistic manner. We can already pre-empt the conclusion at this juncture: The competitive position of gold relative to paper money and other asset classes has improved considerably in recent months.

********

Ronald-Peter Stoeferle Is Managing Partner At Incrementum

Ronald-Peter Stoeferle is Managing Partner and Fund manager at Incrementum AG, based in the Principality of Liechtenstein. The company focusses on asset management and wealth management and is one hundred percent owned by its partners. Ronald manages a fund that invests based on the principles of the Austrian School of Economics.

Ronald-Peter Stoeferle is Managing Partner and Fund manager at Incrementum AG, based in the Principality of Liechtenstein. The company focusses on asset management and wealth management and is one hundred percent owned by its partners. Ronald manages a fund that invests based on the principles of the Austrian School of Economics.

Before becoming partner at Incrementum, he worked in the research department of Vienna based Erste Group, where he started writing about gold in 2006. He gained media attention when he expected the price of gold to rise to USD 2,300/ounce when the current price was only at USD 500. His nine benchmark reports called "In GOLD we TRUST" drew international coverage on CNBC, Bloomberg, the Wall Street Journal, Economist and the Financial Times. Ronald managed 2 gold-mining baskets as well as 1 silver-mining basket for Erste Group, which outperformed their benchmarks from their inception. He is a lecturer at the academy of the Vienna Stock Exchange as well as at the Institute for value based economics. In 2014, he published a book on investing based on the Austrian School of Economics.

He is a Chartered Market Technician (CMT) and a Certified Financial Technician (CFTe). During his studies in finance at the Vienna University of Economics and the University of Illinois at Urbana-Champaign, he worked for Raiffeisen Zentralbank (RZB) in the field of Fixed Income/Credit Investments.