Gold Withdrawals From The ETF Despite Higher Prices! What Is Happening?

Why are the ETF holdings diminishing despite higher prices?

Sprott/Hempke indicated in their weekly interview of Friday February 22 that since January 30, 2019, when Powell reduced its forecast for rate hikes in 2019, some 34 tons of gold has been withdrawn from the GLD gold ETF whilst with a rising gold price the opposite normally happens, more people buy the ETF. The reason in my point of view that despite the rising gold price there were substantial physical withdrawals is because there must be a huge painful shortage of the physical and the bullion banks are clearly scrambling for it. Some ETF holders must have received huge premiums for their ETF gold holdings that subsequently were withdrawn. In the past the gold price was pushed down in order also to free up the ETF physical gold from the weak hands, investors that don’t hold for the long term.

The ESF (Exchange Stabilization Fund) and the bullion banks defend the US dollar

The cabal shorts gold futures contracts in order to suppress the gold price, which they can only achieve being allowed by the CME using naked futures contracts, contracts that are not backed by the physical gold. Next to that they are believed to have a blank check from the ESF (Exchange Stabilization Fund).

The U.S. Exchange Stabilization Fund was established at the Treasury Department by a provision in the Gold Reserve Act of January 31, 1934. The act authorized the ESF to use its capital to deal in gold and foreign exchange to stabilize the exchange value of the dollar read and thus to suppress the gold price. The ESF as originally designed was part of the executive branch and NOT I REPEAT NOT SUBJECT TO LEGISLATIVE OVERSIGHT!! No oversight always leads to abuse and excesses!

As mentioned the suppression of the gold price is done in order to “defend” the US dollar read against the incompetence of the politicians and civil servants in Washington. After all gold is the mirror image of the reserve currency. Gold is the ultimate benchmark of the real value of the paper currencies. Is the gold price weak that inherently means that the US dollar is strong, after all the gold price is expressed in US dollars. Is the gold price strong that means that the US dollar is weak and thus less trusted as the reserve currency because the authorities have conducted a lousy monetary policy undermining the purchasing value of the currency.

I have often wondered why “they”, the cabal, are allowed to continuously rip off investors just so that the US dollar can cosmetically “keep its value”. Most likely they need the “free market” to be able to achieve their goal of pretending that the low gold price confirms the “strength” of the reserve currency, despite the enormous dilution of the purchasing power of the US dollar following their quantitative easings.

There is a direct relationship between Central banks money printing ($15trn since 2009) and the stock market +300%.

Anyway I believe that these days the situation of unencumbered price “management” by the ESF and cabal are coming to an end because of the deteriorating economic circumstances, the reduction of the balance sheet of the central banks and the enormous dilution of the US dollar. After all the chart below clearly shows that there is a direct relationship between Central banks money printing and the stock market. Since the bottom of the market in 2009, $15 trillion have been printed by the Fed, ECB (European Central Bank) and the BOJ (Bank of Japan). The substantial liquidity injection is the reason why the market is up 300% since 2009. All boats rise with a rising tide! Except for the middle and lower classes!

Though this comes at a cost. Next to the fact that seniors have massively lost out on income and have been impoverished the fact is that people again have loaned too much following the historic cheap money driving up housing prices that have now created their own trap with a very low affordability index. And as we know the housing market is the corner stone for the middle class wealth and consumer confidence. When you have a lot of overvalue in your house you feel rich and you feel you can spend. And when that turns we have 2008 all over again though with the big difference that this time almost all other asset classes and economies are in the doghouse. In other words no rescue no way out.

The massive printing of the paper currencies is now having the opposite effect of achieving the strong economy and currency they in their desperate moves were hoping for. Above certain debt levels you can’t lift yourself out of the problem with debt and especially not when you don’t have any budgetary discipline. The US government ex future obligations is now $22trn. And contrary to fiat currencies which can be printed by the central banks (such as the Fed, the ECB or the BoJ) at will, the supply of gold is naturally limited, it can’t be printed it needs to be mined. This is why historically people have chosen the yellow metal as real money; gold has been considered an excellent store of value over time and a hedge against inflation or loss of purchasing power of the currency. Real gold prices adjusted for inflation (loss of purchasing power) are currently higher than 50 years ago, which means that gold has not lost its purchasing power, in other words a strong indication of its historic value.

Chart 1: Gold price adjusted for inflation (calculated as the ratio of the London P.M. Fix relative to the CPI index) from 1968 to 2017.

To sum up, gold’s purchasing power is remarkably stable in the long run and especially when economic circumstances deteriorate strongly and the paper currencies have been heavily diluted, losing their purchasing power.

Investors are switching from paper (intangible) to tangible assets and the bullion banks are queue jumping because of the lack of physical gold!!

Aware of the imminent dire economic circumstances Investors are increasingly looking for (non-paper) hedges against increasing uncertainty and thus in my opinion the pushing down of the gold price will only increase the attractiveness of physical gold. As a result an increasing number of investors will stand for physical delivery of their futures contracts whilst the pool of registered gold inventories (available inventories at the Comex to back up physical delivery on the paper futures gold contracts) is declining.

And what a coincidence that those bullion banks (the banks that deal in gold) are suddenly queue jumping en masse i.e. they enforce through their position in the market that they get physical deliveries from the exchange before the other investors get their physical gold. Basically this queue jumping of the bullion banks is kind of pure front running ahead of all other investors. Explain to me why this is allowed, why the banks get away with it and why the management of these banks are not in jail? The fact that hardly anybody knows that this happens and understand it doesn’t mean therefore that it is not criminal!

The standing for physical delivery of gold at the Comex (with no physical back-up) is transferred through EFPs to London’s LBMA

As a result of the lack of physical inventories available at the Comex that are a fraction of the total fraudulent (naked futures, futures not backed up by the physical as well on the short as well as the long side) paper contracts that are outstanding (ratio paper futures contracts to physical inventories ranges between an incredible irresponsible 70x-500x) the EFPs (Exchange Futures for Physical) to London are increasing and thus the problem of physical delivery is being transferred from the Comex to the intransparant London gold market ruled by the LBMA, London Bullion Market Association regulations.

EFPs change the nature of the gold futures from a standardized exchange to a secretive bi-lateral contract in order to avoid being “decoded” by investors

What I should emphasize also when these EFPs happen is that thereby the nature of the contract changes from a public standard exchange contract to a private (secret) tailor made (non-standard) bi-lateral (non-exchange, between two parties) contract. And as such it is very difficult to figure out what exactly the conditions (tightness, delivery times, sizes, prices/premiums) are for the gold contracts ruled by the LBMA organization members in London. There are no freely accessible statistics. In fact through the EFPs a smoke screen is being created enabling the dealers to hide from investors how precarious their situation is so that these dealers can go on manipulating the price to their advantage as if everything is honkey dory which is NOT the case.

Insiders are informing me that the tightness in the London gold market (the physical delivery market) is getting precarious

We know from insiders that the physical is really drying up and thus much suppressed paper gold prices by the cabal might actually blow up in their face because of the increasing interest at lower gold prices. The physical price setting (the only true price setting) might finally as result take over from the paper price setting on the Comex and cause a force majeure and major losses for the cabal. Hence why perhaps JPMorgan is suddenly recommending gold as an investment and most likely is going long!?

JPMorgan suddenly recommending gold?

Arguing that the Fed might be eyeing an inflation overshoot, JPMorgan, the biggest cabal bank, suddenly promotes gold and TIPS!? According to JPMorgan the Fed appears to be considering trying to let inflation run hotter than its 2% target to make up for years below that level. Negative real interest rates!? In other words JPMorgan now suddenly likes gold on the idea that the Fed will erode real yields to spur the economy, which would undermine the dollar. Hmm unexpectedly the most important bullion bank is promoting gold, will they rip their own clients off (through their shorting actions) or will they suddenly go long!? Who will find out and sue JPMorgan for their unethical and criminal activities.

In 2018 the central banks bought 640 tons the most in 50 years. Basel III will qualify gold as a tier 1 asset as per April 1, 2019

Perhaps JPMorgan “doesn’t have any choice” because the overwhelming interest of central banks to increase their gold reserves also in light of the Basel III accord qualifying gold as a tier 1 asset as off April 1, 2019. The fact that the central banks have bought 640 tons in 2018, the most in 50 years, clearly contributes to the increasing shortage of the physical. Sprott/Hemke referred to this situation as the one similar to the demise of the London gold pool in 1968 whereby as they called it “the rats were leaving the sinking ship”.

The London Gold Pool was the pooling of gold reserves by a group of eight central banks in the United States and seven European countries that agreed on 1 November 1961 to cooperate in maintaining the Bretton Woods (1944) System of fixed-rate convertible currencies and defending a gold price of US$35 per troy ounce by interventions in the London gold market. The price controls were successful for six years until the system became no longer workable. The pegged price of gold was too low, and after runs on gold, the British pound, and the US dollar France decided to withdraw from the pool. The London Gold Pool collapsed in March 1968.

The central bank gold purchases coincides with the demise of the Petro-dollar, whereby Kissinger in the early 1970’s organized the Saudi’s to price oil in US dollars and re-invest these dollars in US treasuries. In other words the anchor of the US currency to the most wanted and valuable commodity is over.

We now have to focus at the fact that the central banks are purchasing gold, and thus away from the US dollar, as a hedge against the overwhelming global debt and the loss of hegemony of the USA. And in my opinion we should differentiate between the central banks that still support the US dollar hegemony such as the Fed, BIS, the western central banks and the central banks of Japan and the central banks that want to get away from the US dollar as the world reserve such as the Russian and Chinese central banks. The Petrodollar’s backing by oil is being replaced by “upcoming” currencies (RMB, Ruble) looking for a gold backing.

You can print money (very addictive) for a long time till the turning point is reached and all the credit(ability) in a paper currency is gone. Though the US can’t be seen to buy gold!!!

As shown with the collapse of the London Gold Pool these runs on the currencies could happen again following the constant undermining of the paper currencies trying “to rescue” the economies hence the acquisition of gold by many central banks. The US though can’t be seen to acquire gold because it would indicate that they don’t trust their own currency and thus the US dollar would lose its reserve status as the prima facie currency, the global anchor currency. In fact this discrediting process is basically already happening because the Chinese and Russians and other central banks seem to prefer increasing their relative holdings of gold vis a vis their US dollar holdings. Chinese and especially the Russians have been selling their US Treasuries.

Next to that as mentioned gold will qualify as a Tier 1 asset as of April 1, 2019 according to Basel III and will be valued 100% for the purposes of banking viability. Essentially, monetary gold is now regulatory considered risk free (has always been risk-free because it has no counter party risk). This could be the start of a significant development whereby the physical will finally take over from the paper market.

Gold regaining its role as a backstop for paper obligations (money, debt)

In anticipation of Basel III February 2018 already marked a major turning point for gold – monetary gold to be more specific – when the Swiss National Pension Fund switched out of synthetic gold derivatives into physical gold. Monetary gold is defined, in the new Basel III banking capital rules, as “physical gold held in their own vaults or in trust.” One might have to wonder what in trust means! The Swiss decision complied with the new banking standards regarding capital adequacy as it relates to solvency and viability. All Systemically Important Financial Institutions (SIFI) had to comply with the new rules for Net Stable Funding Ratio (NSF) and Liquidity by January 2019.

Lessons learned from the last liquidity crisis, when Lehman Brothers nearly caused a global financial meltdown, forced a rethink in how assets held on an institution’s balance sheet are to be valued. Counter-party risk became extremely important again. In short, when trust between SIFIs fails, liquidity dries up as lending ceases due to solvency fears. The need for liquidity was a key change in the creation of the new standards, and it shone a spotlight on an asset that had largely been ignored for this purpose – physical gold. Another reason is that gold has real value contrary to paper obligations (money, debt) and thus can act as a backstop when the paper obligations fail. Anyway this change could mean in my point of view that physical gold purchases will even further accelerate to the detriment of the paper derivatives.

Libor and repo rates represent the trust in the financial system, they are the prices (read risk) that financial institution loan each other money

As we know in the financial world everything is based on the trust that the counter party can deliver. Between financial institutions that trust is reflected by the libor and repo rates.

The ultra low interest rates has fuelled global debts to $250trn and is affecting the purchasing power of the currencies

Next to that with global debts of $250trn+ and a looming slow down in most countries economies not the least in the Chinese economy as we witness in the German (car industry) economy the fundamentals of these economies and thus the purchasing power of their paper currencies is looking less and less attractive. Hence, being fully aware of this looming dangerous situation the central banks want to increase their gold holdings backing up their paper currencies. As we know gold is money and everything else is credit i.e. an obligation of a third party to deliver a promise which is only as good as his ability to deliver. If his counter-party can’t deliver he can’t deliver and the paper obligation is worthless! And if the counter-party is a person or a central bank, guaranteeing the value or purchasing power of money, that doesn’t matter, it is about being able to uphold your promise. And with increasing debt levels and with budget deficits at unsustainable levels using too high tax burdens and the dilutive printing press the currency will implode under its own weight. And if this happens only for a few not so important economies in the world the problem can be solved but if it concerns the major trading blocks such as China, the EU and the USA we have a problem.

Michael Oliver of MSA shows us the historic perspective that is about to be repeated

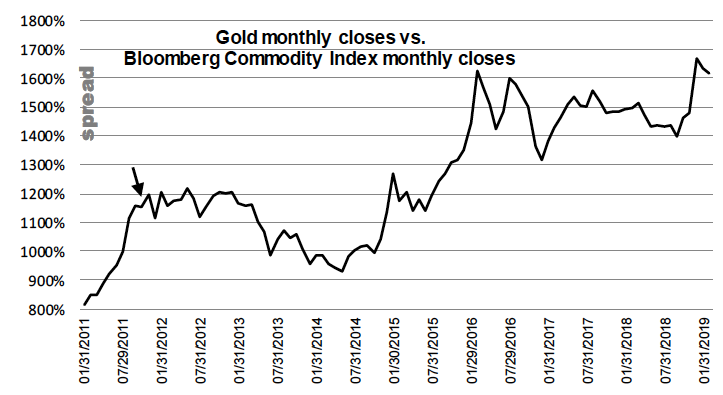

While most analysts think gold responds to inflation (i.e. their narrow notion of commodity price inflation), the reality is that gold took leadership reins early in the commodity boom cycle of 1976-1980 and kept them all the way up. It’s doing the same now. Gold front runs!

Note the down arrow. At that point in late 2011 gold was peaking in net price just above $1900. The spread reflected gold’s sharp drop over the next few years. But gold has since almost doubled in value relative to the commodity basket. It’s not waiting for the category to present us with “inflationary” data points.

MSA suspects gold’s recent surge in relative performance (above chart) is not due to commodity price inflation metrics being broadcast across financial media. Look at the Bloomberg Commodity Index and you’ll see that’s clearly not the case, as BCOM, though now firming, is well in the middle of a two-year-wide base.

Gold can read the clear and evident surrender of central banks. Gold anticipated that, and that’s why it’s been rising constantly since August last year. It was shortly after that gold low that the developed economy stock indices fell into a first void, telltale of topping. CBs were jolted back into their artificial pricing policy syndrome. And it’s MSA’s bet that despite recent eager bidding under developed economy stocks, a multi-year investor preference shift is once again underway. Inexorably. And that shift will vastly favor gold and soon also the bombed-out value category that is “commodities” and related.

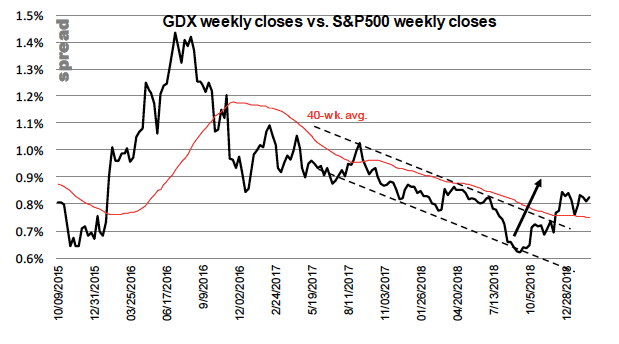

The gold miners’ relative performance vs. the S&P500 turned up before the S&P500 produced its December price collapse. GDX (VanEck Vectors Gold Miners ETF) had earned it. And GDX is still outperforming the broad stock market despite the sharp S&P500 price rally.

Concluding

As Egon von Greyerz rightfully states there is a massive industry that has been created which only lines its own pockets at the expense of ordinary people. If we just take the example of the 2007-9 crash, we know that most investment banks would have gone bankrupt without a massive rescue package by central banks to the tune of $25 trillion including loans credit lines and guarantees. In spite of this, staff at these banks got the same substantial bonuses in 2008 as in 2007, from banks that only survived due to government assistance. Thus, bank profits line the pockets of the bankers while losses are picked up by the state, which means the taxpayers. Where is the accountability?

Ratios like P/E ratio, Shiller’s CAPE ratio, dividend yield, Price to Book ratio, Price to Sales and the Q ratio which is dividing market value by replacement cost of assets are all risk ratios that indicate that the current market is more overvalued than it was in most of the 36 bull market tops in the last 100 years.

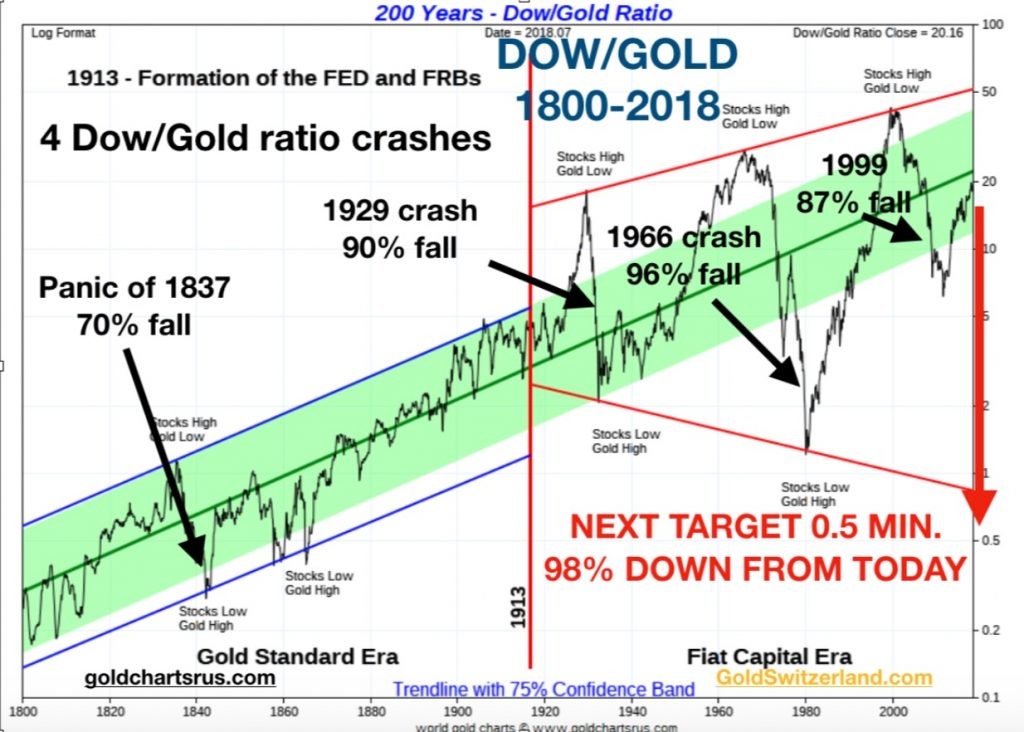

In fact measured against gold the stock market already turned down in real terms in 1999. Between 1999 and 2011, the Dow fell 88% against gold. Since then we have seen a correction up in the ratio and the Dow is now “only” down 55% since 1999. But the correction up of the Dow/Gold ratio is likely to finish in 2019. In 1980 this ratio was 1 to 1 which means that 1 Dow unit was equal to 1 ounce of gold. They were both around 800 at the time.

The next decline of the Dow/Gold ratio is likely to reach 1/2, which means a further fall of 98% from here.

To own physical gold and store it safely outside the banking system is the best insurance against the coming calamity in world markets. Short term, gold in US dollar has attacked the Maginot line as Egon calls it around the $1,350-$1,380 level. This line has been broken by gold measured in many other currencies but not yet in dollars. The reserve currency is the last one to go.

This so-called Maginot line is extremely strong and therefore we might see a few attempts before the price breaks through. I believe that that the banks will try once more to push gold prices down to around $1,240 in order to get the physical gold at the cheap before April 1 (when gold becomes a tier 1 asset) using queue jumping as we know.

Be aware that it is not all sunshine behind the screens because we know that the cabal has huge problems meeting the physical deliveries in London (the delivery market) and despite their physical delivery obligations they continue to queue jumping that should tell us something. The force majeure can’t be far away hence why the cabal banks are also plundering the ETF vaults despite the rising gold prices.

Though understand that when the so-called Maginot line breaks, and April could be the month that this happens following the Basel III implementations, all bets are off and it will signal a massive breach of trust in the US dollar that will tank substantially.

Hedge yourself against paper money that has been diluted like it goes out of fashion and buy tangibles, agricultural land, physical gold and silver and the gold and silver mining companies that are the closest thing to gold and silver futures.

Gijsbert Groenewegen LLD (C)

+1.646.247.1000

+31.6.38.12.70.28

********