Is This It?

In the last issue of this publication, I warned that the Dow Jones Industrial Average and several other key U.S. equity markets had completed a monthly Key Point Reversal top in the month of July. As I have written on several occasions these reversals, whether highs or lows, represent a convincing indication of a change in the price trend. Daily chart price reversals indicate a change in the short term trend; weekly price reversals are indicative of a change in the intermediate price trend and monthly reversals point to a trend reversal over the long term. I have shown you, at least on a couple of occasions, that the HUI (Gold Bugs Index) made monthly key point reversal price tops at every long term cycle price high since the secular bull market began in November 2000 when the HUI reached its secular bear market low of 35.31 points. The last of these was in September 2011, when the HUI made a price peak of $638.59 (U.S.). Since that reversal high, it has been nothing but a series of deteriorating prices for almost all of the gold stocks. Here's the chart that I showed in the 'Special Edition' publication, 'The Natural Behavioral Patterns of Economic Cycles within the Investment Markets', published in November 2013. Key point reversals are by no means present at every trend reversal, but when they do occur they have proven to be very reliable trend reversal indicators.

Thomson Reuters.

Let's get back to the monthly Key Point Reversal High that the Dow Jones Industrials made in July. At the beginning of August the DJIA made a lower price low than the low made in July (16,333.78 points versus 16,563.30 points) thus, setting the stage for a contrary monthly key point reversal low in September. To do that, the Dow had to close at the end of August above the July high of 17,151.56 points; it didn't do that, closing at 17,098.45 points on the last trading day in August. On the other hand, the S&P 500 did reverse the key point reversal high it made in July by making a key point reversal low in August.

September will be an interesting month. Will the S & P 500 confirm its reversal, bringing the Dow along with it during the month or will this index reverse to the downside following the DJIA August non-confirmation of a trend reversal for a continuation of higher prices? We shall see, but whatever the outcome, I am convinced that the U.S. stock markets are on their respective last legs and when the bear market resumes it will resume in unprecedented fury, taking prices far lower than the euphoric bulls can ever imagine. Those of you who know me, know that I haven't written this for theatrical effect. It is my sense that when the powers that be lose their control to offset the natural functioning of the markets, cycles will revert to the norm. Because stock prices have been so skewed by man's interference in their natural market function, prices will over extend on the downside. "It is natural law. Action equals reaction in the opposite direction." W. D. Gann.

Everything that I have written so far, I actually wrote almost a month ago, meaning it to be a part of my September publication. Anyway, September did indeed turn out to be a very interesting month in the stock markets. No, the DJIA failed to follow the bullish key point reversal exhibited by the S and P 500 in August; indeed, the DJIA completed another key reversal high at the end of September, but more importantly so did the S and P 500. I show that to you in the chart below. This is a very compelling reversal, in as much as the S and P 500 has made three monthly reversals in a row, July, August and September. I looked for other examples of such a phenomenon and could not find any. What this tells me is that "This Is It', which is to resurrect the title of my publication published in 2007. Interestingly, it is also the title of Robert Prechter's recent flash warning alert, which he published on September 19, 2014 and concluded with this warning"...., next week the U. S. stock averages should begin their biggest decline ever." You should read that again "...Biggest decline EVER", and that means this decline will be greater than the 89% experienced in the previous winter stock bear market between 1929-1932.

S&P500, Monthly chart Jan 2014 - present.

Thomson Reuters

Mr. Prechter's dire prediction for the stock market is shared by Dr. Robert McHugh who in his weekend report of Friday, September 26, 2014 wrote the following, "The industrials, S&P 500 and NASDAQ 100 all look to have completed large Rising Bearish Wedge patterns from October 2013....Those patterns looked to have topped on September 19th, 2014. That looks to be the top of the multi-decade Jaws of Death pattern that started in 1987, and looks to be the top for Grand Super Cycle degree wave (111), which was centuries in the making." Technicalindicatorindex.com. Wow, if this coming bear market is a correction of a multi century stock bull market it will be as Robert Prechter has written, "The biggest decline ever."

What is interesting about Dr. McHugh's latest prognosis is that before this, he had been anticipating one further correction in the major US stock market indexes, after which he anticipated further upwards price moves to record highs into 2015; these record highs would be the climatic end of multi century stock bull markets.

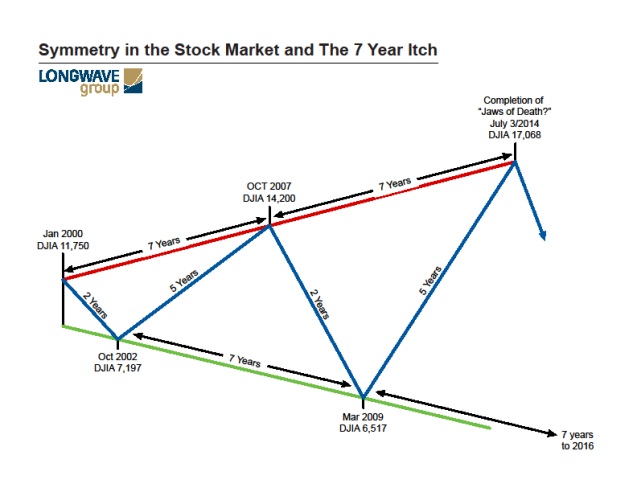

As for me, I could not see the bull market extending beyond 2014. You may remember the following schematic that I produced in the July 11, 2014 Ian's Investment Insights publication.

Allow me to quote from that publication, "Cycles are also suggesting that the peak in stock prices is near and is more than likely to occur sometime in 2014. W. D. Gann, the great cycles proponent and highly successful trader, wrote that the number 7 was a tragic number. I referenced this number and other Gann numbers in my work 'This Is It' (available on the website in the Special Editions section), which was published in 2007 and accurately forecast the stock bear market and the banking crisis. There are two different number 7s associated with the stock market this year. The first is that in numerology terms the year 2014 is equal to seven, 2+0+1+4 = 7. The second is that the year 2014 is 7 years beyond the previous the previous bull market peak in 2007. That bull market peak was itself 7 years beyond the 2000 bull market price peak. The two bear market lows 2002 and 2009 were also 7 years apart. (Above), I show a stylized version of the bull and bear markets since the great autumn stock bull market ended in 2000. Note the beautiful symmetry, which is an important feature of cycle analysis. Each bear market lasts approximately 2 years. The bull market, 2002 to 2007 lasted 5 years and the current bull market is well into its fifth year. The numbers 2 and 5 are Fibonacci numbers and these numbers are used extensively in technical analysis and in particular in Elliott Wave analysis."

In his September 12, 2014 Stock Cycles Forecast publication, Michael Jenkins ( I am a long time subscriber to his newsletter because in my opinion he is perhaps one of the best living market cycle analysts) wrote a synopsis of the importance of the number 7 as it pertained to stock market analysis. "W. D. Gann always talked about the 'death zone' being the 7th unit over in time and he got that from the Bible. God set up the universe with a 7 count and the eighth ‘day’ starting the new octave, so most markets climaxed or crashed near the 7th or 8th period." The days of the week are numbered to 7 to count these times easily..........Seven years has always been a good cycle ever since the mention of Pharaohs biblical dream of seven fat cows being eaten by seven thin cows representing seven years of abundance followed by seven years of extreme starvation. Astrologers know this to be the planet Uranus which changes signs of the zodiac every seven years and signs alternate from positive and negative polarities. The last 100 years has seen a great many collapses and panics at seven year intervals (7, sometimes plus or minus 1 or 6-8 years) so we can see big turns such as 1973 + 7 = 1980 + 7 = 1987 + 7 = 1994+ 6 (7) = 2000 + 7 = 2014 (digits 2+0+1+4=7). From this coming October 8th date ( a blood moon and almost exactly 7 years from the stock market peak in October 2007), eight months back is February 8th.-our last major low. October 8th. this year is a lunar eclipse and that's what hit on almost the exact same date and degree in 1987 which triggered the crash of 1987. Then the crash low was October 19th, this year we have a solar eclipse on October 23rd. From 1987 to 2014 is 27 years and from 1987 27 years back was 1960, which had the final lows of the year in the first and third weeks of October. 27 years prior in 1933 saw a major low in October and 27 years prior in 1906 (the year before the huge panic) the first week of October was a high. This October will be an exact 7 year from the top in 2007 and an exact 12 years from the 2002 low-sure looks like big things happening."

In addition to our own cycle analysis, there is very strong evidence from several independent reliable sources (I have quoted from three of them) who suggest that this Central Bank induced stock bull market is ending. Their prognoses for the immediate future is a long wave winter bear market made significantly worse than the previous long wave winter bear markets because of the ongoing official interference since 2000 in the cyclical nature of markets.

It took an 89% reduction in the index level of the DJIA to correct the 500% increase that this Index rose in value during the great autumn stock bull market of 1921-1929. What kind of price reduction in the DJIA might we expect during this winter bear market following the autumn stock bull market of 1982 - 2000 during which time the DJIA increased by almost three times more than it achieved between 1921 and 1929? I would expect that it would be materially greater than the 1929-1932 89% corrective experience; after all "to every action there will be an equal and opposite reaction."

If for the sake of argument, we concede that the overall loss in this winter bear market will be equivalent to the 90% loss experienced during the 3rd. winter bear market of 1929 to 1932, such a percentage loss would result in a total monetary loss of approximately $19.5 trillion (U.S.). By comparison between 1929 and 1932 the total loss experienced by investors was $68 billion (U.S.), which today would be equal to a little more than $1 trillion (U.S.). Think on that for a moment, a comparable 90% loss in U.S. share price values in this ensuing bear market would result in 19 times the monetary losses experienced in the previous winter bear market. That bear market effectively destroyed the wealth of the American people, which was a primary cause of the failure of the U.S. banking system and the Great Depression.

Not only, will the overall monetary loss attributable to this winter bear market be multiple times greater than the loss experienced in the previous winter bear market, but also, at the onset of this winter bear there exists within the banks and quasi banks an unfathomable exposure to financial derivatives. Derivatives were not even a part of the 'Roaring 20s' scenario.

It should not require much of an imagination to see the utter economic and financial devastation that will be foisted on us by the pending derivatives catastrophe and winter stock bear markets. One prominent and well respected newsletter writer has suggested that this pending disaster will bring about a period something akin the 'Dark Ages.' Whether it is as bad as that dark period in world history following the fall of Rome, or not, what lies directly in our immediate future has to be something significantly worse than the Great Depression of the 1930s.

Financial derivates, the vastly overvalued stock markets and related investment attributes such as ETFs, and seriously overpriced real estate now much recovered from the 2006 -2010 debacle, all of which have been fueled by central bank fiscal and monetary largesse, made possible by grossly dishonest paper money are one obvious cause for the pending calamity. Less obvious, but in my mind just as important is the blatant fraud perpetrated by the banks, particularly by the major U.S. and British banks. These crimes have only been punished by the imposition of fines, which were miniscule in comparison to the monetary gains produced by these fraudulent actions such as mortgages, subprime mortgage debt, Libor, betting against their clients and many other examples. (If you want to understand why it is that the U.S. and British banks are in the forefront of these crimes, I suggest you read, Hidden History: The Secret Origins Of The First World War by Gerry Docherty and Jim Macgregor.)

Reading this book will give you an understanding of the inter-relationships that exists between the major U.S. and British banks and the Federal Reserve and the Bank of England and more importantly the U.S. and British Governments; you will perceive that these three entities are acting in unison to achieve a common objective; you will understand the ongoing wars fostered by the U.S. and supported by Britain and the reason for the Ukrainian revolution, the imposition of Russian trade sanctions and the ongoing demonization of President Putin. This Anglo-American hegemony, carefully implemented since the days of Cecil Rhodes will be seriously threatened in the up- coming economic and financial storm.

As the crisis begins to unfold led by falling stock prices the move to own gold and silver as harbingers of safety will intensify and prices for these two monetary metals will rise accordingly. Below is a monthly chart depicting the spot gold price, It appears that the price of gold has made a triple bottom in June and December of last year and this month, October this year. What is exciting is that the gold price looks to be setting up a monthly key point reversal low this month. The gold price low in September reached $1,205 (U.S.) per ounce and the closing price on September 30th was $1,209 (U.S.) per ounce; the October price low, at this time, is $1,184 (U.S.) as shown on the chart, and that is $25.00 (U.S.) lower than the September low price. All that is now required to set up a key point reversal low for the month of October, 2014, is for the gold price to close the month of October higher than the September closing price of $1,209 (U.S.) per ounce; the higher the close above that September closing price the more emphatic will be the reversal signal.

Spot Gold Price, Monthly Chart

Thomson Reuters

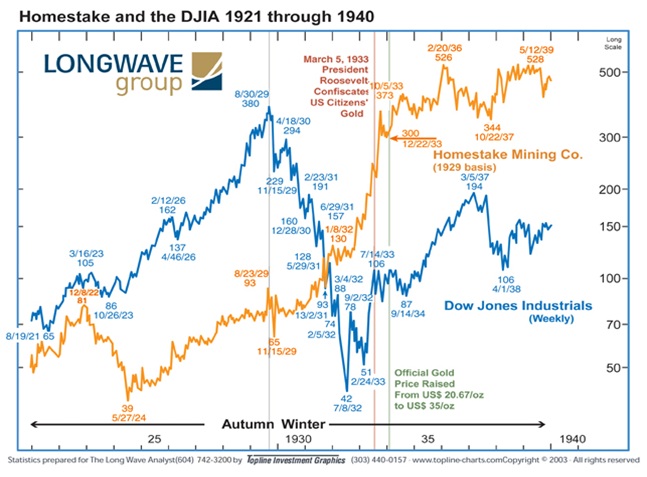

In the meantime, this is the time to be buying the shares of precious metals companies, particularly gold company shares. I have on several different occasions, most recently in the Economic Winter publication of June 17, 2014, with the title, Gold Versus Silver, written about the capital flight to gold and gold shares during the last economic winter depression. This is a quotation from that publication, "It was not only gold itself that frightened investors turned to as their ultimate safe have asset, but it was also to invest in the companies that mined gold and even those that explored for the precious metal. In fact, following the stock market crash in 1929 what remained of capital flowed almost exclusively to gold and shares in gold companies, both miners and explorers." The following chart vividly displays the contrasting price actions of the Dow Jones Industrial s Average and the price of gold company shares, in this case Homestake Mining, both during the Roaring 20s autumn stock bull market and the subsequent stock bear market and the economic winter depression.

You should not forget that the gold price was fixed at $20.67 (U.S.) per ounce until January 1934 when it was increased to $35.00 (U.S.) per ounce. There is no such fix during this economic winter and the price of gold, based on the anticipated demand during this developing economic and financial catastrophe, should soar to an unimaginable level, leading the share prices of both gold miners and explorers in a similar vein.

There should be no misunderstanding about my warning; I am convinced that we are in the initial stages of a terrifying stock bear market, which will reduce share prices by at least 90%. The fall in stock values will be the precursor to a devastating economic depression. This will be a worldwide catastrophe and will lead to extremely dangerous political ramifications.

The Powers That Be will do everything that they can to hold back the impending stock deluge, because they know that once stock prices collapse they will take everything, but gold and silver, down with them. The declines of 2000 to 2002 and 2007 to 2009 were arrested by powerful central bank action. This time, however they have run out of the ammunition that they used during those previous two declines. Administered interest rates are already at, or close to zero and pushing copious amounts of money into the banks has had little positive impact on the economy. Anyway, as Gann wrote in his Outlook for 1929, "When the time cycle is up, no one can stem the tide. It is a natural law." The time cycle is now up and all the actions of the 'Powers that Be' will be futile in their efforts to arrest the impending stock market debacle.

So, to answer the question that is the title of this piece, Is This It? Yes, this is it; there is overwhelming evidence to support the notion that the stock bull market is finished.

********

This information is not intended to be investment advice. Members of the Longwave Group may acquire, hold or sell securities referred to in this document. The companies referred to herein may pay a fee to be listed on the Longwave Group website or referred to in this publication. See the disclosure under the heading “Disclaimer” on this page for further important information.

Ian A. Gordon, The Long Wave Analyst, www.longwavegroup.com

Disclaimer : This information is made available by Long Wave Analytics Inc. for information purposes only. This information is not intended to be and should not to be construed as investment advice, and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific reader. All readers must obtain expert investment advice before making an investment. Readers must understand that statements regarding future prospects may not be achieved. This information should not be construed as an offer to sell, or solicitation for, or an offer to buy, any securities. The opinions and conclusions contained herein are those of Long Wave Analytics Inc. as of the date hereof and are subject to change without notice. Long Wave Analytics Inc. has made every effort to ensure that the contents have been compiled or derived from sources believed reliable and contain information and opinions, which are accurate and complete. However, Long Wave Analytics Inc. makes no representation or warranty, express or implied, in respect thereof, takes no responsibility for any errors and omissions which may be contained herein, and accepts no liability whatsoever for any loss arising from any use of or reliance on this information. Long Wave Analytics Inc. is under no obligation to update or keep current the information contained herein. The information presented may not be discussed or reproduced without prior written consent. Long Wave Analytics Inc., its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein. In addition, the companies referred to herein may pay a fee to Long Wave Analytics Inc. to be listed on www.longwavegroup.com. Copyright © Long Wave Analytics Inc. 2014. All rights reserved.

”Those who cannot remember the past are condemned to repeat it.” Santayana