Macro transition; Goldilocks Now, Deflation Later

The NFTRH view has been for a macro transition from inflation (past) to ‘Goldilocks’ (present) to deflation (later)

Since projecting the Q4-Q1 broad market rally back in November, we have been managing a macro transition within this rally. Based on the leadership of the Semiconductor sector and Tech, it has been dubbed a “Goldilocks” (inflationary pressures not too hot, not too cold) transition, as inflationary pressures ease (the inflation has come and gone, while it’s lagging supply chain and services related effects linger on) and the former inflation trades under-perform.

There is a word for what supply chain and related services are doing and it’s called “gouging” by opportunistic entities squeezing the inflation hysteria for all it is worth. But I digress.

While waiting for the gold stock sector to truly become unique (not quite yet) in the post-bubble environment an honest look at the macro will yield a developing fundamentally positive view for gold mining (details beyond the scope of this article), but also insofar as the macro transition from Goldilocks to deflation has not yet come about, a hell of a lot of quality Tech/Growth stocks beaten down and looking to rally (actually, many have already begun to rally).

So our chain for the stock market has been a microcosm of the Semiconductor > Tech > Broad (SPX) chain we used in 2013, beginning with the Semi Equipment sector’s ramping book-to-bill ratios. Microcosm in this case means shorter-term and interim, whereas the 2013 situation began a multi-year Goldilocks phase. This post from February 28th updated the chain, which was intact then and remains so today.

But the title begins with “macro transition”. We’ve already transitioned from inflationary to Goldilocks, as anticipated. Now, while anticipating another transition into perhaps more severe liquidity problems later in the year we are currently managing a relatively pleasant interim phase. I have been focusing on Semiconductor and key Tech stocks, like the beaten down but growing Cloud security area, for example. Semi is leading Tech, which is leading the broad market which, importantly, has avoided a breakdown through our ‘do or die’ parameter using SPX as an example.

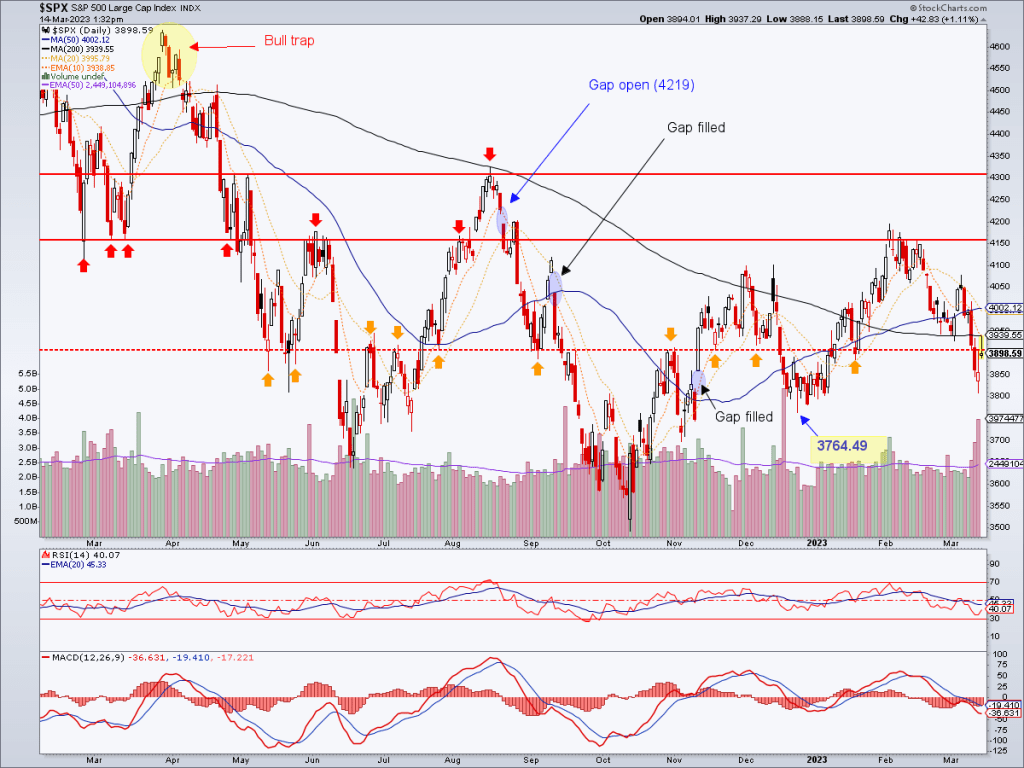

While many charts within the targeted sector areas are looking prospective, the S&P 500 has been our guide as to when to call it a day on the Q4 (2022) – Q1 (2023) broad rally, at least from a US perspective. As is typical of markets, SPX tested the limits of our downside parameters yesterday, amid the banking sector uproar (a post from yesterday shows the destruction there). The broad SPX includes multi-sectors, including the banking sector. It is no wonder it is relatively weak. But the leadership chain linked above is well intact and as long as SPX holds the key December low of 3764.49 and Semi and Tech leadership continue, we can keep the Goldilocks rally view alive going forward.

With a market in transition, it pays to look under the surface and be aware of the dynamics in play at any given time. I am not pro-Tech or pro-Semi. I am just noting what appears to be in play beneath the broad market’s surface. With a couple of banks blowing up the word is that the Fed may have finally broken something, as we’ve been expecting to happen before they even consider stopping the rate hike regime. But we have key macro indicators to watch behind the scenes that as of last weekend (NFTRH 748) were not yet sounding alarms.

Again, I expect Goldilocks to be temporary, maybe very temporary because typically when the Fed halts a rate hike regime that is when troubles brewing beneath the surface tend to bubble up to the surface. The Fed is on the back 9 (and eyeing the 19th hole) of its rate hiking regime and before 2023 is done I expect all those inflation headlines to have given way to the next hysteria, which will be in the opposite direction.

Aside from gold miners and prospective Semi/Tech, for now cash is still paying out a decent income and the bond market may also become constructive. So there’s that too. Be aware of discrete sector character, time frames and parameters like the SPX 3764.49 parameter above. And beware autopilot thinking or the agendas of perma bulls or perma bears going forward. Oh, and over the course of the year, keep an eye on the gold stock sector as the expected relative performance of gold to other markets should eventually manifest in a stellar investment case for quality miners (often a contradiction in terms, I grant you).

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by Credit Card or PayPal using a link on the right sidebar (if using a mobile device you may need to scroll down) or see all options and more info. Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter@NFTRHgt

********