The Path To Monetary Collapse

Few mainstream commentators understand the seriousness of the economic and monetary situation. from a V-shaped rapid return to normality towards a more prolonged recovery phase.

The fact that a liquidity crisis developed in US money markets five months before the virus hit America has been forgotten. Only a rising gold price stands testament to a deeper crisis, comprised of contracting bank credit while central banks are trying to rescue the economy, fund government deficits and keep the market bubble inflated.

The next problem is a crisis in the banks, wholly unexpected by investors and depositors. At a time when lending risk is soaring off the charts, their financial condition is more fragile than before the Lehman crisis. Failures in European G-SIBs in the next month or two are almost impossible to avoid, leading to a full-blown monetary and credit crisis which promises to undermine asset values, government financing and fiat currencies themselves.

We can now discern the path leading to the destruction of fiat currencies and take reasonably guesses as to timing.

How central banks view the current situation.

The financial world is bemused: what is it to make of the economic effects of the coronavirus? The official answer, it seems, is on the lines of don’t panic. The earliest fears of millions of deaths have subsided and in the light of experience, a more rational approach of easing lockdown rules is now being implemented in a number of badly hit jurisdictions. Whether this evolving policy is right will be proved in due course. But the motivation is moving from saving lives to restricting the economic damage.

While I am a critic of the inflationist policies of central banks, it is always valuable to look at monetary policy from a central banker’s point of view. Last Friday, Andrew Bailey, the new Governor of the Bank of England, gave an interview to Chris Giles of the Financial Times, where he spoke frankly and reasonably freely about the challenges the Bank faced in common with other major central banks.

Regarding inflation, from his comments it is clear Bailey defines it as changes in the general level of prices, which is hardly surprising, since central banks are mandated to target it. He believes that the rate of price inflation will fall towards zero, citing recent moves in the oil price as a major factor, though the oil price has since recovered. This gives him room to use monetary policy to its greatest extent.

His view was that monetary policy would minimise what he called “scarring”. This is the new buzzword for economists who generally dismiss the economic effects of the current crisis as being temporary, as in when it heals the only evidence left will be a scar. In other words, some overindebted businesses will fail and others would be victims to changes in consumer patterns once normality returns. Therefore, the working assumption is that once the coronavirus crisis is behind us the economy would broadly return to normal, and while he didn’t specifically say it, he expectats is a V-shaped recovery, possibly with a moderate time element to it.

The bank is undertaking a £200bn programme of quantitative easing, which amounts to two-thirds of Britain’s expected funding requirement relating to the coronavirus, in order to satisfy the following policy objectives:

-

To stabilise financial markets, buying £50-60bn of gilts every month, in common with actions of other central banks in their markets. This suggests the economy is expected to be on the way to recovery by late-July.

-

To reassure the market that extra government debt would be absorbed and to smooth the profile of overall government borrowing. This will enable the bank to keep gilt yields low, and those of corporate bonds as well.

-

To meet economic objectives. In other words, pursue a Keynesian policy to return to full employment.

-

To address counterfactual issues that can be expected to arise if the Bank did not do QE. Presumably, other than disrupted markets Bailey was referring to fears of deflation in the absence of monetary stimulus.

If Bailey is right and QE of £200bn will see the British economy through the crisis, then that £200bn will be an addition of a little more than 10% to the national debt. The addition to February’s M3 money supply is 6.8%, which is hardly a problem. But there will be trouble if he is wrong, glitches that could arise from one or more of three sources. If other central banks, principally the Fed, dilute their currencies by a larger amount proportionately, the effect on commodity prices, particularly agricultural products, could be to drive them up in sterling terms, helping to undermine sterling’s purchasing power for life’s essentials. Secondly, 28% of gilts in issue are owned by foreigners, who, needing the money in their own currencies, are likely to turn sellers. The third threat is of systemic failure, requiring extra expenditure to rescue one or more major banks and to manage the fall-out.

There is little doubt that Bailey’s thinking is shared by his counterparts in the other major central banks. Besides the threats listed above, the mistake is to simply assume the economy is an entity that does not change materially over time. While seeming an innocuous mistake, it leads to the belief that there is a normality to which to return. Bailey dismisses the problem by saying some businesses won’t survive, and others might have to change. But he is clearly banking on a return to normal, when there is no such thing. It is the proper function of economic, monetary and credit analysis to divine the benefits and threats that make the future different from the present.

Issues of credit

By definition, central bankers do not fully understand credit cycles, otherwise they would have done something to fix their disruptive nature long ago. Instead, they believe in business cycles, which central bankers view as disrupting monetary policy, thereby muddling cause with effect. Conveniently for state organisations, central banks place the blame for irrational behaviour on the private sector. The banks, so obviously the cause of credit cycles, are seen to be merely responding to changing business conditions and must be discouraged, in their own interests, from making the situation worse at a time of periodic crisis.

But central bankers play their part in credit instability by encouraging banks to extend credit to stimulate the economy in the first place. That fact alone makes it nearly impossible for them to accept the consequences of their monetary policies. Central bankers like Andrew Bailey not only look at bank credit through the wrong end of the telescope, but they do not see a credit crisis in the making. This amounts to an ignorance that explains why they believe that the coronavirus is simply a one-off hit, and after a short period of time, everything can return to normal, so long as the recovery is properly managed.

Their simplistic approach does not explain the liquidity stresses in the US banking system that surfaced last September, long before the virus had infected anyone. It does not explain why the Fed was forced to abandon its attempt to reduce its balance sheet, over five months before the first virus casualty occurred in the US. It ignores the consequences of the tariff war between America and China, which collapsed international trade by the beginning of 2019. Central bankers have been blind to evidence that the world was already tipping into a recession, and that commercial banks were, and still are, dangerously leveraged in the face of escalating loan risk.

The bureaucrats in central banks and banking regulatory bodies believe they have insulated commercial banks from the extreme risks of over-lending. Since the Lehman crisis, rules and compliance measures have been put in place designed to reduce these systemic risks, and periodic stress tests have been run from time to time to establish the level of existing risk. Unfortunately, stress testing appears to be designed not to expose systemic weakness but to confirm it no longer exists.

A new paper by Dean Buckner and Kevin Dowd has examined the current position of UK banks, which is instructive in the wider sense about the relationship between central banks, regulators and commercial banks. It concludes that “the core metrics of the Big Five UK banks have deteriorated sharply since the New Year, and even more since the end of 2006, i.e., the eve of the Global Financial Crisis.” It goes on to say,

“The BoE’s ‘Great Capital Rebuild’ narrative about a strongly recapitalised UK banking system is little more than an elaborate, and occasionally shambolic, window dressing exercise. The BoE focused most of its efforts on making the banking system appear strong by boosting banks’ regulatory capital ratios instead of ensuring that the banking system became strong through a sufficiently large increase in actual capital meaningfully measured. The result is that the UK banking system enters the downturn in a worryingly fragile state and avoidably so.”

The authors did not spring this on Britain’s central bankers and regulators all of a sudden. For almost a decade, Professor Dowd has written and co-authored papers warning of the inadequacy of official attempts to strengthen the resilience of the banking system to systemic shocks. And now, a weaker banking system is tasked with supporting the non-financial economy, where lending risk is soaring off the charts.

It is not just the UK banking system that’s in trouble. While the Buckner & Dowd paper confines itself to UK banks and there are differences in the detail, we know that banking regulation is standardised across borders, and the motivation for stress tests to see no evil is common to other major central banks. A central point, missed by most observers, is that the markets are telling us there is a banking crisis already, with bank share prices significantly lower than book values.

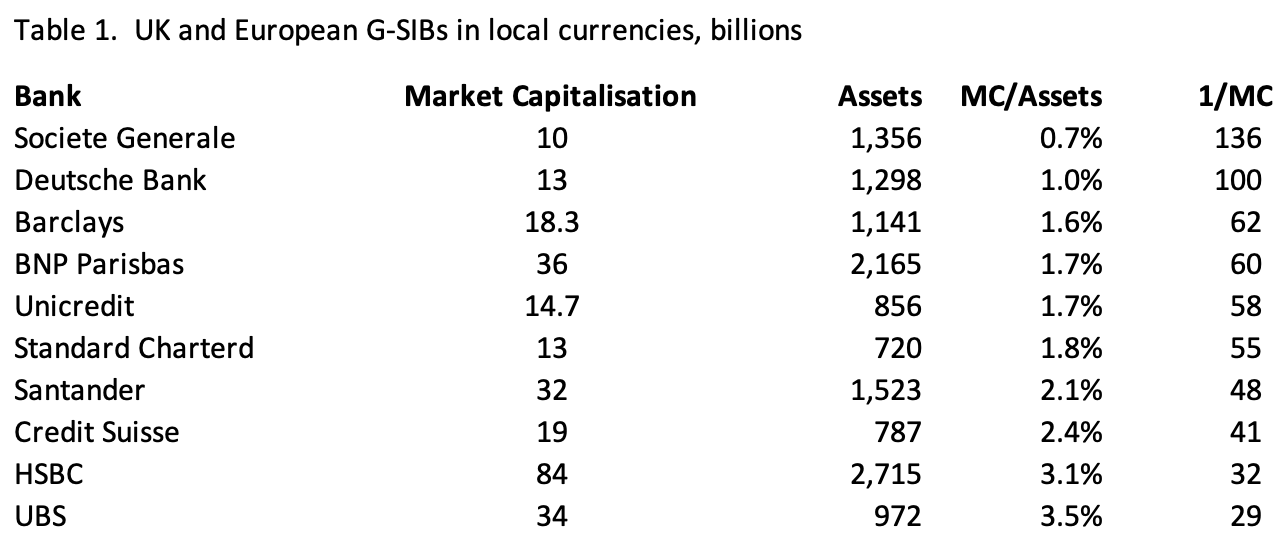

The authors go further, pointing out that the relationship that matters most is between total assets and market capitalisation, the true forward-looking value independently placed on a bank in the markets instead of a static accounting figure for shareholders’ capital in the balance sheet. In the case of Barclays Bank its assets relative to market capitalisation gives a leverage for shareholders of 62 times at a time of increasing lending risk. Put another way, additional loss provisions of only 1.6% of the balance sheet asset total wipes out the bank’s market capitalisation. Major Eurozone banks are in a similar or worse condition, as shown in Table 1, of all UK and European designated and listed global systemically important banks (G-SIBs). The G-SIBs are meant to have extra capital buffers to lessen the likelihood of a repeat of the Lehman crisis.

Clearly, it is virtually impossible to see some of these highly leveraged banks surviving today’s deteriorating loan conditions, nor is it possible to imagine that if one or more of them fail how they will not take down other banks.

As well as believing their own wise monkeys, Andrew Bailey and Christine Lagarde should be praying on their knees that the recovery will be V-shaped and rapid, because the banking system might not even survive that, let alone anything worse. But the outlook is significantly worse because of the pre-existing slide into global recession. The G-SIB bankers’ problem is managing the risk they already have to contend with and not the additional risk the central banks now wish them to bear.

Looking ahead, with increasing certainty we can expect a European and British banking crisis. There is no material reason for it not to happen. The Keynesian debt machine has ploughed on regardless since the Lehman crisis and roughly doubled the debt problems that led to it. The evidence from the Bucknall & Dowd paper is that the banking system, in the UK at least and by extrapolation in Europe and almost certainly elsewhere, is less fit to deal with a crisis on the Lehman scale, let alone the larger one ahead of us. And on top of all that the coronavirus has shut down the global economy. The best possible outcome is that governments and non-financial private sectors emerge with substantially more debt.

Given these factors, it is nearly impossible to argue convincingly that a banking crisis will not emerge very soon, perhaps in as little as a month or two. A banking and systemic crisis will raise the costs for central banks and their governments considerably, not just because they will have to fund bail-outs, but they will also have to cover the associated fallout, such as the inevitable evaporation of interbank credit in the financial sector and of bank credit from non-financial borrowers.

We now know with the greatest certainty what the policy response will be: a further acceleration of base money inflation. In the UK’s case, the estimated cost of £300bn to the exchequer of the coronavirus will turn out to be an appetiser not just for a main course but for the full-blown banquet. And what applies to the UK will apply to the other major advanced nations which lack the genuine savers to fund it all.

The golden canary

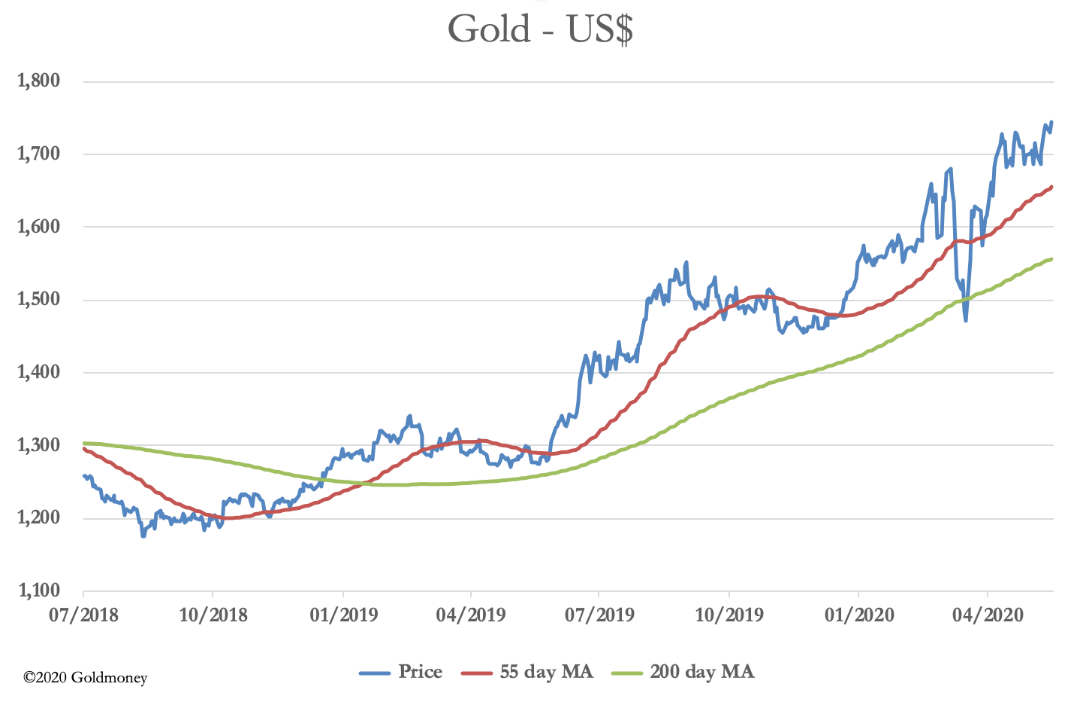

At the time of writing few if any headline-writers in the media have pointed out the dangers to the global banking system from the coronavirus shutdown and the contraction of bank credit. Equity markets have rallied strongly in recent weeks and bond yields have remained low. As forward indicators, these financial markets communicate an ethereal stability. The only sign that black swans, a common sight nowadays, are peddling furiously while appearing calm above the surface is in the gold price. Measured in US dollars, while it is yet to conquer the highs seen at the time of the last Eurozone banking crisis, it appears to be on its way to doing so. The chart below shows how the gold price has over the last twenty months.

In August 2018, it first became clear that America’s tariff war against China was disrupting international trade, which coincided with the gold price setting off on its current bullish run. More recently, gold markets and their derivatives faced unprecedented stresses as bullion banks running short positions have been wrongfooted by changes in monetary policy responding to the coronavirus. So far, gold has been doing what one would expect: discounting increasing rates of future monetary expansion.

But it also acts as a warning of troubles to come. The shock it has yet to discount is the rising systemic risk from bank failures. Barring successful intervention to suppress it, a sharply rising gold price must be the logical outcome from an increasingly certain banking crisis, as people flee bank deposits in favour of physical bullion held outside the banking system.

In previous fiat currency inflations, there has always been a cash alternative to bank deposits. A bank run created increased preferences for cash. At the least, prices of goods did not rise as a direct consequence of systemic crises, and it is worth noting that increased cash hoarding tends, if anything, to lead to falling prices. That can no longer be the case. Retail banks everywhere have been instructed to discourage the disbursement of even relatively small amounts of cash, making it virtually impossible for a depositor to encash all but the smallest deposits. Unless a depositor already has an account with a bank he is confident is safe, he has no alternative but to spend the deposit and give someone else the headache of being a creditor in a failing banking system.

Financial assets are also likely to be unsafe beyond the very short term, and the restriction of bank and mortgage credit in these conditions makes residential and commercial property a bad bet as well. Our frightened depositor is left scrabbling for alternatives to money in the bank, and therefore as a measure of how the crisis unfolds, the gold price is likely to be the most reliable indicator.

For this reason, a gold price rising sharply will not be welcomed by the major central banks, who will rightly fear it is an indicator of declining confidence in the monetary system. Central banks in emerging economies have a different problem, seeing the dollar upon which they depend failing. Undoubtedly, this has encouraged many central banks in this category to build gold reserves as a dollar substitute, at least until the way to a new currency regime can be seen.

The path to fiat obscurity

With the knowledge that the situation is considerably more serious than just a temporary COVID-19 interruption, we can be certain of a lethal combination of mounting bad debts and bankers desperate to contain escalating lending risks. The situation invokes the ghost of Irving Fisher, who was credited with describing the destructive workings of a debt-deflationary spiral driving the economy inexorably into a depression. Central banks will do everything they can to avoid a debt-driven depression, but it is likely to prove an insurmountable task. With a high degree of certainty, the result will be bank failures and bank rescues. And with commercial bankers fearful of their own bankruptcies, they will be poor transmitters of raw base money into the non-financial economy.

From these obstacles to monetary planning, we can tentatively sketch a path towards future events, some of which that are likely to run concurrently, including the following:

-

The first G-SIB failure will initially trigger widespread liquidations of bank-issued bonds and flights of large uninsured deposits from the riskier banks. Capital flight creates funding difficulties for vulnerable banks, and wholesale money markets will seize up. Attempts to proceed with bail-ins, which have been enacted into law by most if not all G20 nations will only make the situation worse. Bail-ins were designed to shift the cost of bank rescues to the private sector instead of governments, which is the case with bail-outs. Therefore, as banks fail there will be added penalties for bond holders and large depositors.

-

Market capitalisations of listed banks will take another lurch downwards, pushing price to book ratios substantially lower. Governments, sovereign wealth funds and central banks are likely to mount emergency support operations for the shares of the G-SIBs and all other listed banks at risk in an attempt to calm markets.

-

After an initial panic, the determination of the authorities to support the banks may buy a brief period of stability. As lockdown restrictions are abandoned, we can expect a partial recovery in the wider economy, fuelled by essential maintenance and catch-up activities that have been put on hold by lockdowns. At this point, everyone heaves sighs of relief in the hope that the worst is over.

-

Following a temporary period of relief, high levels of unemployment and consumer caution are likely to restrict further economic recovery. Real assets held as bank collateral will continue to fall in value, renewing pressure on lending banks. It will become increasingly obvious that global and local economies are not returning to normal with the ending of the virus. Following an anaemic recovery from the easing of lockdowns, it will be apparent that central bank attempts to use a broken banking system to funnel credit to the non-financial economy is failing. Small and medium size enterprises, which typically contribute a Pareto 80% of all economic activity is unlikely to obtain the financial support more easily accessed by big business.

-

Residential property prices will fall, in many cases heavily, as a consequence of lack of demand, risk aversion among buyers and lack of affordable mortgage finance upon which prices are marginally based. Commercial property values will also decline, driven by falling retail and office demand. Both sectors are important loan collateral for the banks, adding to systemic woes.

-

Seeing deteriorating economic conditions, central bankers with an eye to the immediate effects on the consumer price index will be encouraged to double down on monetary inflation, principally to support financial markets. They will see it as the only way to keep their governments out of a trap comprised of a combination of rapidly rising debt and the cost of financing it.

-

Inevitably, government bond prices will begin to reflect the heightened levels of government deficits and the consequences of inflationary funding. Central banks will find they are the only significant buyers of government and corporate debt. Their resistance to raising interest rates will then be undermined by market reality.

-

The general public will be more concerned with rising food prices, energy, and others of life’s essentials, a process which has already started. Throughout history, it has been the economic and social destruction wreaked by the rising prices of these basics that has led to price controls and loss of public confidence in government money. At this point, the public is likely to finally realise that it is the currency that is losing its utility, and that it must be discarded as quickly as it is obtained.

Timing

Following a banking crisis, deteriorating economic and monetary conditions are likely to evolve more rapidly than circumstances might suggest. Information, global communications and the interconnectedness of markets all suggest it. The evolution of cryptocurrencies, such as bitcoin, has made millennial generations more aware of monetary debasement than their parents. But most importantly, by cutting off holding cash as an escape from bank deposits, an attempt by a population to move deposits out of banks will result in the immediate purchase of non-monetary goods. Cash has been regulated out of this function and the reservoir effect of it delaying the price consequences of a crisis no longer exists.

Governments and central banks can be expected to cooperate with each other to stop their currencies collapsing, but ultimately it is a matter for the general public. While inflations have persisted for considerable periods, the final collapse, when the public realises what is happening to money, in the past has typically taken between six months and a year. The German inflation 97 years ago started before the First World War, but its catastrophic phase can be identified as starting in May 1923 and ending the following November. John Law’s monetary collapse, the closest parallel to that of today, ran from approximately February 1720 to the following September.

In the run up to its collapse, Law’s Mississippi experiment depended increasingly on money-printing to support financial asset values. The same inflationary policies apply today. The end point of Law’s inflationary stimulation is lining up to be identical with our neo-Keynesian experiment, and on that basis alone is increasingly likely to come to a rapid conclusion.

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

Twitter: @MacleodFinance

MOBILE: +44 7790 419403

Goldmoney

The Most Trusted Name in Precious Metals tm

NEW YORK | ST. HELIER | TORONTO

Publicly Traded Symbols: CA: XAU | US: XAUMF

© 2020 GOLDMONEY INC. ALL RIGHTS RESERVED. THIS MESSAGE MAY CONTAIN CONFIDENTIAL OR PRIVILEGED INFORMATION. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE ADVISE US IMMEDIATELY. THIS MESSAGE IS FOR GENERAL INFORMATION ONLY AND SHOULD NOT BE CONSTRUED AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY SECURITIES OR ANY OTHER FINANCIAL INSTRUMENTS. WE DO NOT PROVIDE TAX, ACCOUNTING, OR LEGAL ADVICE, AND RECOMMEND THAT YOU SEEK INDEPENDENT PROFESSIONAL ADVICE IF NECESSARY. WE CONSIDER INFORMATION IN THIS MESSAGE RELIABLE BUT WE DO NOT REPRESENT THAT IT IS ACCURATE, COMPLETE, AND/OR UP TO DATE AND IT SHOULD NOT BE RELIED ON AS SUCH. OPINIONS EXPRESSED ARE OUR CURRENT OPINIONS AS OF THE DATE APPEARING ON THIS MESSAGE ONLY AND ONLY REPRESENT THE VIEWS OF THE AUTHOR AND NOT THOSE OF GOLDMONEY INC OR ITS SUBSIDIARIES UNLESS OTHERWISE EXPRESSLY NOTED.

Notice: This email may contain confidential or privileged information. If you received this email in error or believe you are not the intended recipient, please notify the sender immediately and delete this email without forwarding or opening any attachments. Thank you for your cooperation and attention.

********