Post-Lehman Legacy And The Gold Price

Have we learned anything from Lehman Brothers’ bankruptcy? On Saturday, there was a 10-year anniversary of the symbolic beginning of the global financial crisis. So it’s a great opportunity to discuss lessons from the Lehman’s collapse and the post-crisis legacy for the gold market.

Too Little Capital

10 years ago, Lehman Brothers collapsed, which is commonly considered as a symbolic beginning of the Great Recession. We analyze thoroughly lessons from the Lehman’s bankruptcy for the gold market in the upcoming October edition of the Market Overview. But it is such a vast and important topic that we decided to write about it today as well. In contrast, we will focus on what we have not learned from Lehman Brothers’ collapse.

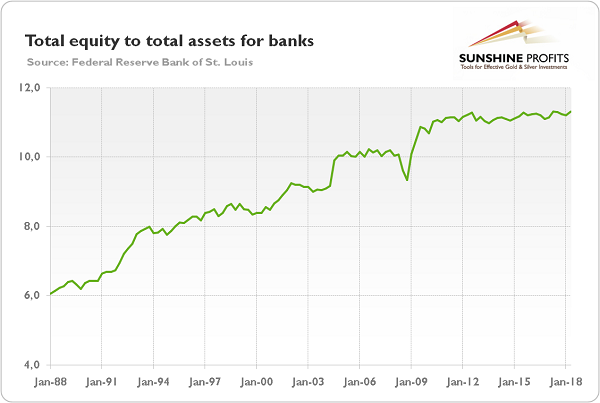

In short: the global financial crisis was caused by excessive indebtedness. Banks had too much debt and too little equity, so they couldn’t bear the losses they faced. But little has changed. Sure, the commercial banks were recapitalized, but the financial system remains generally fragile like back in 2007-2008. As the chart below shows, the total equity to total assets is 11.3 percent. It is more than one percentage point higher than banks had had on the eve of the crisis in 2008, but it is not enough, by any reasonable measure (especially that the weighted average tangible common equity ratio at the six largest U.S. banks is even lower). The implication for gold is clear: when another crash comes, it may quickly transform into a banking crisis, if banks do not have adequate capital. Gold will shine then.

Chart 1: Total equity to total assets for US banks from Q1 1988 to Q2 2018.

Too Much Debt

The pre-crisis boom was fueled by easy money and low interest rates. Even people with no income, no assets and no job were given loans. As a result, the global debt surged from $84 trillion at the turn of the century to $173 trillion at the time of the 2008 financial crisis. The problem is that 10 years after the collapse of Lehman Brothers, due to the ZIRP, the global debt ballooned to $250 trillion. We may call it the post-Lehman legacy.

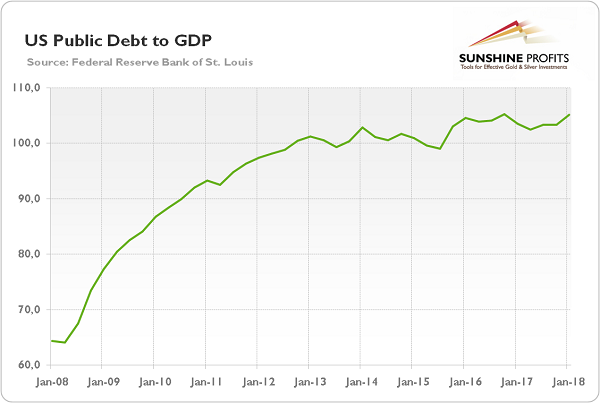

Of course, the situation differs depending on where you look. The US households and financial corporations have reduced their leverage. But nonfinancial companies and government have increased their indebtedness (as the next chart shows). Similar trends are seen in other advanced and even emerging markets. In particular, China’s debt level has exploded since 2008.

Chart 2: US public debt to GDP (as %) from Q1 2008 to Q1 2018.

Although that massive indebtedness does not have to trigger a crisis in the near future, the leverage seems to be unsustainable in the long run. Which is approaching due to the Fed’s tightening cycle. In particular, the emerging markets are exposed to higher rates and stronger greenback. But the governments of advanced countries are also in trouble. They will have to either raise taxes decisively (which are already high) or print money. If we see higher inflation and more central banks’ meddling with the economy, the price of gold should finally rise.

Implications for Gold

It’s true that the financial system is safer than 10 years ago. But it does not matter. The real question is whether it is safe enough. We are not doomsayers, but we are also not incorrigible optimists who turn a blind eye to problems. Banks have more capital, but it may be still too little, especially in Europe. The financial system is less fragile, but the governments and central banks are less capable to cope with a crisis. We have more of maybe even smarter regulations, but the risks have migrated to non-regulated areas. The global economy has recovered, but the road to growth was paved with debt. And as such it is not a sustainable growth model. It’s a one-way street. But, hey, guess what is at the end of that road. Yes, you are right: gold.

Arkadiusz Sieron

Sunshine Profits - Free Gold Analysis

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017. He is a board member of the Polish Mises Institute of Economic Education, author of several dozen scientific publications (including in such periodicals as the Journal of Risk Research, Prague Economic Papers, Quarterly Journal of Austrian Economics, and Research in Economics), and a regular contributor to GoldPriceForecast.com and SilverPriceForecast.com. His two books, Money, Inflation and Business Cycles and Monetary Policy after the Great Recession, are both published by Routledge. Arkadiusz is also a certified Investment Adviser, a long-time precious metals market enthusiast, and a free market advocate who believes in the power of peaceful and voluntary cooperation of people.