Price Inflation Rose in June to a Five Month High—But Don’t Blame Tariffs

Price inflation is moving up again, in spite of President Trump’s repeated (and false) claims that prices are falling. The media isn’t right either, though, since much of the media consensus about June’s stubbornly high price inflation trend is that it was caused by tariffs. Tariffs however, are not inflationary. The price inflation we now see is the continued legacy of the monetary inflation of Trump-Biden efforts to embrace huge deficits and pressure the Federal Reserve to push interest rates downward with easy-money policies.

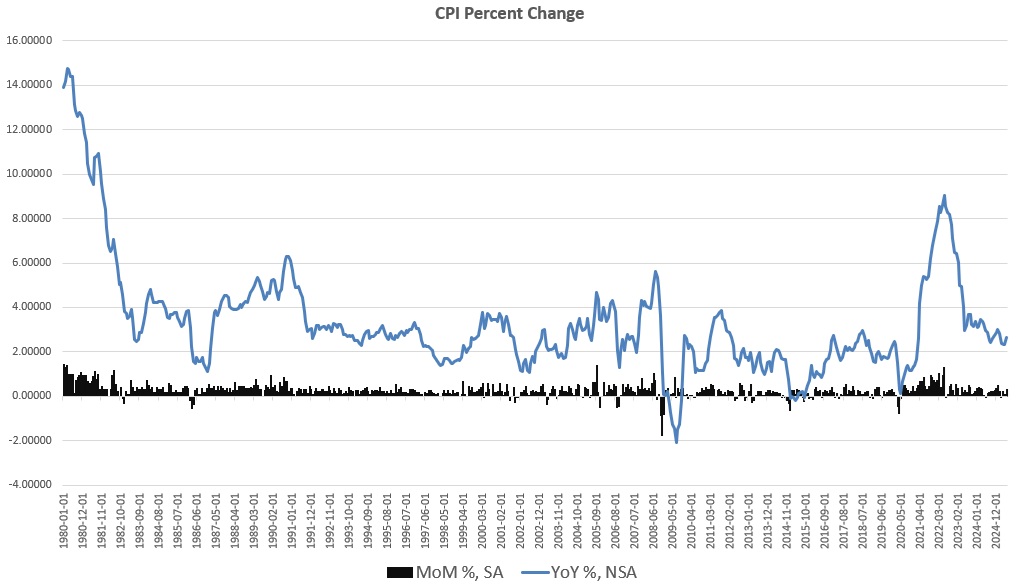

According to the latest price inflation data from the Bureau of Labor Statistics, the consumer price index rose 2.7 percent year over year, and 0.3 percent month over month. That’s the largest year-over-year increase in four months, and the largest month-to-month increase since January 2025. June’s CPI increase also places CPI growth above of CPI growth rates experienced during September of last year. At that time, Fed Chairman Jerome Powell had declared that price inflation was rapidly moving back toward the Fed’s two-percent target. Nine months later, we can see the Fed’s forecasters were clearly wrong, as the CPI has increased by 2.1 percent in that period.

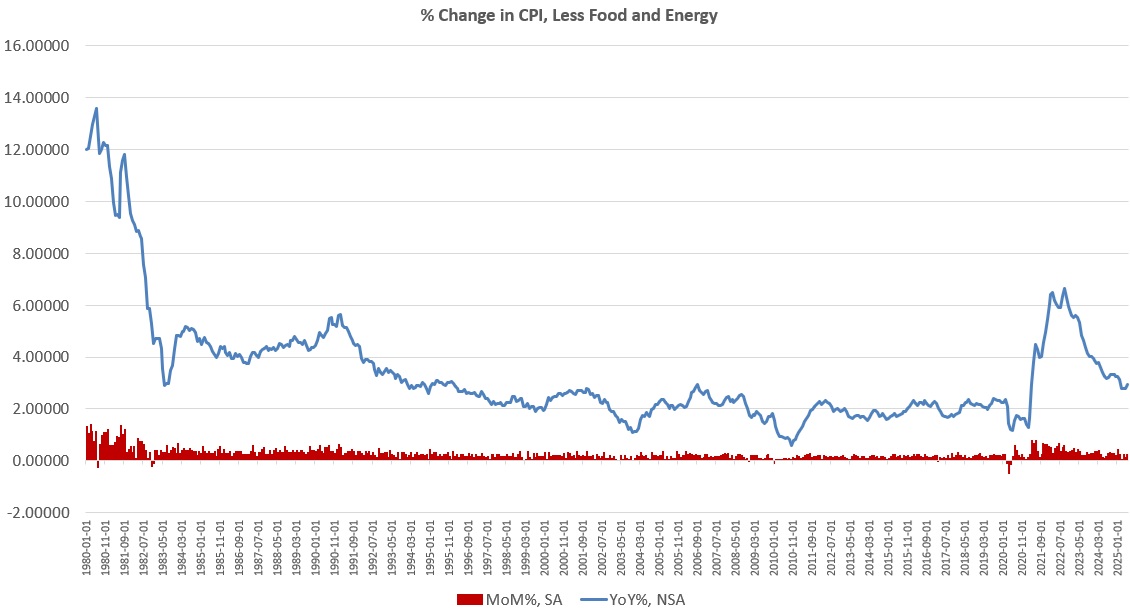

We find a similar trend if we look at so-called “core CPI” which removes volatile food and energy prices. Core CPI also hit a four-month high in June, measured year-over year. Measured month-to-month, core CPI hit a five month high in June.

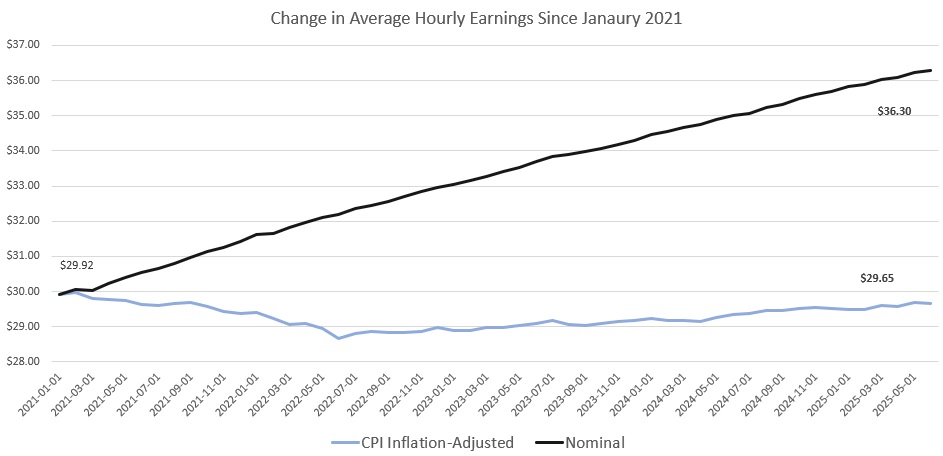

Put into larger perspective, we find that ongoing price inflation continues to ensure that real wages have stagnated for years. For example, since January 2021, average hourly earnings have increased by 21 percent. During that same period, however, CPI inflation has increased by nearly 22 and a half percent. Put another way, the average hourly earnings increased from $29.92 from January 2021 to $36.30 in June 2025. In real, inflation-adjusted terms, however, average hourly earnings fell from $29.92 to $29.65 during that same period. Wages simply have not been keeping up with price increases.

In its comments on June’s CPI report, however, the Trump White House stated in a press release that “prices for everyday Americans continue to fall” and crows that core inflation “beat expectations.” First of all, “beating expectations” does not mean price inflation has improved. To “beat expectation” means simply to come in slightly less bad than what forecasters who were expecting. “Beating expectation” is something that investors follow, but the concept is irrelevant to the real economy. Moreover, it is absolutely not the case that prices “continue to fall” as the White House claims. Naturally, the White House public relations workers point to the few places in the report that show falling month-to-month prices, specifically, new and used vehicles. Virtually all other categories—including shelter, medical care, food, and energy, showed rising prices over the period, however. Year over year, shelter prices were up 3.6 percent, medical care was up 3.4 percent, and food was up 3 percent. This is not an economy in which basic expenses are becoming more affordable.

(Moreover, CPI core inflation has now been above the Fed’s two-percent target for 51 months. CPI has been above the target for 52 months. PCE, the Fed’s favored measure of price inflation, has been above the target for 51 months.)

In media coverage of the report and rising prices, most outlets take the position that rising prices are explained by new tariffs imposed by the administration. While it is true that tariffs will indeed increase prices in areas most directly impacted by tariffs, this is not “inflation” in the strict sense. The conventional definition of price inflation is that it is a general increase in prices. Tariffs—which are taxes—do not cause a general increase in prices because, in the absence of monetary inflation, rising prices in some areas will lead to falling prices in other areas.

For example, steel tariffs will indeed cause the price of steel to go up because the tariff will limit the supply of steel at the former non-tariffed price. Assuming that the demand for steel remains the same, the steel tariff will cause prices to rise. Unless the supply of money goes up, though, rising steel prices will leave less money available to purchase other goods, so prices in other areas will go down. Thus, the tariff by itself will not cause a general increase in prices. It will only cause prices to go up in some areas and down in others.

So, it is not accurate to say that tariffs cause inflation in any precise sense. We can only say that tariffs cause rising prices in some areas—assuming stable demand. Indeed we could argue that tariffs are deflationary in many cases because they raise the prices of important inputs for domestic production and thus force down labor demand and wages. Overall demand will then fall, and there will be deflation. This doesn’t mean tariffs improve the economic situation, of course. Tariffs are simply sales taxes on goods Americans wish to buy, and like all taxes, tariffs choke demand by leaving Americans will less disposable income.

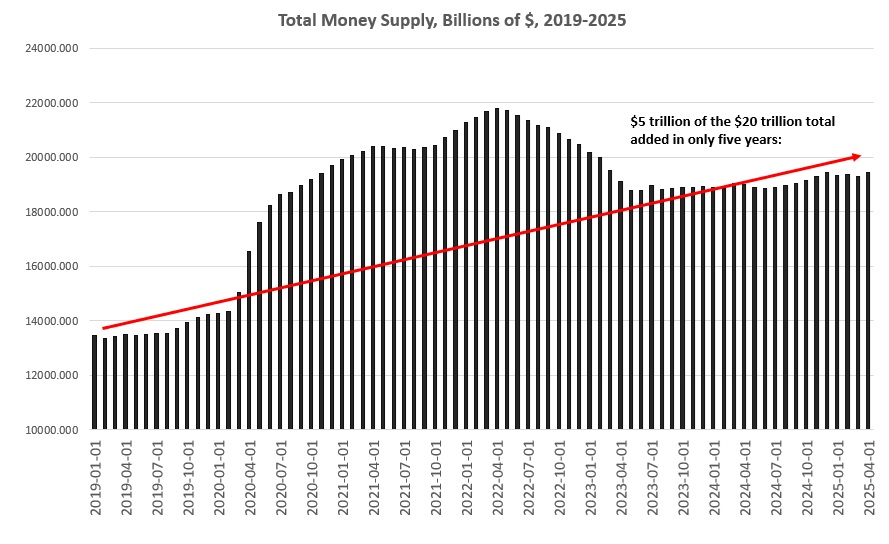

If we wish to find the real cause of general price inflation, we need look no further than the monetary inflation that continues to be baked into the US economy. The US economy is still dogged by the more-than-five-trillion dollars that was created as a result of the Fed’s covid-era inflationist policies. This massive infusion of new money will continue to show up in unpredictable ways.

Notably, the bond markets today have signaled that bond investors are not convinced that price inflation is “solved,” regardless of what the Trump administration might claim. Noting that price inflation is likely to persist into the foreseeable future, longer bond yields surged in the wake of the CPI inflation report’s release, with the 30-year yield surging to over five percent by midday on Tuesday. The ten-year yield—which is key in setting mortgage rates—responded to the CPI report by rising from 4.4 percent to 4.48 percent.

According to MarketWatch today:

The U.S. bond market was in the process of selling off on Tuesday in a manner that tends to spell fresh trouble for many stock investors.

The selloff in Treasurys sent the yield on the 30-year bond above 5% and on its way toward its highest closing level since May. Back in May, the 30-year yield’s rise above 5% was accompanied by worries about the U.S.’s fiscal outlook. By contrast, Tuesday’s moves were largely about the outlook for inflation after June data showed consumer prices rose by the most on a monthly basis since the beginning of the year.

Courtesy of Mises.org

********