Race to Debase

The ‘race to debase’ is on and the majority of nations are now involved in competitive currency devaluations. For instance, in addition to America, Euro zone and Switzerland, even Japan has now affirmed that it wants to weaken its currency. Furthermore, almost every country in the developing world is also expanding its monetary stock. Consequently, the world is being flooded with currency units and unless the monetary system changes, it is likely that this policy will continue.

Simple economics states that if you increase the supply of any item, its value diminishes. Thus, it should come as no surprise, that the increasing quantity of money is reducing its purchasing power.

It is notable that over the past decade, money lost considerable value against commodities, whereas it more or less maintained its value against stocks. However, we suspect that over the following years, money will lose tremendous value against stocks and it may hold its own against commodities.

If you review 200 years of financial history, you will realise that stocks and commodities are inversely correlated and a boom in one asset-class usually coincides with a slump in the other. So, if our assessment is correct, contrary to the recent experience, the next decade will bring about a boom in stocks and a bear-market in hard assets.

Figure 1 captures the performance of the Reuters-CRB (CCI) Index (left panel) and the S&P500 Index (right panel) since the turn of the millennium. As you can see, the CCI Index has appreciated significantly over the past 13 years, whereas the S&P500 Index has remained in a sideways trading range. Now, if our world-view is valid, this trend may now reverse and the next decade could coincide with a serious boom in American stocks and a disappointing era for commodities.

Figure 1: Commodities and stocks are inversely correlated

Source: www.stockcharts.com

Today, most investors and market commentators remain optimistic about commodities and many are convinced that this asset-class will continue to shine. However, a closer inspection of the fundamentals indicates that the primary driver of the commodities boom (supply and demand imbalance) is no longer present and it may take several years for demand to catch up.

After all, the housing bust in the West seriously dented the aggregate demand for commodities and it may be a while before consumption collides against available output. In the meantime, the world will have to deal with the increased commodities’ supply which was brought online due to record prices. Thus, if there is ample production and not enough demand, it is reasonable to assume that the prices of commodities will struggle to appreciate anytime soon.

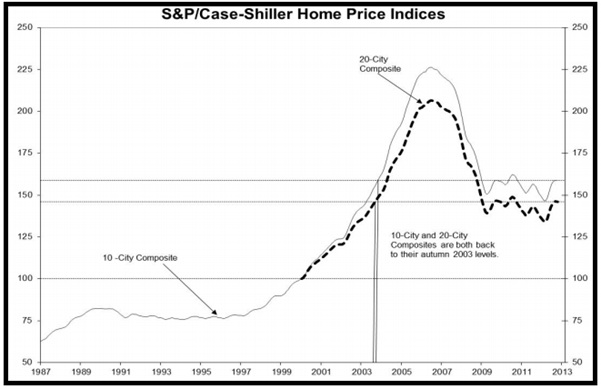

Turning to the stock market, it is worth noting that this asset-class has disappointed investors for 13 years and over that time frame, we have experienced two significant bear markets. Today, investor sentiment towards stocks remains extremely pessimistic and data confirms that the masses continue to withdraw capital from equity mutual funds. Furthermore, after declining for 6 years, the American housing market seems to be bottoming out (Figure 2) and this is a major plus for the world’s largest economy. Therefore, given the improving fundamentals, length of the secular bear-market (13 years) and today’s negative investor sentiment, it is conceivable that Wall Street may be on the verge of a historic secular uptrend.

Figure 2: Is the US housing market bottoming out?

Source: Standard & Poor’s

Source: Standard & Poor’s

Now, we are aware that some of our readers may disagree with our view. After all, the West is swimming in debt, deficits are spiraling out of control and unemployment is very high. Nonetheless, we are of the view that all these well known facts may have already been discounted by the market.

Whether you like it or not, the truth is that the Federal Reserve is cleaning out the banks’ balance-sheets via its QE program, Mr. Draghi has already pledged to save the single currency and the troubled European nations are being bailed out. Over in Asia, policymakers in both China and Japan are stimulating their economy and even the Indian government has unleashed economic reforms. Thus, at least for now, the policymakers have succeeded in temporarily dealing with some of the major economic issues.

In addition to policy intervention, monetary policy remains extremely accommodative in most nations and as long as this is the case, stocks should continue to appreciate in value.

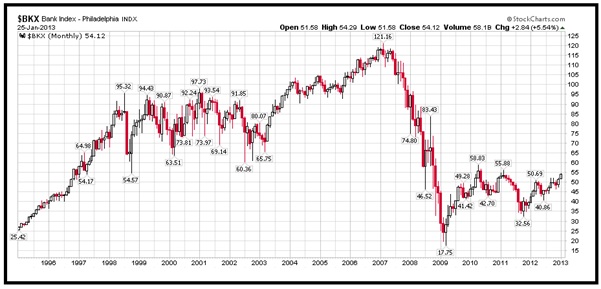

In terms of specific sectors, it is interesting to note that whereas commodities outperformed in the previous cycle, financials and housing related stocks have now emerged as the leaders. Bearing in mind the fact that America’s central bank is bailing out the financial institutions, the recent outperformance in the banks is hardly surprising.

Figure 3 confirms that the Philadelphia Bank Index has appreciated nicely since its mid-2011 low and it has now climbed above its previous high which was recorded last year. More importantly, despite the ongoing advance, this index is still significantly lower than its all-time high. In our opinion, it is only a matter of time before the Philadelphia Bank Index returns to its all-time high, thus investors should consider allocating capital to this sector.

For our part, for the first time in years, we have invested some capital in the leading financial stocks and it is our firm belief that these positions will produce good growth over the following months. We are sure you will agree that the banking industry is not about to run out of style and as long as this is the case, we will see a recovery in this depressed sector.

Figure 3: Philadelphia Bank Index

Source: www.stockcharts.com

Source: www.stockcharts.com

Currently, many of the prominent banks are trading below their book values, but we do not expect this situation to continue for much longer. As we have stated previously, the Federal Reserve is effectively cleaning out the banks’ balance-sheets and this should have a positive impact on investors’ perception. Thus, we believe that the major financial stocks look attractive and they may provide excellent returns!

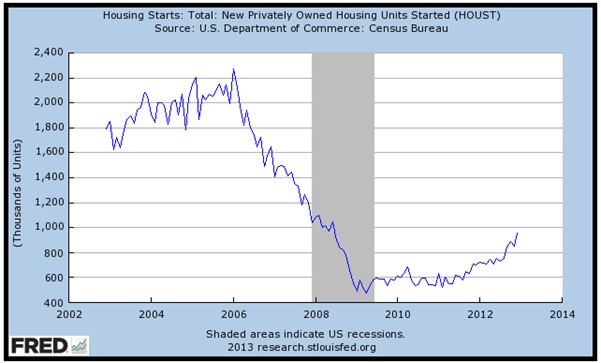

Elsewhere, housing related stocks are performing exceptionally well and our equity portfolio is heavily invested in home improvement retailers, paint companies and building materials stocks. It is our contention that coming out of the recent bust, the housing sector offers a tremendous investment opportunity.

In case you are sceptical, you may want to review Figure 4 which confirms that after falling off the edge of a cliff, housing starts bottomed out in 2008 and the recovery is now gaining momentum. In our view, this is a very big deal and further progress in this sector will bode well for the profitability of the associated companies.

Figure 4: US Housing Starts

Source: St. Louis Fed

Source: St. Louis Fed

In addition to the financials and housing related stocks, biotechnology and healthcare are performing well and we expect these sectors to provide solid long-term growth. Remember, these sectors have just broken out of a decade-long trading range and it is possible that the advance may now continue for several years.

Last but not least, the oil services stocks and industrials have recently sprung back to life and some capital can be allocated to these sectors. We have recently invested approximately 10% of our equity portfolio in this area and as long as the uptrend prevails, we will continue to hold these positions.

In summary, as long as central banks remain accommodative and policymakers pursue pro-growth policies, the uptrend in global stocks will probably continue. At this stage, we do not know when the party will end. However, we are monitoring the US unemployment rate closely as a sharp decline here will prompt the Federal Reserve to tighten monetary policy. When Mr. Bernanke ends the ‘stimulus’ and increases the Fed Funds Rates, stocks and high yield bonds will depreciate in value. Fortunately, it appears as though it will take several months before the Federal Reserve reigns in its ‘stimulus’.

Puru Saxena publishes Money Matters, a monthly economic report, which highlights extraordinary investment opportunities in all major markets. In addition to the monthly report, subscribers also receive "Weekly Updates" covering the recent market action. Money Matters is available by subscription from www.purusaxena.com.

Puru Saxena

Website - www.purusaxena.com

Puru Saxena is the founder of Puru Saxena Wealth Management, his Hong Kong based firm which manages investment portfolios for individuals and corporate clients. He is a highly showcased investment manager and a regular guest on CNN, BBC World, CNBC, Bloomberg, NDTV and various radio programs.

Copyright © 2005-2012 Puru Saxena Limited. All rights reserved.

Puru Saxena is the founder of Puru Saxena Wealth Management, his Hong Kong based firm which manages investment portfolios for individuals and corporate clients. He is a highly showcased investment manager and a regular guest on CNN, BBC World, CNBC, Bloomberg, NDTV and various radio programs.

Puru Saxena is the founder of Puru Saxena Wealth Management, his Hong Kong based firm which manages investment portfolios for individuals and corporate clients. He is a highly showcased investment manager and a regular guest on CNN, BBC World, CNBC, Bloomberg, NDTV and various radio programs.

More from Gold-Eagle