Reflections On The US Election And Gold Implications

In years to come," says Deutsche Bank's Jim Reid, "markets may well look back at the month just passed as one of the most pivotal in recent memory." The natural follow-up question might be "What exactly are we pivoting to?" Opinions abound on that score and below we have assembled a baker's dozen of what we consider the most insightful for your consideration. As always, we give special attention to the gold market.

"It is too easy, and too comforting, to blame Alan Greenspan’s supposed intellectual errors for the 2008 crisis—to imagine that, just because we have learned to speak the language of market overshoots and balance-sheet recessions, we have inoculated ourselves from a repeat of the meltdown. Unfortunately, the origins of the crisis lay not in the maestro’s failure of understanding — which would be easy to correct. Rather, it lay in the failure of our

–– Sebastian Mallaby, author of "The Man Who Knew – The Life and Times of Alan Greenspan" (Financial Times business book of the year) politics. Who in this electoral season would bet that we are safer now?"

"The bar was so low on Trump to the point people were expecting markets will go down 80 percent and global depression - and now this guy is the Wizard of Oz and so expectations are high. There's no magic here. . . There is going to be a buyer's remorse period. The dollar is going to go down, yields have peaked and will move sideways, stocks have peaked as well and gold is going to go up in the short term."

–– Jeff Gundlach, Doubline Capital

Editor's Note: Gundlach gets investor attention because of his consistent record of calling major turns in market sentiment. He called the Trump victory all the way back in January, 2015 and predicted the upturn in bond yields early on.

"The market is banking on the idea that the Trump presidency is going to be a giant reflation trade: A bet on higher equity prices, rising interest rates and a stronger dollar. The expectation is that Trump is going to get rid of tons of regulations. He’s going to push through a massive fiscal stimulus either through tax cuts or infrastructure rebuilding or all of the above. And that is going to lead to something we haven’t seen in a decade: economic growth of 3 or maybe even 4%. That would also mean higher interest rates because the deflation mind-set is gone. That’s what the market is banking on, at least initially right now."

And…

"The Fed has lost control of rate hikes. The market is in control. If the market prices a rate hike in, it will happen. If the market prices it out, it won’t happen. The Fed follows the market."

–– Jim Bianco, Bianco Research

Editor's Note: Mr. Bianco is highly regarded among institutional investors.

"President-elect Trump is in effect advocating a substantial fiscal stimulus to the economy. The difference between monetary stimulus and fiscal stimulus is found in price inflation. Simply put, monetary stimulus tends to inflate asset prices, while fiscal stimulus tends to inflate consumer prices. Therefore, fiscal stimulus leads with greater certainty to rising interest rates and bond yields, because of the price inflation effect, inflicting painful losses for banks invested in bonds. . .

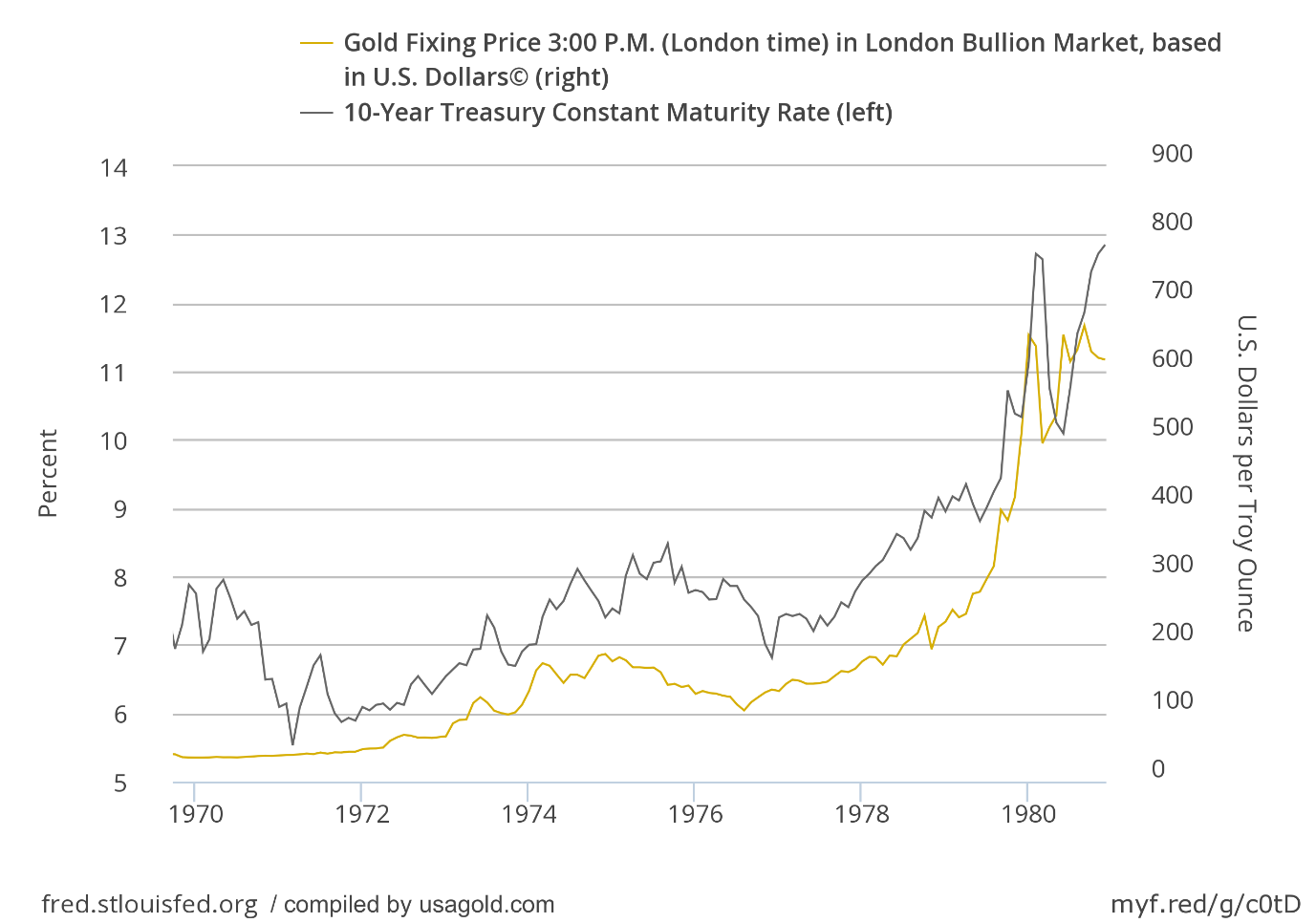

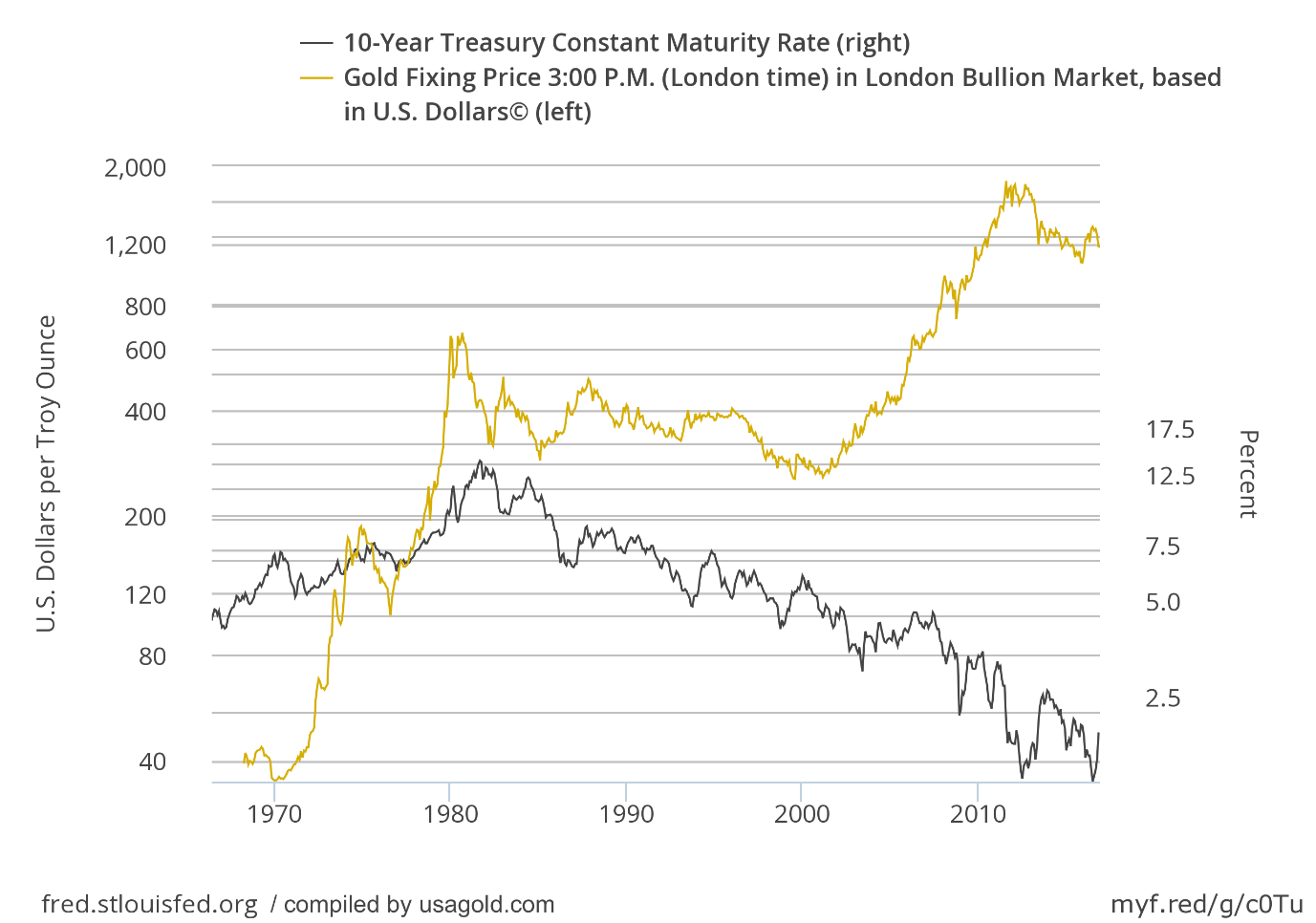

"Gold rose from $35 to $197.50 between 1970 and the end of 1974, an increase of more than four times. During that period, as mentioned above, the Bank of England’s base rate rose from 5% to 13%. The Fed’s discount rate was 4.5% in 1972 and rose to 8% in August 1974. So, a rising gold price was accompanied by a rising interest rate, contradicting the conventional wisdom of today. Gold went on to hit a peak price of $850 at the afternoon fix of 21 January 1980, when the Fed’s discount rate was at an elevated 12%. The current belief that rising interest rates are bad for gold was disproved by those events. The reason gold rose had little to do with interest rates, and everything to do with accelerating price inflation."

–– Alistair Macleod, GoldMoney

“Gold and Silver are as they were; a diversification of monetary risk. There will be a proper rally. It will be slow and orderly. We personally do not want volatility to the upside. Let it sleep and slowly climb without funds piling in it prematurely. . . Precious metals will enjoy the rally they are owed. Inflation is already here in all but name.”

Also, on future Fed policy:

"We think most importantly, the Fed is a 'chaser', or reactor to things. Not a pre-emptor. A big reason for that is job security. It will chase inflation up just as it has chased deflation down. It will react in half measures to be careful. The most important thing from here is this: Real Rates will likely remain negative for a protracted period of time acting as a reason to own stocks, and later on, Gold. Only after things have gotten away from the Fed will someone come in and really put the brakes on inflation. Volcker 2.0 is our guess."

–– Soren K., Market Slant

Editor's Note: The piece from which these quotes were extracted is billed "as a collaborative piece between several Traders and Bankers."

"On a technical basis, the music is playing, there are no negative signals and people are dancing. It's career suicide if you are not in the market."

–– Vinny Catalano, Blue Marble Capital

Editor's Note: Many of you will recall a similar quote from CitiGroup's Chuck Prince in 2007, just before the financial collapse. "When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing." Catalano's comments were with reference to the stock market advance following the Trump election victory.

"Joking aside, 'president Trump' means that the rug is about to be pulled from under the fake economy."

–– Tyler Durden, Zero Hedge

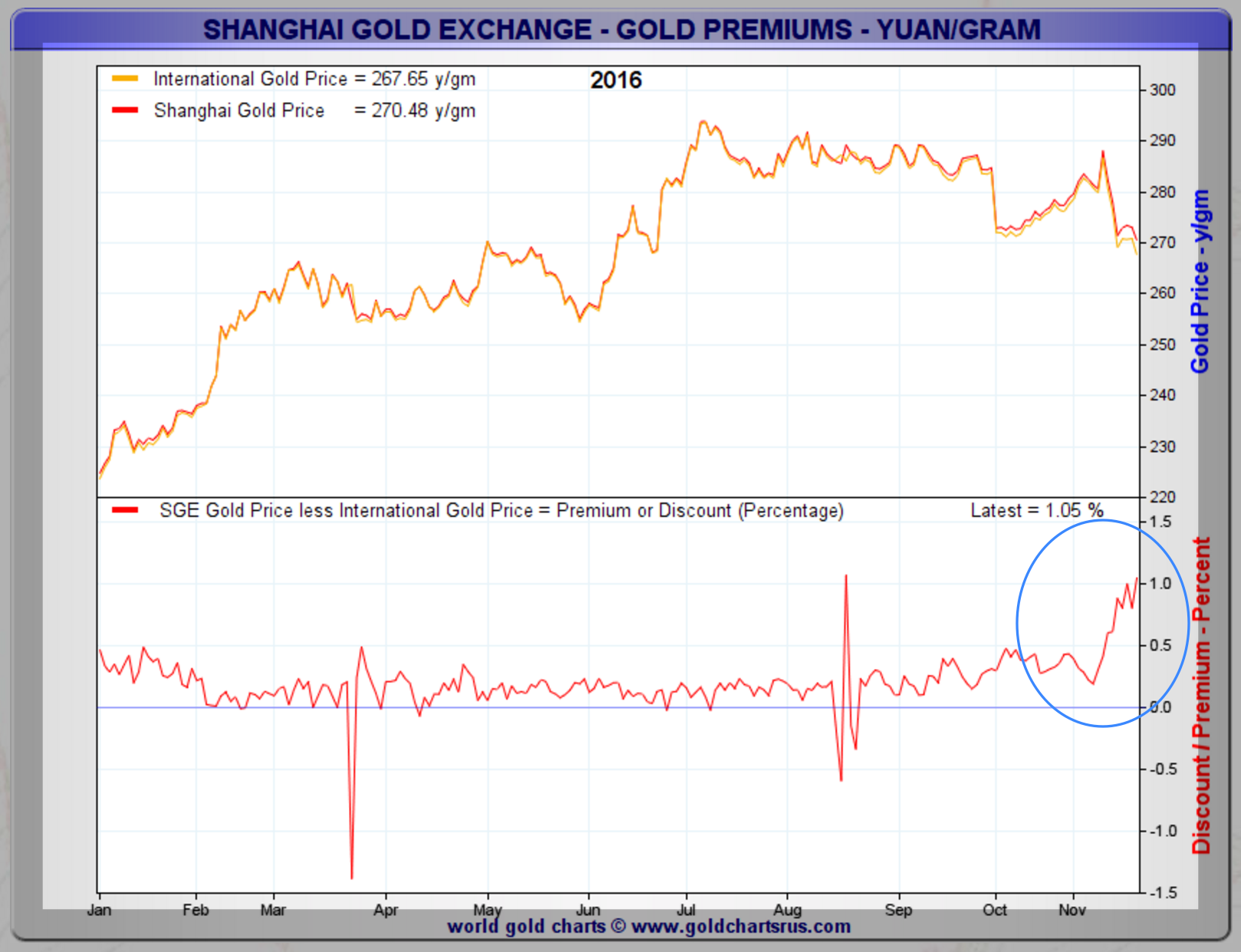

"The last day of November saw the Shanghai Gold Exchange deliver over 28 tonnes of gold - the largest amount in almost a year. Chinese gold premiums have also crossed the 1% level over international gold prices. This is showing strong physical gold demand in China which is what gold investors are waiting for. We think the bearish bias with speculators is creating an asymmetric trade in gold and any one of the upcoming catalysts could move gold higher quite fast. While gold investors close the books on the worst month for gold since 2013, something very interesting happened over in the Chinese market. Chinese buyers stepped up and bought the most gold in months."

Editor's Note: The uptick in Chinese gold demand is directly attributed to depreciation in the yuan. The yuan was weak before the Trump election victory. It is even weaker in the aftermath. Premiums on gold are rising in China suggesting a split with the rest of the global market on the real price of gold."The last day of November saw the Shanghai Gold Exchange deliver over 28 tonnes of gold - the largest amount in almost a year. Chinese gold premiums have also crossed the 1% level over international gold prices. This is showing strong physical gold demand in China which is what gold investors are waiting for. We think the bearish bias with speculators is creating an asymmetric trade in gold and any one of the upcoming catalysts could move gold higher quite fast. While gold investors close the books on the worst month for gold since 2013, something very interesting happened over in the Chinese market. Chinese buyers stepped up and bought the most gold in months."

"Gold has always been touted as a hedge against inflation. If Trump's policies increase inflation, gold is a winner. If President Trump implements his trade protectionist policies, it is likely to lead to a global economic and geopolitical turmoil, which will be even better for the buyers of gold. So, whichever way you look at it, gold will benefit its buyers. . ."

And…

"The speculators had accumulated short-term positions in gold, expecting a Brexit type rally if Trump were to be elected. However, when that hasn't happened, they are in a hurry to close their positions, which has exacerbated the fall. Once these positions are cleared, the stronger hands are likely to step up their purchases because gold is available on a ‘SALE'. We expect these prices to be the lowest in our lifetimes. Hence, be ready to buy gold in large quantities for the long-term."

–– Chris Vermeulen, AlgoTrades System

"The surprising win by Trump has triggered frenzied repositioning across asset classes. Jumping to conclusions, investors seem to have been caught up in a highly speculative and emotional game of musical chairs. If only the future were so easy to divine! The prevailing snap macro-wisdom seems based more on the perceived certainty that Obama-Clinton was a road to ruin rather than any knowledge whatsoever of the realities of the future world of Trump. If consensus analysis were such a reliable approach, how does one explain the massive capital losses that followed the dot-com bubble or the 2008 credit meltdown? It has been our experience that when markets are convinced of a certain outcome, the bell is ringing to get out of the pool

And…

'In our view, the systemic risks that existed prior to the presidential election have not suddenly vanished. Most important among these is a massive bond-market bubble. Close behind, equity valuations remain at historically extreme levels. How the new administration deals with these vexing issues, assuming that it even begins to comprehend them, is a complete unknown. Any unwinding promises to be precarious, full of pitfalls and setbacks, all of which are reason enough to hedge bets on a trouble-free return to robust economic growth with exposure to gold and precious-metals equities."

–– John Hathaway, Tocqueville

"We need to put this [global economic inequality] alongside the financial crash, which brought home to people that a very few individuals working in the financial sector can accrue huge rewards and that the rest of us underwrite that success and pick up the bill when their greed leads us astray. So taken together we are living in a world of widening, not diminishing, financial inequality, in which many people can see not just their standard of living, but their ability to earn a living at all, disappearing. It is no wonder then that they are searching for a new deal, which Trump and Brexit might have appeared to represent."

–– Stephen Hawking, Cambridge University

"The good news starts with US growth, which will almost surely accelerate well above the 2.2% average annual rate during President Barack Obama’s second term. This is because the Republican aversion to public spending and debt applies only when a Democrat like Obama occupies the White House. With a Republican president, the party has always been glad to boost public spending and relax debt limits, as it was under Presidents Ronald Reagan and George W. Bush.

Thus, Trump will be able to implement the Keynesian fiscal stimulus that Obama often proposed but was unable to deliver. The resulting deficits may be described as 'supply-side economics,' rather than Keynesian stimulus, but the effect will be the same: growth and inflation will both increase. As the US economy runs into the limits of full employment, additional growth will push inflation higher, but that bad news can wait until 2018 and beyond."

–– Anatole Kaletsky, Gavekal Draganomics

“The key is not the S&P 500. It’s the 10-year note and 30-year bond that matter. The only thing which is way out of line is the price/earnings ratio in the bond market. And that is not an insignificant factor.”

–– Alan Greenspan, Greenspan Associates, LLC

Editor's Note: Greenspan expresses his chief concern for the present (along with the return of a 1970s-style stagflation) on the 20th anniversary of his famous remarks about "irrational exuberance" in the stock market.

This chart further supports Alasdair Macleod's point made above that gold responds favorably during periods of rising interest rates like the 1970s. It also makes the point that gold does well in a falling interest rate environment like the 2000s.

One factor often overlooked and evident on the charts is just how long we have been in a declining interest rates environment, i.e. since 1985. Too, the rising rate environment that preceded it originated in the early 1960s and lasted nearly 25 years. In other words, if we are indeed at the genesis of a new rising interest rate trend similar to the 1970s, as some are suggesting, it could last for a very long time.