The Return of Inflation and Goosing Retail Investors: Got Gold?

When it comes to financial news, stocks, bonds, interest rates and inflation are some of the topics that garner headlines, but it’s consumer spending that matters most.

The amount that Mr. and Mrs. Consumer spend represents close to 70% of US Gross Domestic Product (GDP). It’s around the same level globally.

Economists therefore keep a close eye on both consumer spending and consumer sentiment to see which direction a country’s economy and the global economy are heading.

Source: Visual Capitalist

A stagflationary environment is one where economic growth is decelerating, and inflation remains high.

Is the US on a road leading to stagflation and recession? Tariffs are inflationary. Decelerating growth means job losses. While US GDP grew by 3% in the second quarter, against -0.5% in Q1, the outlook is weak.

Trading Economics predicts US GDP growth will be at just 1% by the end of this (Q3) quarter, and it is projected to trend around 2% in 2026, according to econometric models.

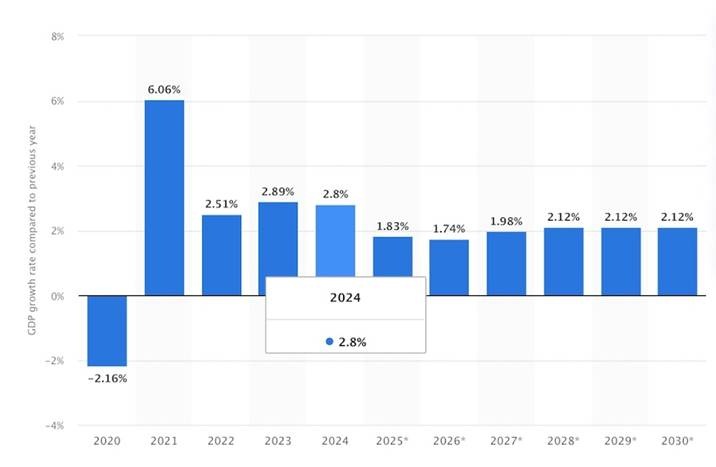

A Statista chart shows annual GDP growth of just 1.83% in 2025 and 1.74% in 2026, versus 2.8% in 2024 and 6.06% in 2021.

Real US GDP growth rate, 2020-30. Source: Statista

Private-sector investment in the second quarter plunged 15.6%. Inventories dropped 3.2% and non-durable goods manufacturing slowed to 1.3%, down from 2.3% in the first quarter. (Al Jazeera)

The July jobs report was the worst since the pandemic and the hiring rate was just 3.3% in June, well below the pre-covid average of 3.9%.

At AOTH we believe the US is on the road to stagflation.

Precious metals gold and silver will ultimately become the last safe haven standing after the stock market bubble pops, bond yields spike, the dollar plummets, and generalized economic fear takes over.

Video — The looming threat is stagflation: The new reality for the US economy

The return of inflation

US producer prices increased by the most in three years in July amid a surge in the costs of goods and services, suggesting a broad pickup in inflation was imminent, Reuters reported on Thursday.

If that happens, it will jeopardize an expected (though not by us at AOTH) interest rate cut from the Federal Reserve in September.

“This is a kick in the teeth for anyone who thought that tariffs would not impact domestic prices in the United States economy,” Reuters quoted Carl Weinberg, chief economist at High Frequency Economics.

Bloomberg agreed that companies are starting to pass on higher input costs to their customers after months of “eating them”. The higher costs are weighing on corporate earnings, putting shareholder pressure on firms to maintain profit margins and “pass through” the tariffs.

The Producer Price Index (PPI) rose 0.9% from June, the largest advance since consumer inflation peaked in June 2022, said a report by the Bureau of Labor Statistics (BLS). It climbed 3.3% from a year ago.

“New tariffs are continuing to generate cost pressures in the supply chain, which consumers will shoulder soon,” Samuel Tombs, chief US economist at Pantheon Macroeconomics, wrote after the BLS report, via BBC News.

“While businesses have assumed the majority of tariff costs increases so far, margins are being increasingly squeezed by higher costs for imported goods,” Ben Ayers, senior economist at Nationwide, said in a note. “We expect a stronger pass through of levies into consumers prices in coming months with inflation likely to climb modestly over the second half of 2025.”

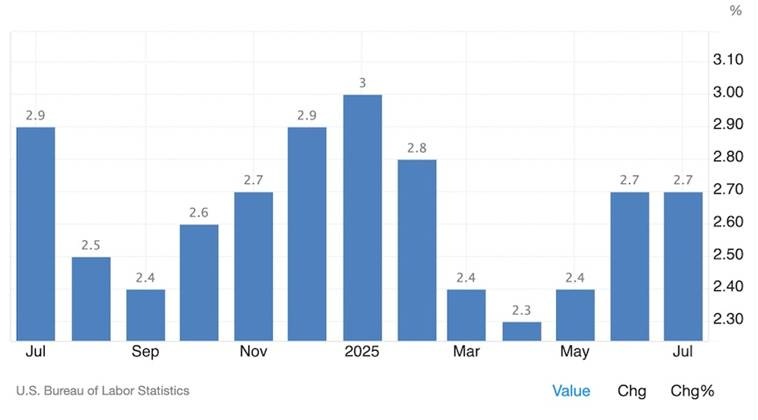

US inflation. Source: Trading Economics

As for the PCE price index, the Fed’s preferred measure of inflation, it’s also going up — +0.28% in June compared to 0.17% in May and 0.16% in April. Durable goods are up 0.47% compared to near zero in May and April. Food purchased at stores was 0.26% more expensive in June compared to +0.17% in May.

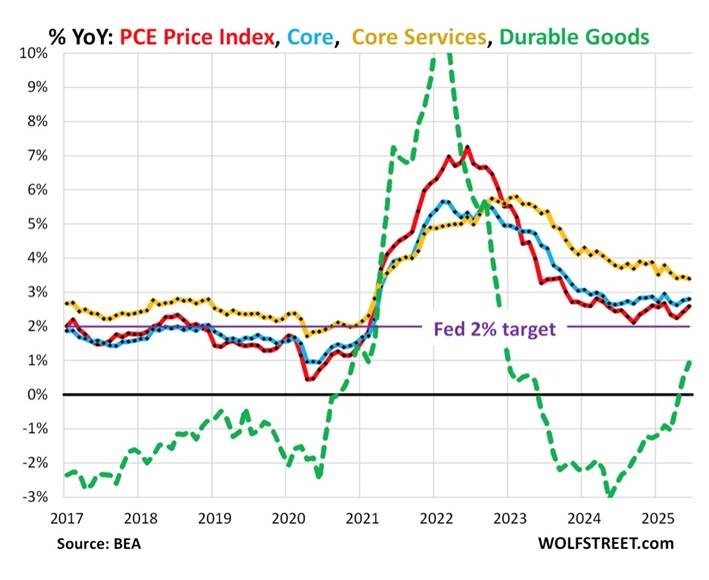

The annual rates are more concerning, as plotted in the chart below. The overall PCE price index, the red line, was +2.6% in June, and the core PCE (goods and services minus food and fuel) in blue was +2.8%.

Wolf Street notes The core services PCE index, at +3.4% (yellow) for the third month in a row, is substantially hotter than in the pre-pandemic years and the biggie that keeps core PCE and overall PCE well above the Fed’s target.

Source: Wolf Street

Consumers, naturally, won’t be happy.

Barron’s reported recently that inflation was their biggest worry this year and last year:

In Numerator’s monthly consumer sentiment survey of approximately 2,000 representative households last year, consumers listed “rising prices” as their main concern—ahead of unemployment, potential recession, crime, or immigration. They say the same thing even now, even as inflation slows to below 3% year-over-year.

The publication notes tariffs haven’t shown up meaningfully in consumer prices yet but warns they’re coming. The reason for the delay is that existing contracts prevent higher costs from immediately being passed onto consumers. It’s also difficult for businesses to set a price increase, when Trump keeping changing the tariff rates. One thing is for certain, Barron’s states: as these contracts come up for renewal, suppliers and manufacturers negotiate higher prices, and consumers start paying more at checkout.

Packaging giant Procter & Gamble let its retailer customers know on July 29 that they would have to raise prices on goods like paper towel and detergent, starting the following week. About a quarter of P&G’s products will get more expensive to help offset the cost of new tariffs. Swatch, the watch maker, hiked prices 5%.

Reuters notes that, while US stock indexes have reached record highs this year, mainly on the strength of technology stocks, many consumer bellwethers have struggled. Since Trump’s April 2 tariff announcements, P&G shares have declined 19%, Kimberly-Clark is down 11%, and PepsiCo is off nearly 7%, compared to the S&P 500’s more than 13% gain (figures as of July 29).

Between July 16 and 25, companies in the Reuters global tariff tracker said they expected to lose a combined $7.1 billion to $8.3 billion for the full year.

“Main Street has yet to see the fallout from increased tariffs — and they’re going to go higher,” said Bill George, former chairman and CEO of Medtronic and executive education fellow at Harvard Business School.

According to a Bloomberg opinion piece, the Budget Lab at Yale estimates the levies so far will reduce annual GDP by $115 billion and result in an average per household income loss of $2,400.

The same Budget Lab was quoted by The BBC estimating that, as of Aug. 7, the average effective tariff was 18.6%, the highest since 1933. The average tariff before Trump took office for a second time was 2.4%.

The publication noted that, while the tariffs in June brought in $28 billion in revenues — triple the monthly revenues seen in 2024 — and the Congressional Budget Office (CBO) estimates that new US tariffs would reduce US government borrowing over the next 10 years by $2.5 trillion, the CBO also said the tariffs would shrink the size of the US economy and that additional revenues generated by the tariffs would be more than offset by revenue lost by Trump’s tax cuts.

More than 70 economists surveyed by Bloomberg now see GDP expanding by just 1.5% this year, and by only 1.6% in 2026 — similar to the Trading Economics and Statista forecasts cited above.

Moreover, the 12-month outlook for inflation among bond traders has more than doubled since last September to around 3.4%, compared to the current 2.7% and significantly higher than the Fed’s 2% inflation target.

Consumer spending takes a hit

It’s clear that US consumers are sick of inflation, even as more is yet to come, and they’re taking it out on retailers by spending less.

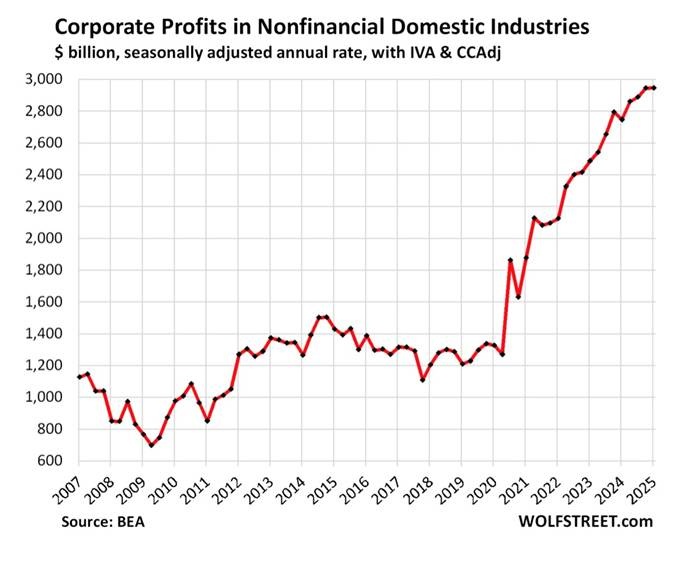

Wolf Street has some interesting observations about retailers raising prices, or not. Wolf Richter takes us back to 2021-22, when companies jacked up prices and sales didn’t plunge because consumers were in good financial shape due to the covid-19 stimulus checks.

For an illustration of the ensuing explosion in corporate profits, see the chart below:

Source: Wolf Street

By mid-2022 consumers were fed up with the price increases and started shopping for deals. Companies responded by slashing prices. The price cutting faded in early 2024 when consumers grew tolerant of increases again.

Fast forward to the current state of affairs, and the picture is mixed:

Some retailers have recently raised prices on some of their products, and some got away with it, and some didn’t and got hit by sales declines.

Long-term though, this can’t continue. If tariffs stay in place, companies will have no choice but to pass on the higher costs to their customers or risk the wrath of shareholders.

Remember what was said at the top of this article: consumers are 70% of the US economy — they matter.

Consumer spending increased by a soft 0.5% in the first quarter and a not-much-better 1.4% in Q2. Adding them together gives the worst six-month stretch of spending since the last half of 2022.

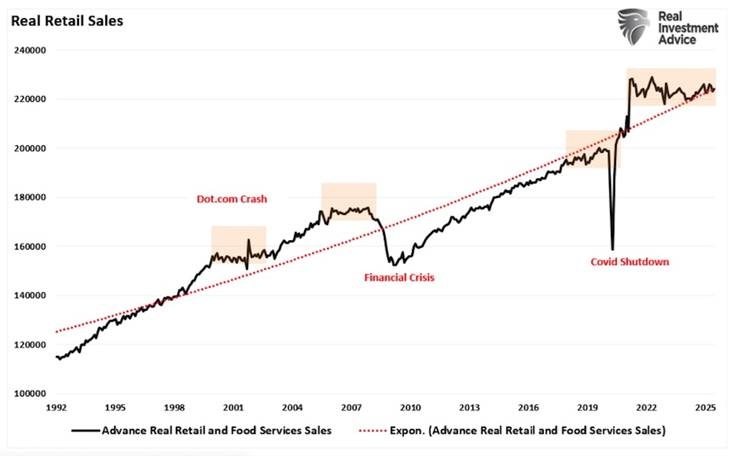

Real Investment Advice headlines that ‘Retail Data Sends A Warning’:

While Yahoo may not have found any signs of “rot” with the consumer, it is there if you want to look. The recent retail data showed an increase of 0.6% on a nominal basis, but real, inflation-adjusted retail sales data have remained flat since the stimulus-induced spending frenzy in 2021. Notably, previous periods of stagnant retail sales occurred before or during recessionary periods…

Source: Real Investment Advice

the weakening of retail data regarding the market raises concerns, given that corporate earnings come from consumer spending.

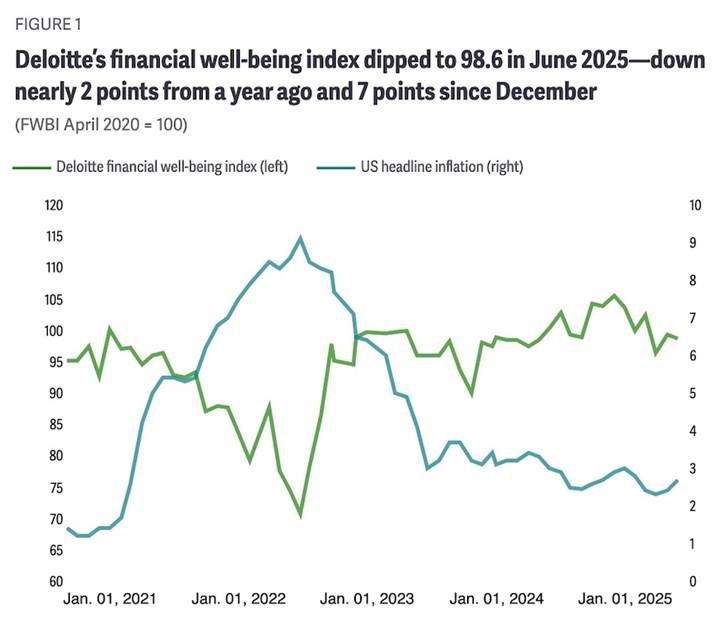

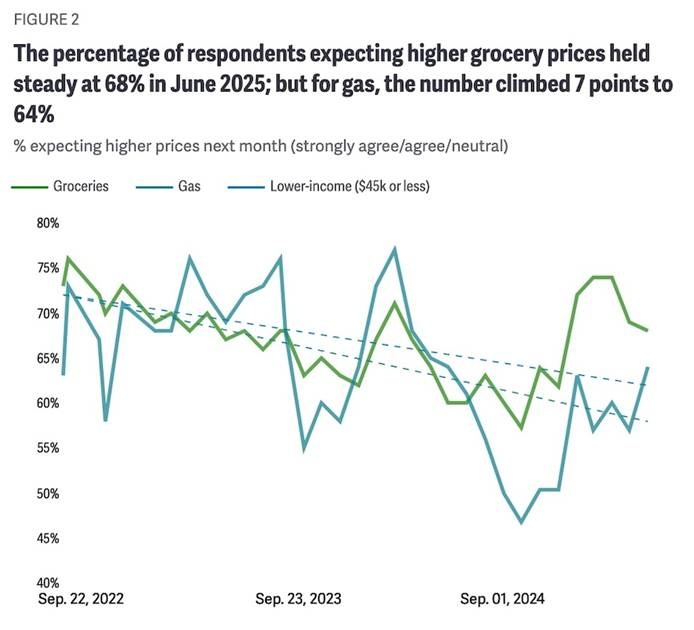

Deloitte’s recent financial well-being index shows consumer’s well-being on a steady downward slide since December 2024. The firm’s ‘State of the US consumer: July 2025’ also says consumers remain braced for higher prices, with grocery inflation expectations remaining elevated, and gas inflation expectations rising.

Source: Deloitte

Source: Deloitte

Source: Deloitte

Goosing retail investors

Consumers may be getting more price-sensitive, but they are also growing more risk-tolerant when it comes to buying stocks.

The first thing to notice is that retail buyers are becoming a larger part of the total pool of investors. According to Goldman Sachs analysts, retail investor participation as a share of total S&P 500 flow during the third week of July reached 12.63%, the highest since February.

Their participation has rarely exceeded 13% in the last few years, Reuters reported on July 29.

In fact, according to Barclays Bank strategists, retail investors have been the primary driver of the current rally, pouring more than $50 billion into global stocks during the month of July.

“Re-risking seems to be the priority for small investors as improved sentiment into 2Q25 earnings, resilient macro data and Fed cut speculation combine to outweigh still-lingering tariff threats and deficit concerns,” the strategists wrote.

Not only is retail more numerous, but they are also optimistic. In Morgan Stanley’s latest quarterly survey, 62% are now bullish US equities, and two-thirds think the US market will rise by the end of the quarter.

Fears of a market correction are not unwarranted, says Reuters, given the latest figures from the Financial Industry Regulatory Authority (FINRA), which show that margin debt in US stocks has crossed the $1 trillion mark for the first time.

This refers to investors borrowing “on margin” to buy stocks they can’t afford to pay for with investment capital.

The risk these investors are allowed to take is about to get a whole lot greater, thanks to a change to an obscure trading rule, and changes to the rules around investing in private equity.

Reuters reports the Trump administration is drawing up an executive order to allow retail investors to add private equity into 401(k) retirement funds. Media reports also suggest FINRA is considering proposals to ease the “Pattern Day Trading Rule” — which was set up to limit highly speculative trading practices — by slashing investors’ minimum margin account balance requirements to $2,000 from $25,000 currently.

Some comment on each of these regulatory changes is warranted.

Up to now, retail investors have largely been excluded from opportunities available in private markets.

Bloomberg said Robinhood Markets is now offering tokens to European clients that would effectively give them exposure to private companies such as OpenAI. Last month JP Morgan and Citigroup said they’re adding research on private companies in sectors such as artificial intelligence and aerospace. “Surging valuations among such companies have been triggering a surge in retail interest,” Bloomberg writes.

Yet there’s a catch — private equity is risky. It turns out, much riskier than playing in the public-markets pool. Bloomberg states:

Private equity-owned companies drove an increase in defaults and continue to turn to distressed debt exchanges after credit conditions deteriorated in the wake of US tariff announcements, according to Moody’s Ratings.

In the three months through June, 21 companies defaulted on more than $27 billion of debt, the firm said in a Tuesday report. That’s up from the 15 companies that defaulted on about $15 billion of debt in the prior quarter.

As for the reduction in minimum margin account balance requirements to $2,000 from $25,000 currently, this is to do with “Zero Days to Expiration” (0DTE) options, which are option contracts that exist for a single trading session and expire on the same day that they are traded. A recent Wall Street Journal article highlighted how 0DTEs have exploded in popularity. According to Real Investment Advice it’s a glaring example of risk-taking behavior, and history consistently shows that markets peak when the average investor starts chasing lottery-like returns. This is a huge behavioral shift from investing to outright gambling. As a consequence, we’re in this day-trading speculative fervor that is taking over the market.

A few more indicators show that all is not well in the USA and that a reckoning may be coming that causes a major precious metals bounce.

Rising bond yields

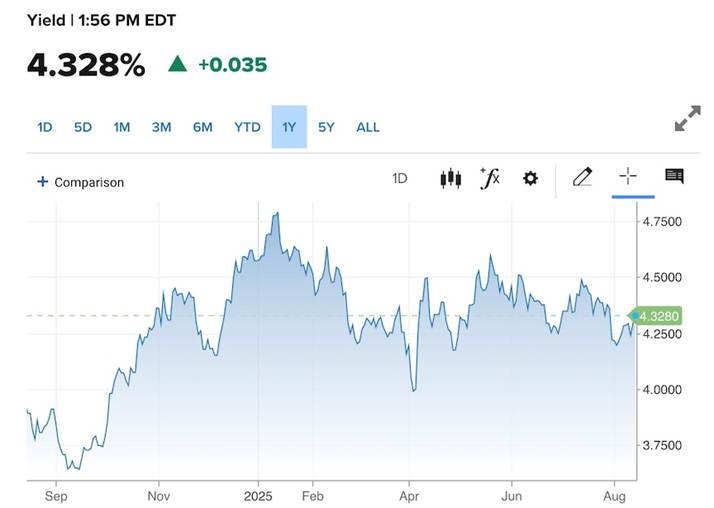

The first is rising bond yields. On Thursday US Treasury securities sold off, sending yields higher after a hotter-than-usual PPI inflation report promises to push the Fed’s preferred PCE inflation gauge higher, the Wall Street Journal reported. The benchmark 10-year yield ended the day at 4.29% versus 4.23% Wednesday. The yield ticked up to 4.32% in mid-day trading, Friday.

Source: CNBC

Reuters said in mid-July that a strong majority of bond strategists surveyed by Reuters predicting demand for Treasuries lagging an expected deluge of new supply.

Two reasons were given. One is Trump’s One Big Beautiful Bill Act, which is expected to add $3.4 trillion to America’s already massive $36.2 trillion national debt.

Then there’s Trump’s trade war. Inflation risks from it have pushed the US “term premium” higher. Term premium refers to the compensation investors demand for holding longer-term bonds:

With net Treasury issuance expected to approach nearly half a trillion dollars this quarter a rising risk premium makes it considerably harder to finance those expenses at higher interest rates.

Nearly 77% of bond strategists, 23 of 30, responding to a July 10-15 Reuters survey said demand for U.S. Treasuries would lag supply slightly both this quarter and the next.

Manufacturing slowdown

The whole idea behind the trade war is to prevent foreign companies from dumping cheaper products into the United States, incent such companies to build factories in the US, thus avoiding tariffs, and bring back American jobs that have been out-sourced abroad.

It’s a good theory, but the reality is somewhat different.

Manufacturing in the US is declining, not increasing, as a result of tariffs put in place in early April. According to Trading Economics,

The S&P Global US Manufacturing PMI was revised slightly higher to 49.8 in July 2025 from a preliminary estimate of 49.5, but it remained the lowest reading since December and continued to signal deteriorating operating conditions in the US goods-producing sector. [PMIs <50 signal a manufacturing contraction]. Demand stagnated and tariff uncertainty continued to dominate the manufacturing landscape.

The admittedly anti-Trump, leftist CBC News quoted Philip Luck, a former deputy chief economist with the US State Department, saying that the current tariff regime doesn’t make sense as a way to make industry thrive.

Trump’s strategy is “going to increase costs, it’s going to decrease U.S. competitiveness and it’s going to make us worse off,” Luck told CBC News Network on Thursday.

The article goes on to say that it isn’t outsourcing that has resulted in the loss of US manufacturing jobs, but automation and higher productivity.

Apple recently announced a $100 billion US increase in its domestic production plans, bringing the company’s promises of US investment to $600 billion US over the next four years.

The Wall Street Journal responded to the announcement by describing the manufacturing sector as “spluttering” in 2025.

“Economic activity tied to manufacturing has shrunk for most of Trump’s second term,” the Journal reported.

According to the Bureau of Labor Statistics, the sector has seen a net loss of 37,000 jobs in the three months since May, and five straight months of contraction, as per the key benchmark tracked by the Institute for Supply Management (ISM).

(Trump promptly fired the bureau’s commissioner after the latest numbers came out. The BLS is already, since Trump took office, so underfunded that they’ve cut 350 economic reports — Rick)

Terrible jobs report

In early June the Labor Department reported that the federal government has shed 59,000 jobs since January.

Just 73,000 jobs were added in July, with the monthly totals for May and June revised down by a combined 258,000 jobs (CNN).

“It’s stalling out right now,” Diane Swonk, chief economist at KPMG, said of the labor market.

With those monumental, quarter-million-job downward revisions, the meager job gains in June were the weakest since December 2020, the last time the labor market had monthly job losses. The pace of job creation seen so far this year is the weakest in decades, outside of recessions.

“This is absolutely the worst major economic report since the end of the pandemic era,” Joe Brusuelas, chief economist at RSM US, told CNN.

As mentioned, the Labor Department said the hiring rate was just 3.3% in June, which is well below the pre-covid average of about 3.9% and in line with levels generally associated with recessions.

Conclusion

With all the bad economic news we have just outlined, could there be a better time for owning precious metals?

It’s too early to proclaim stagflation in the United States but the economic indicators are certainly pointing in that direction, at AOTH we believe ‘70’s style stagflation is the least bad result of President Trump’s policies.

Economic growth at sub-2% is anemic, and it’s not supposed to get any better in 2026. Inflation is picking up as the Trump tariffs take effect. Companies’ input price increases are gradually being passed through to customers, boosting inflation gauges like the CPI, PPI and PCE.

The Fed will be watching inflation closely to see whether a September rate cut is warranted.

Consumer spending makes up nearly 70% of US GDP so the condition of the American consumer is of utmost importance.

Consumer spending increased by a soft 0.5% in the first quarter and a not-much-better 1.4% in Q2. Adding them together gives the worst six-month stretch of spending since the last half of 2022.

Despite weak manufacturing data and a stalled labor market, US stock markets continue to run hot. The Dow on Friday trimmed earlier gains to fall just short of a record close. (Yahoo Finance)

The Trump administration is changing the rules around private equity to allow more retail investors into a risky space and is reducing investors’ minimum margin account balance requirements to $2,000 from $25,000 currently. Both measures throw caution to the wind and increase the chance of a stock market meltdown.

Margin debt in US stocks has crossed the $1 trillion mark for the first time.

Lower interest rates will fuel the retail speculative gambling bubble. Trump is highly motivated to get the Fed to cut interest rates so that he doesn’t have to finance the national debt at higher rates when US Treasury bonds roll over. It looks like Trump will get his wish.

He nominated Stephen Miran, chair of the Council of Economic Advisors, to replace Adriana Kugler on the Federal Reserve Board of Governors. Fed Governor Christopher Waller, viewed as more dovish, could be Trump’s pick to lead the central bank, reinforcing expectations of easier policy. Trump could either fire Powell or wait until his term ends next May before appointing a successor more to his liking.

Gold’s real secular move has yet to even begin – Richard Mills

Whether it happens now or later, interest rate cuts will be a tailwind for precious metals. Gold is up 25% year to date, as of Friday @ 2:03 pm Pacific; silver has gained 31%.

Historically, the best leverage to rising gold and silver prices is to buy junior resource companies. The juniors haven’t yet joined the upward march in gold and silver prices, so I’ve been loading up on cheap precious metals exploration companies with experienced management teams and with great projects in safe jurisdictions.

Richard (Rick) Mills

aheadoftheherd.com

********