Shenanigans Abound

Listening to a particularly popular “weekly wrap-up” (featuring a gold perma-bull and a certain prominent billionaire’s “favourite technical analyst”) last Saturday afternoon, I was immediately struck by the reversal in the analyst’s so-called “technical picture” for gold and silver because it was only two weeks ago that “silver looks great” and “gold is biding its time” (or something like that). Instead, he now does not like the gold or silver miners and thinks both are headed lower, but that Bitcoin is headed “to $36,000 then $54,000” as part of the final blowoff in its “parabolic ascent”.

So, if I were to follow his line of reasoning, you want to take a bullish trading posture to the most speculative bubble in history while avoiding the asset class with 5,000 years of utility and history that is currently in a long-term bull market but dangerous because it is 12.29% off the all-time highs seen in August 2020.

Herein lies the difficulty in basing 100% of your investment decisions on any one form of analysis. Fundamentalists tend to ignore the predictive power of price patterns and other quantitative data that can often reveal changes in the flow of capital to and from the precious metals sector. Technicians, by contrast, tend to focus purely on short-term signals that choose to ignore fundamental changes in macroeconomic trends or in either fiscal or monetary policy by those in charge.

When both fundamental and technical analyses are blended, in a perfect world, the result is a beautiful canvas of analytical brushstrokes producing a world-class roadmap of the future direction and amplitude of a stock’s next move. However, in reality, what often results is a dog’s breakfast of conflicting signals and omens leaving the investor both confused and disillusioned.

Gold and silver mining stocks are today a textbook example of this dichotomy of portent with low input costs such as energy and cost of capital aligning with near-record pricing structures to produce profit-margin windfalls throughout the entire sector. Fundamental analysts like Fred Hickey and Pierre Lassonde are beating the “undervaluation” drums with ecumenical enthusiasm yet such fervor is being met with abject disdain by those managing large portfolios because price – the final arbiter of investment acumen – refuses to pay heed to such pulpit preaching by counters of beans.

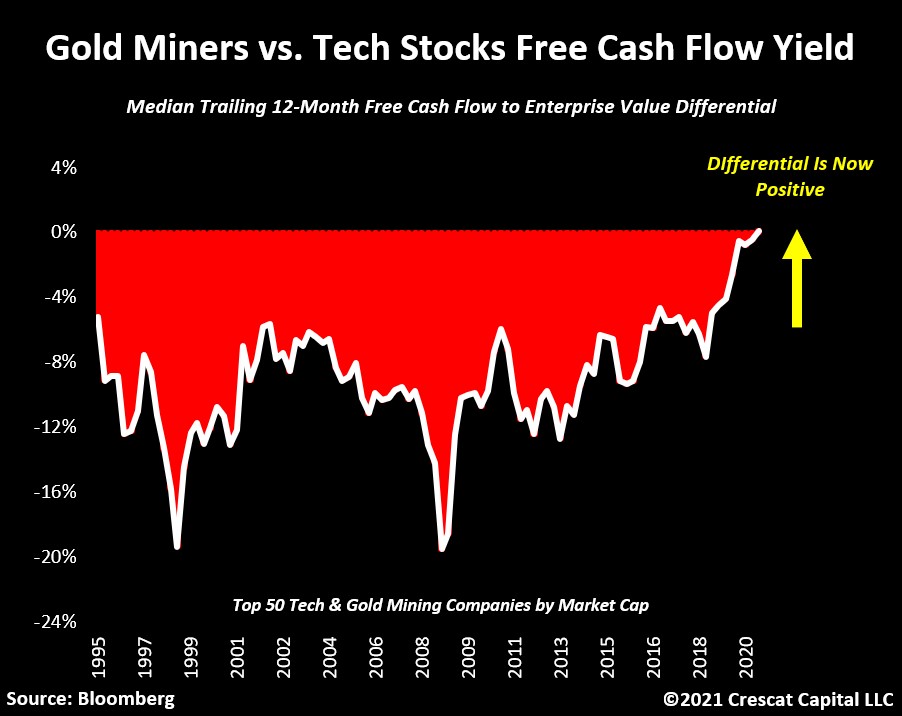

Here is a favourite graph making the rounds in the precious metals blogosphere: it is a comparison of free cash flow between the gold miners and the tech stocks. It suggests by way of inference that the legions of Gen-Z, Millennial, and Gen-X investors make their investment decisions based upon “informational tripe” such as this. For the past year and certainly since early August, stimulus cheques have been allocated to owning tech which these kiddies not only understand but also worship due to the generational obsession with all things digital.

Not having been schooled in the history of hyperinflation over the past 5,000 years, this new breed of youthful investors soar from one name to another and from sector to sector like flocks of swallows chasing insects in the swamp at dusk, large arching ascents followed by near vertical dives in hunt of their buzzing prey. I assure you; gold and silver are not on their menus.

The yellow highlighted portion in the graph above means nothing to the stewards of these large capital pools; if their social media feed like Twitter or Instagram told them to buy into asteroid mining, they would gladly re-tweet the narrative until the desired effect was achieved. A great example of this was when the Robin-Hooders took bankrupt Eastman-Kodak from $2 to $60 in a 72-hour period, only to succumb to gravity (as opposed to common sense or sanity), and crash back down to $6. Alas, 90% drawdowns are meaningless when the investor is using government handouts to play the game as opposed to four years of summer job savings or rent money.

The problem facing investors born before 1977 is that the rules of investment engagement have been altered to the point where the scales are tilted in favour of price at the detriment of value. For the older generations, gratification and reward for any endeavour was a process that took time to achieve. Mid-semester school projects involved hours at the library versus minutes on the internet while shopping for the best refrigerator took multiple store visits over weeks rather than a lunch hour online. Patience is now a lost art form while instant gratification a God-given right. Investment rewards for the younger generations involve daily tabulations of price versus monthly or yearly assessments of value – and this is precisely why we are faced with this maddening dichotomy in the gold and silver miners.

Which brings me to the point of the exercise – what will snap these markets back to the proper balance between value and price?

The answer lies in that old adage that “the best cure for high prices is high prices” because in a free market economy (remember that?), high prices attract new supply as manufacturers retool and rebrand in search of that demand which is creating those high prices. Conversely, low prices discourage new entrants to the market and force existing supplier elsewhere which eliminates excess supply after which price rebalances.

High stock prices in the technology space have persisted because the demand for them has been fueled by cheap money and government subsidies. Without subsidies, Tesla would be toast. Without the bailouts in 2008, half the global financial behemoths would be either gone or massively restructured under new ownership. If the U.S. 10-year were back at 9% as in 1994, competition for return – especially risk-adjusted return – would siphon money away from stocks and into bonds. However, government intervention has minimalized the perception of risk and made it perennially safe to invest in stocks and bonds but unsafe to speculate in gold or silver. Note the difference in terminology – invest versus speculate.

Larry Summers, Treasury Secretary under Bill Clinton, was a huge proponent of “behavioural finance”, and believed that stock price movements had a huge impact on consumer behavior. The “asymmetrical wealth effect”, defined as the impact of inflating assets such as housing and stocks upon spending habits, has long been viewed with overt reverence by the politico-banco

elite but what was once a beneficial barometer of a booming economy is now seen as the temperature of a booming economy. This is why government intervention is so ardently “pro-stocks” and “anti-gold” – because it violates the mantra long preached by the elite.

There is another competitor in the arena that is threatening to dethrone stocks and while in the last three decades it was precious metals donning the black hat of the enemy, cryptocurrencies are now the enemy. The initial line of defence has been central bank threats to launch their own digital currencies but the crypto-advocates have thus far soundly rejected any notion of that being successful. When the politico-banco criminals decide to shut down crypto, and I firmly believe that they will, those wishing to control their wealth away from the watchful, covetous eye of Big Brother will finally recognize that “possession is nine-tenths of the law” and storing wealth in a digital vault is a far cry removed from having it in your home within spitting distance of your Smith & Wesson.

For value-seekers to finally begin to dominate price-chasers, the central bank lifeline must be terminated either by the impact of high prices or by the final acceptance that stock prices are no longer impacting consumer behaviour. Once that happens, capital flows will gravitate toward value because prices no longer manipulated by the elite can no longer be trusted. When price-chasers finally become value-seekers, companies producing products cheaply while commanding high prices will increase in value until they are no longer attractive. The key will be the sheer volume of dollars, euros, yen, and renminbi migrating from price-chasing to value-seeking and when that occurs, owners of gold and silver and their equity market brethren will soar.

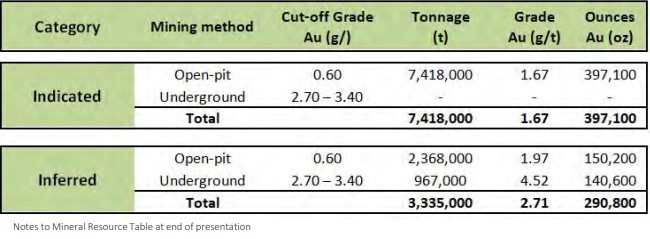

Gold and silver miners are today generating historic profits and while high prices are most certainly going to attract more supply, that supply can only arrive from the developers. As an example of the value proposition, I want to take you to the announcement last week of the “friendly” acquisition by Eldorado Gold Inc. (EGO:US) (USD $11.13) of junior explorer/developer QMX Gold Corporation (QMX:TSXV / QMXGF:U.S. OTC) (CAD $.28 / USD $/22) for the approximate sum of CAD $132 million in cash and stock.

The graphic shown above demonstrates the indicated and inferred ounces at 687,900 present in the Bonnefond Deposit located in Val D’or Quebec adjacent to the Lamaque Mine currently operated by Eldorado.

While there are numerous other discovery zones present in the QMX land package, EGO paid USD $150.63 per ounce to acquire QMX which appears quite generous at first glance but when you go through the corporate presentation for QMX, it is obvious that there are a great many more ounces situated within their property boundaries. However, it hammers home a point I have been making for the better part of a year and that is that developers such as Getchell Gold Corp. (GTCH:CSE / GGLDF:US OTC Qb) are going to viewed as equally as attractive when the scale of the mineralized envelope at Fondaway is revealed by way of the 2021 drilling program. The initial news releases referred to QMX as a “Val D’or explorer” which is why they sold off EGO on the news but this type of M&A activity is what I expect to see accelerating in 2021 and it plays favourably into the future for the GGMA portfolio which is overweight developer /explorers in expectation of this incoming tsunami of mergers and buyouts.

I do not usually make it my practice of subscribing to other newsletters but one I absolutely deem as “required reading” is anything put out by Grant Williams and that means podcasts, interviews, or his newsletter. This weekend I listened to his interview with legendary hedge fund manager, Paul Singer, who has been described as “one of the toughest and smartest in the hedge fund industry”. It was an “eye-opener” to say the least and even though I am resolute in my adherence to self-imposed investment rules, I still from time to time require a dollop of morale boosting for a number of reasons, the most important being to maintain my sanity in the face of these gargantuan dislocations in valuations which exists everywhere you run into central bank fingerprints.

At the end of the day, no amount of bullion bank shenanigans is going to alter the final replacement cost of an ounce of gold or silver when the unit of payment is a depreciating currency. Show me one currency in circulation anywhere that is practising sound money principles and I will choose it over gold or silver but the reality is that with this global pandemic still shuttering economic activity, global currency debasement is universal.

*********

More from Gold-Eagle