Stocks And Awe: The Federal Reserve Regime Change Is Here!

The Everything Bubble is bursting, and the Fed has barely even begun its war on inflation. Many top stocks are already in their own bear markets. Nvidia, way off its game, has lost 25% of its value from its last high score. The ridiculously skyrocketing Tesla has plunged back toward earth’s gravity on a trajectory that has lost 28% of its high-orbit altitude. Facebook (now transrendered as “Meta”) has done a face plant near bear territory, down 17%, as has Amazon, slithering down 16%. These are the market leaders that I’ve said would fall the hardest during the developing collapse.

Following such high-tech trends, the QQQ and the NASDAQ have busted below their lower support trend lines, and the NASDAQ has plunged well below its 200-day moving average:

More than 50% of NASDAQ stocks are in bear markets. The average NASDAQ stock is down 38%! The total index, itself, is already in full correction (down by more than 10%).

Goldman Sachs led the present slide in the reporting season for the fourth quarter of last year when the massive bank got sledge-hammered after its earnings report, diving 7% in one day to where it has now lost 8.5% of the company’s value.

The taper tantrum is here

“The Problem?” asks one analyst…

The Fed taper has started, earnings have been disappointing to start the year, momentum and technical conditions continue to weaken, and possibly the most significant factor is that valuations are still very high.

First on his list: the Fed taper has started, and that taper still has a long way to go. Everyone is saying it now. That thing that I predicted would kill stocks — the Fed’s taper being rapidly accelerated by inflation — has arrived, and it’s decimating stocks already by doing exactly what I’ve said it will do — releasing bonds from the Fed’s steely grip so they can finally price for inflation. That last bit being the key blindspot that I said almost no one in these markets was understanding.

Looking at what is happening in combined stock and bond prices (inverse of bond yields), they haven’t fallen in unison this hard since last March:

If you maintain the old standard 60-40 stocks-to-bonds portfolio, you’ve lost money in thirteen of the last fifteen days. For bond traders holding ten-year treasuries, this has been the worst start of a year in three decades!

With all this, how is that long-languishing market volatility doing? Well, for the NASDAQ, it’s suddenly getting up there again:

Measured in another broader way, volatility in stocks right now is looking like it did in the early days of the dot-com bust:

And we’re just getting started because, as I laid out in my most recent thank-you post for those who support my writing, the Fed is still adding liquidity to markets like there is no tomorrow. While it is already halfway through its tapering, “tapering” only means it has slowed down in how rapidly it is adding QE. The Fed is still doing as much QE as it did at its various peaks anytime since the Financial Crisis that put us into the Great Recession, which I will show further down below.

The bond vigilantes are back

Just backing off on Fed bond purchases has already released the bond vigilantes:

The Rates Vigilantes are at the gates and are now pushing through / above 4 hikes in ’22…and with more trending.… The Fed will simply “have to” take what the market is dictating to them, despite me currently believing that the FOMC has little desire to do-so.

Nomura via Zero Hedge

That is what “bond vigilantes” do. What the term represents is bond investors taking the lead in setting bond yields to such a level that bond yields, by themselves, force other interest rates up that are pegged to bonds, which can even drive up the Fed Funds Rate. This is EXACTLY what I have been saying will happen. As the Fed releases its grip on the bond market, those bonds that everyone thought did “not see inflation coming” will rapidly price in the inflation that bond investors actually do believe is already here and is coming. THE BIG KEY I GAVE YOU: It is only the Fed’s MASSIVE manipulation of the bond market that has suppressed true price discovery, which is now going to get real again VERY QUICKLY. (Without any price discovery in the bond market, of course it looked like “all-wise” bond investors saw no inflation coming. Practically the only bond investor in the pool was the Fed, since it was buying more than 50% of treasuries issued, and we all know the Fed didn’t see any inflation coming because it kept telling us that!)

What the return of price discovery (the re-entrance of the bond vigilantes) means is that the Fed will BE FORCED TO rapidly raise its official base inter-bank lending rate (the Fed Funds Rate) just to maintain the illusion that it is in control. It cannot be seen setting a low Fed Funds rate as a stated target and having that rate float above its target due to market forces, and it will not be able to maintain that rate at zero as it relinquishes its death grip on bonds, so it will be forced to raise its stated target to match what is actually happening between banks.

Such is the work of “bond vigilantes,” forcing the Fedto rapidly reprice all interest rates for inflation, regardless of what the Fed wants. The tail is starting to wag the dog. The Fed’s only route out of that is to go back to QE in order to rest control back from other bond investors, which would shove inflation into a neighboring solar system. It doesn’t want to do that.

Nomura’s Charlie McElligott warns that a good part of this vigilante action might happen in a quick dump this week because …

We see “-100% Short” signals across every G10 Bond and MM Rate in the model.

In other words, the aggregate of bond shorts has grown so high that those shorts, now that bond prices are falling, will force the investors who are on the long side of those trades to rapidly sell, collapsing bond prices even further in favor of those who are shorting bonds. There is an elevator down here, ready to be taken, and someone at the top has a pair of loppers around the cables.

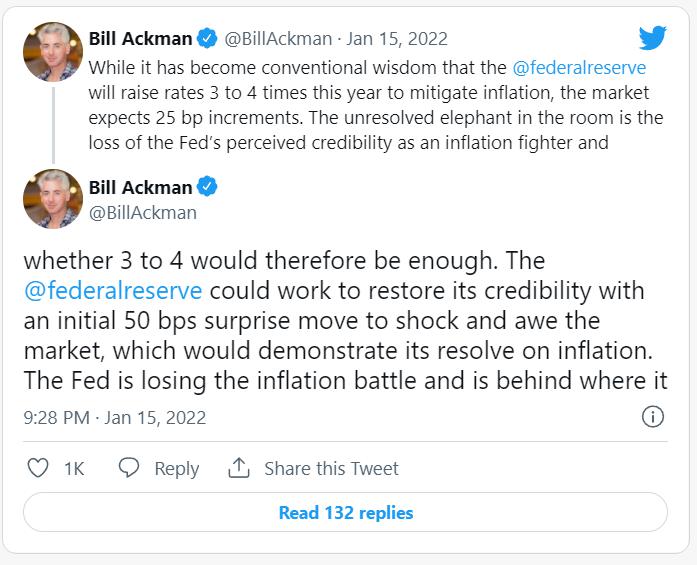

The market has already priced in four rate hikes this year, but that is still below what Fed members are saying is likely. Both Nomura and Deutsche Bank are suddenly saying (just since I wrote that Patron Post that said yield escalation was coming quickly) they anticipate the Fed will lead off with a shock move to signal to everyone it is finally taking inflation seriously, raising its Fed Funds rates by half a percent in one jolt in March; i.e., the second its taper is complete. Beyond that, Deutsche now says,

The most likely scenario is that the Fed begins to raise rates at each meeting this year beginning at the March meeting,

Deutsche isn’t the only one who foresees a shock move with an initial 50-basis-point rate hike:

Ackman, from what I’ve seen, talks his book — i.e., says whatever it takes to manipulate the listening stock market to do whatever is good for his positions — and it sometimes works! However, BofA has also hinted at a 50-basis-point initial hike in March, and Jamie Dimon of JPMorgan is now predicting 6-7 rate hikes this year.

The last time the Fed moved at this speed was 22 years ago when the Fed popped the dot-com bubble. Interesting, since I have also said this market destruction is likely to play out like the dot-com bust.

Here is what Charlie McElligott says about how quickly the bond vigilantes could make all of that happen (as early as this week) in his always half-digested, gut-bomb quant talk:

The potential for a “short gamma / negative convexity” event grows substantially on Dealer hedging “accelerant” flows, which would push 10Y yields beyond 1.90% (to the inevitable 2.00% Maginot Line)…

Heck, that event is already looking easier than it is to read. He’s saying interest rates may change even faster than they have been due to the short positions in the bond market, and I’m saying that will accelerate the Fed’s already rapidly changing stance (as I described it in that Patron Post) by pressing the Fed to hike its Fed Funds Rate even faster just to keep up with the real-market pricing that the Fed’s step back from bonds is now allowing. These shorts could reek havoc this week, making even March a late date for the first re-rate out the gate. I have always stated this new inflationary economic climate would drive the Fed into hyperdrive because the Fed was completely missing the boat with its mantra last year that inflation was “transitory,” but this would be even faster than I anticipated if those gamma shorts kick in.

The key mover right now is the 10-year yield, which has already slammed well above its 1.8% barrier since the Fed taper got serious this month and appears to be reaching for 2%. While I was writing this article, the 10-year touched 1.899% intraday. That’s as close as you get in Marketworld to tagging 1.9% without actually doing it, and the week’s only half over. So, it may be that the short situation Nomura sees as a possible climax on Friday is already starting to play through. No one wants to wait to the last day in a crowd like this.

When bond yields are up, prices are down, so the kind of bond action we are now seeing leaves bonds cheap relative to stocks, meaning the old reason for buying stocks that drove the stock market through a good part of the past decade — TINA (There Is Nothing Else) — is dead … or, at least, on her death bed and fading quickly.

Suffice it to say, the counterbalance to the price of 10-year treasury bonds is yields, which have made a quick trip up to 1.9% and may even hit 2% very soon, allowing a rapid ride down on the bond price elevator. It is at 2% that you can say the cables simply got cut, and we’ve started an all-out bond crash. Hitting that level so quickly, if it were to happen, could cause all kinds of things to go catastrophic because stocks and other markets react even more to the speed of bond interest changes than the amount.

McElligott is not saying, however, that bonds will go there this week, but he’s saying the way the market is shorted, it currently has the potential to take that kind of dive in bond prices (rocket-ride in bond yields). There would be blood in the streets at that pace to that level.

McElligott refers to this as a financial conditions tightening tantrum and, therefore, warns, US Equities Index Options positioning into Op-Ex this week is particularly dicey.

That is because, if bond yields rise that rapidly, letting bond prices fall, money will flee from stocks to bonds because TINA lies dead under the crashed elevator at that point. McElligott warns to watch the 127 level as the tipping point on the ten-year. Below that, the elevator has lots of room to fall unhindered.

Aside from this week’s possible accelerant, Andrew Ticehurst, a rates strategist at Nomura, say history suggests that 10-year yields are unlikely to peak before the first rate hike of the cycle. Since we’re already essentially tagging 1.9% today, and the first actual rate hike implementation is probably two months away (though the Fed’s decision may come as early as this month), the vigilantes have time to work.

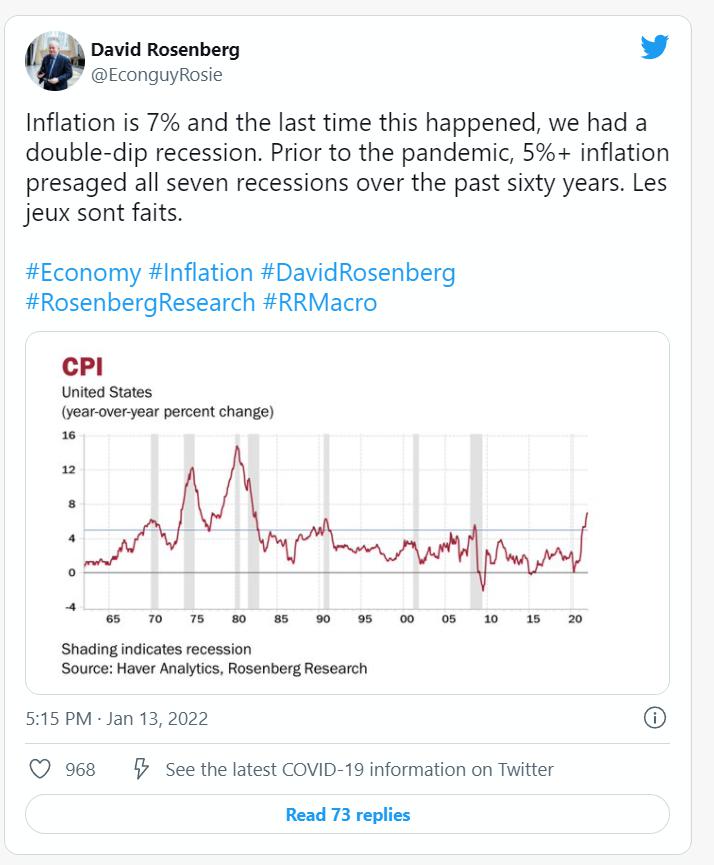

All of this has already resulted in a violent flattening of the yield curve, even though all yields are moving quickly to price in inflation as the Fed leaves yield-curve control behind, as I also said would happen. That indicates we are pressing rapidly toward the recession I promised for the start of this year. David Rosenberg notes this as well:

Rosenberg went on to note that the Fed prepping the market for a 25-basis point hike but then leaping in with a 50-basis-point hike will “do wonders for its communication skills!” From all appearances, as laid out first in my Patron Post but now with additional support here, we appear to be entering the Fed’s most rapid tightening schedule in history!

Hmm, ending QE and hiking interest rates just as we slide into recession, what could wrong with that?

(And, if you knew what additional big move the Fed has in store as I laid out in that post, you’d know we’re really in trouble. That is how desperate the Fed is to catch up with the inflation it let run out of control, and it cannot so easily back out of its tightening this time if the pram runs off the rails because inflation is the Fed’s pram driver, and it’s not letting up.)

Said recession, coming from the Big Bond Burst that is starting to unfold, will also include a spill over into housing as the probable crash of the bond bubble takes out the everything bubble, which includes the housing bubble by driving up mortgage rates:

The Fed’s now-clear assault on “too-easy” financial conditions via their pivot to “Inflation Hawks” as it has become a non-partisan political issue into mid-term elections … with the knowledge that mortgages have not yet even begun to feel the full sting of the coming market ownership reversal, as the Fed … forces actual “price discovery” … MBS spreads are already moving meaningfully wider… affordability in the housing market evaporates completely.

I’m already seeing real-estate ETFs go wonky and even commodity ETFs seem to be joining the stock market’s slide, so I’ve pulled my money back out of those. They were doing great for awhile because of inflation. Suddenly, not so much. I guess that is what the bursting of the everything bubble looks like. Even what seemed safe group may join the momentum of the slide.

Of course, McElligott’s big warning about the potential short trip down in bond prices may not come into play. In that case, all of the above still plays out, but just not as quickly because I’ve said all along to expect a tug-o-war between stocks and bonds that likely plays out over months as those two markets tussle for equilibrium.

McElligott, however, is not the only one saying this could all slide quickly now.

Real yields may be about to see a massive move higher…. Real yields are racing higher, with the 5-yr TIP rate now at -1.22% the morning of January 18. [Two weeks ago] the 5-yr “real” yield was -1.6%. The higher this rate climbs, the more the [stock] earnings multiple will contract. The biggest problem for the equity markets is that the “real” yield on the 5-yr TIP may be about to go much, much higher. A technical chart shows that the 5-year TIP rate may make a significant breakout, sending that real yield soaring from -1.22% to around -50 bps. That would be an increase of more than 70 bps, creating carnage in the already overvalued equity market.

Even TIPS (Treasury Inflation-Protected Securities) are not keeping up with the real rate of inflation. You can see the TIPS bond market made a sudden leap up at the end there as soon as it cleared all the 2021 little ups and downs. Now pressed up against its next point of resistance, it can make another abrupt run up another 70 basis points if it breaks through resistance, which still won’t have caught up with inflation as they are supposed to.

On the stock side of resistance, the S&P and Dow are already below their 100-day moving average and still falling. As noted the NASDAQ is below its 200-day average, and mid-day today is falling further. For the moment, this is moving money out of stocks and into bonds, easing bond yields a little. That is the seesaw I’ve said we should expect when the reason for stocks falling is bond yields rising due to the Fed tightening faster due to scorching-hot inflation at the Fed’s back, leaving it with little choice. Here is another key point I don’t want you to miss: All of these inflationary pressures leave the Fed unable to back out so easily as it did in 2019 when its 2018 tightening went off the rails.

Hear others saying it, so you don’t have to just take my word for it

Here is some perspective from others on the Fed’s moves and resulting bond action:

Last week’s “Fed hawk shock” warrants trading the new higher rate range “with a bearish duration + curve flattening bias”

Bank of America (via Zero Hedge)

Based on the rate movement in January so far, we think only a small fraction of the anticipated QT effect is priced by the market.

Deutsche Bank

The repricing of duration to start 2022 signals risk of higher yields ahead [as] too many central banks are on the move or sending signals, rendering traditional cross-market valuation metrics less reliable. [An early start to Fed QT] will steepen the yield curve,and open the door to more rate hikes over the cycle — not fewer — raising the terminal rate the Fed could achieve [to 8 hikes].

Morgan Stanley

We see more room for yields to rise, although the path to higher yields is likely in stages

Société Generale

It feels like it was only last week that we published our 2022 Market Outlook. Technically it has only been two weeks, but so much has gone on…. Certainly, in 2022, January is forcing us to do more than we usually do in a quarter, if not a year! Now it is like there is some race to be the first to call for more aggressive Fed actions!

Academy Securities via Zero Hedge

Does the Fed have little choice?

What the Fed actually does will likely depend on how economic data — particularly inflation data and wage data and GDP data — look at its future FOMC meetings. I will go into all the reasons that shortages are going to continue or even worsen so that Fed-fueled inflation is going to keep rising in another post (likely my next), but let’s look at the conundrum the Fed is already in.

Over the past few weeks, Fed speakers are bemoaning inflation and voiced their wishes to squash it. They frequently mention how effective their monetary toolbox is in managing inflation.

********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.