Why The Fed Will End QE On Wednesday

This week we will find out the answer to whether the Federal Reserve will end its current quantitative easing program or not. Today is the last open market operation of the current program, and my bet is that it will be the last, for now. Here are my three reasons why I believe this to be the case.

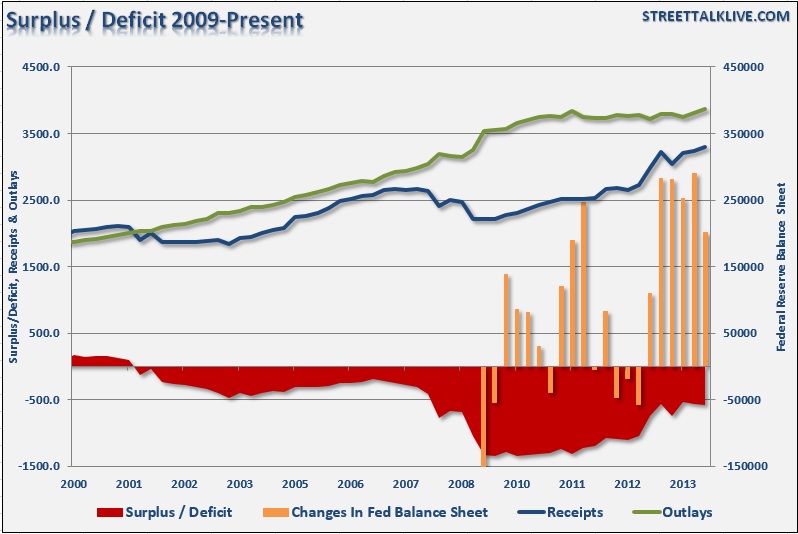

1) Much Smaller Deficit Restricts Treasury Bond Issuance

Over the last few years, the Federal deficit has shrunk markedly as infighting between Republicans and Democrats has restricted government spending to a large degree while taxes were increased across a broad spectrum of American taxpayers. The good news is that the U.S. government is closer than in many years to running a balanced budget, although it is has been more by accident rather than through a logical approach of budgeting and waste reductions. The bad news is that deficit spending has been a major contributor to economic growth in the past and the reduction of such has been a drag on economic growth recently.

The chart below shows the level of federal spending, revenue and the deficit. I have added the Federal Reserve's balance sheet which has been a major buyer of U.S. debt in recent years.

One of the reasons, as I explained previously, that the Federal Reserve will allow the current QE program to conclude is because the shrinking deficit is reducing the number of bonds being sold by the Treasury.

"But in the economic recovery phase, the federal deficit commenced shrinking sooner than the Fed commenced tapering. There reached a point at which the Fed was acquiring more than 100% of the net new issuance of US government securities. At that point, the Fed's buying activity was withdrawing those securities from holders in the US and around the world. Essentially the Fed was bidding up the price and dropping the yield of those Treasury securities, and it was doing so in the long-duration end of the distribution of those securities.

The Fed has taken the duration of its assets from two years prior to the Lehman-AIG crisis all the way out to six years, which is the present estimate. It is hard to visualize the Fed taking that duration out any farther. There are not enough securities left, even if the Fed continues to roll every security reaching maturity into the longest possible available replacement security."

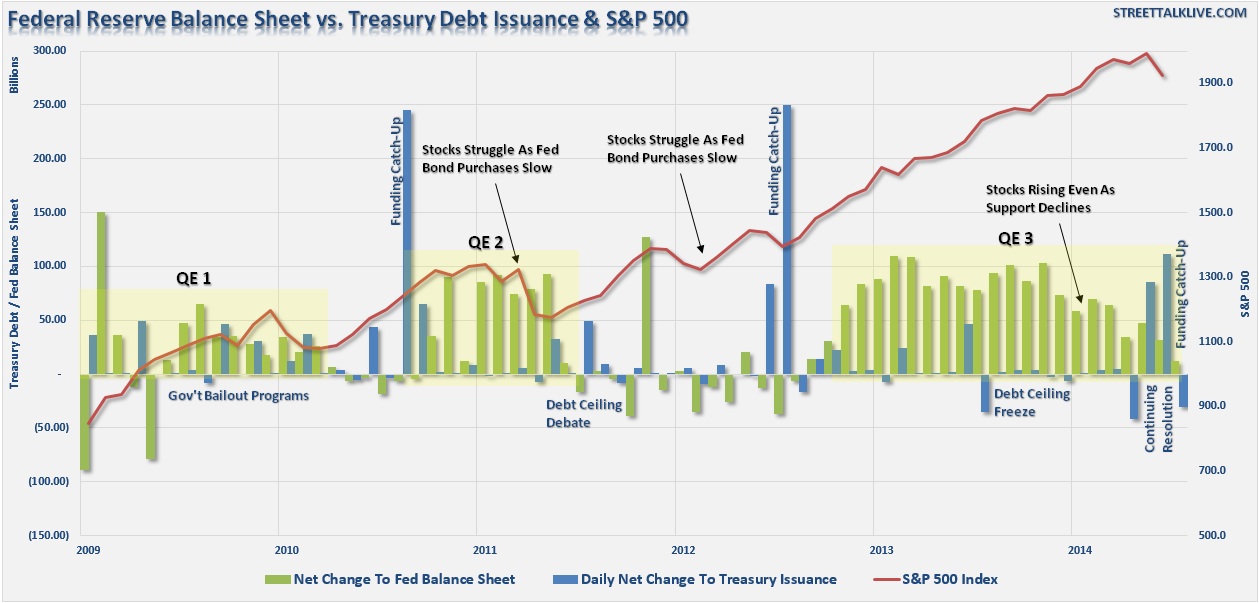

The chart below illustrates this point.

As you can see, the net change to the Federal Reserve's balance sheet swelled during each of the quantitative easing programs. The liquidity supplied flowed into the financial markets driving asset prices higher. Importantly, notice the extreme level of balance sheet expansion during QE 3 which caused assets to surge in 2013. However, since the beginning of 2014, the balance sheet expansion has markedly slowed and along with it the inflation of asset prices.

Importantly, with the Treasury issuing fewer bonds due to reduced funding needs, the Federal Reserve can not keep the current pace of purchases going without the risk of potentially creating a liquidity problem within the credit markets. I am quite sure that the Federal Reserve is aware of this issue which is why, despite many bumps in the market this year, they have continued their pace of reductions without pause.

For investors this is critically important to understand, as shown above, there is a very important correlation between the Fed's QE programs and the liquidity flows that support asset prices. As that liquidity push is extracted from the financial markets, there will be a corresponding increase in market volatility. "Tapering" is in effect a "tightening" of monetary policy which historically slows the growth rate of asset prices.

2) Not Ending Program Could Send Wrong Message On Economy

Boston Federal Reserve President, Mr. Rosengren, recently stated that: the Fed's asset purchases have achieved their stated goal, the jobs report for September is already in and his economic forecasts have not changed.

"There has been substantial improvement in labor markets, and as a result I would be pretty comfortable [ending purchases] at the end of the month.”

"Fed Speak" holds much sway over the markets. After each meeting, as Janet Yellen gives her press conference, market participants are quick to parse her words and place market bets on what they think she is implying. Up to this point, each post-meeting confab has been a reaffirmation that the economy is improving enough to expand without the support of monetary policy.

It is very likely that if the Federal Reserve decided to keep its current pace of bond purchases in place it would likely be interpreted that the economy is indeed not as strong as the statistical headlines suggest. Such an interpretation could lead to a repricing of risk, and a sharp decline in asset prices, that would potentially destabilize consumer confidence. This is not the outcome that the Federal Reserve is looking for.

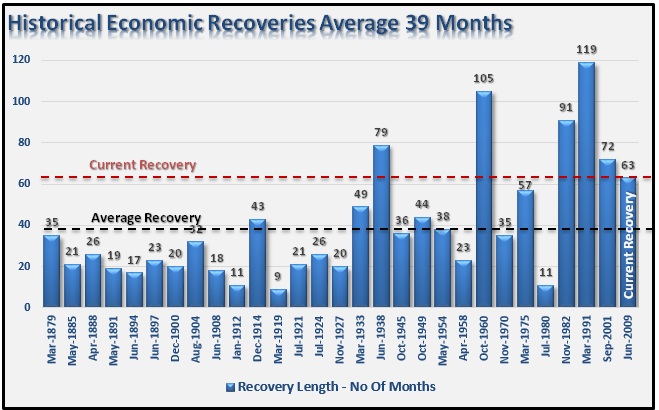

3) Must Normalize Policy Before Next Recession

Most importantly, the economy is now more than five years into the current expansion. As shown in the chart below, we are now in the fifth longest economic expansion on record. This sounds great until you realize that has been achieved with the lowest level of economic growth of any post-WWII recovery.

While much of the mainstream media, analysts and economists ignore normal economic cycles, it is very likely that we are closer to the next recession than not. This is not a bearish prognostication, but rather just the realization that despite the Fed's best intentions, normal economic and business cycles have not been repealed.

The problem for the Fed is that with the effective interest rate near ZERO, one of their most important monetary tools to offset recessionary drags within the economy has been removed. The chart below shows the history of the Fed's overnight lending rate as it compares to economic growth, the market and recessions.

Historically, each time there has been a crisis, or recession, the Fed has responded by dropping the effective Fed funds rates in order to induce borrowing and lending within the economy. As stated, with the rate near zero, the Fed is trapped without an important policy tool if the economy slips into a recession in the near future.

This is why they have been so vocal about raising short-term interest rates. The Federal Reserve needs to normalize monetary policy before the next recession hits in order to have some "working room" to stem off any potential future crisis. Ironically, there is a case to be made that the Fed's interest rate policy manipulations are a cause of economic crises and recessions.

For these reasons, I highly suspect that the Federal Reserve will announce the end of the current "QE" program during their post-FOMC conference on Wednesday. How the markets respond initially will be focused on what she "says," however, going forward the "lack of liquidity" may become a much more important issue.

Just my opinion of course.