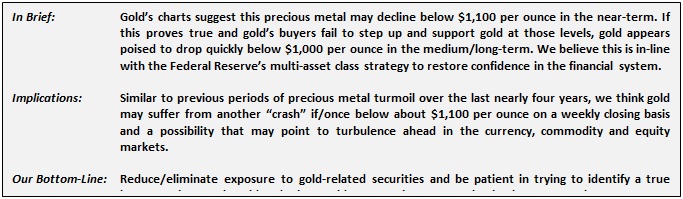

Will Gold Go Below $1,000?

After enjoying a robust bull market run for more than a decade, gold’s long-term uptrend officially reversed last October and something that suggests continued selling pressure is likely to drive gold lower – perhaps significantly lower – over the medium/long-term.

This possibility is consistent with our prevailing view on gold over the last four years and it could validate our September 16, 2011 note titled Gold to Fall By 50%. At that time, gold put in a weekly close of $1,857 per ounce with the charts suggesting its increasingly fragile uptrend was close to breaking and something that started just a week later and within weeks of gold’s record nominal high.

Ironically, then, the official end of gold’s secular bull market that came late last year may be best viewed as merely the finale to cap gold’s 40%+ reversal from its 2011 peak and one driven by the Federal Reserve’s September 2011 initiation of Operation Twist, in our view.

We believe this is an important point to make because it highlights the current success of the Federal Reserve’s multi-asset class strategy to restore confidence in the financial system and economy coming out of the 2008 financial crisis. Specific to gold, the Federal Reserve steered investor money into stocks and out of gold through the guidance of Operation Twist and policy that offered implicit support for the dollar.

On the face of it, this observation may sound simplistic, but the power of what the Fed did cannot be underestimated.

In short, the Federal Reserve successfully stirred the animal spirits in late 2011 – again – to create a bullish shift in investor confidence and one that favored risk assets over the perceived safety of gold.

Testimony to the power of this shift toward risk taking on the part of investors and away from safety is demonstrated by the fact that SPDR S&P 500 Trust (SPY) now holds net assets of about $194.1 billion relative to GLD’s current net assets of $30.1 billion according to data from Yahoo Finance. This is in stark contrast to the National Inflation Association’s report that GLD held net assets of $77.5 billion in August 2011 “which at the time was equal to SPY’s net asset value of $77.5 billion – for a SPY/GLD net asset value ratio of 1.”

What makes this sort of a shift in investor sentiment so valuable, and especially coming out of the worst financial crisis since the Great Depression, is that it encourages a virtuous wealth effect. This is thought to occur when a rising stock market helps ordinary Americans feel more confident, and thus drives consumer spending, corporate capital expenditures, job creation and, ultimately, organic economic growth.

Until interest rate policy is normalized and there is no reason to think the Federal Reserve may have to initiate another bond-buying program, it is unclear whether the result of its policy moves over the last six years will be a strong economy that can grow on its own.

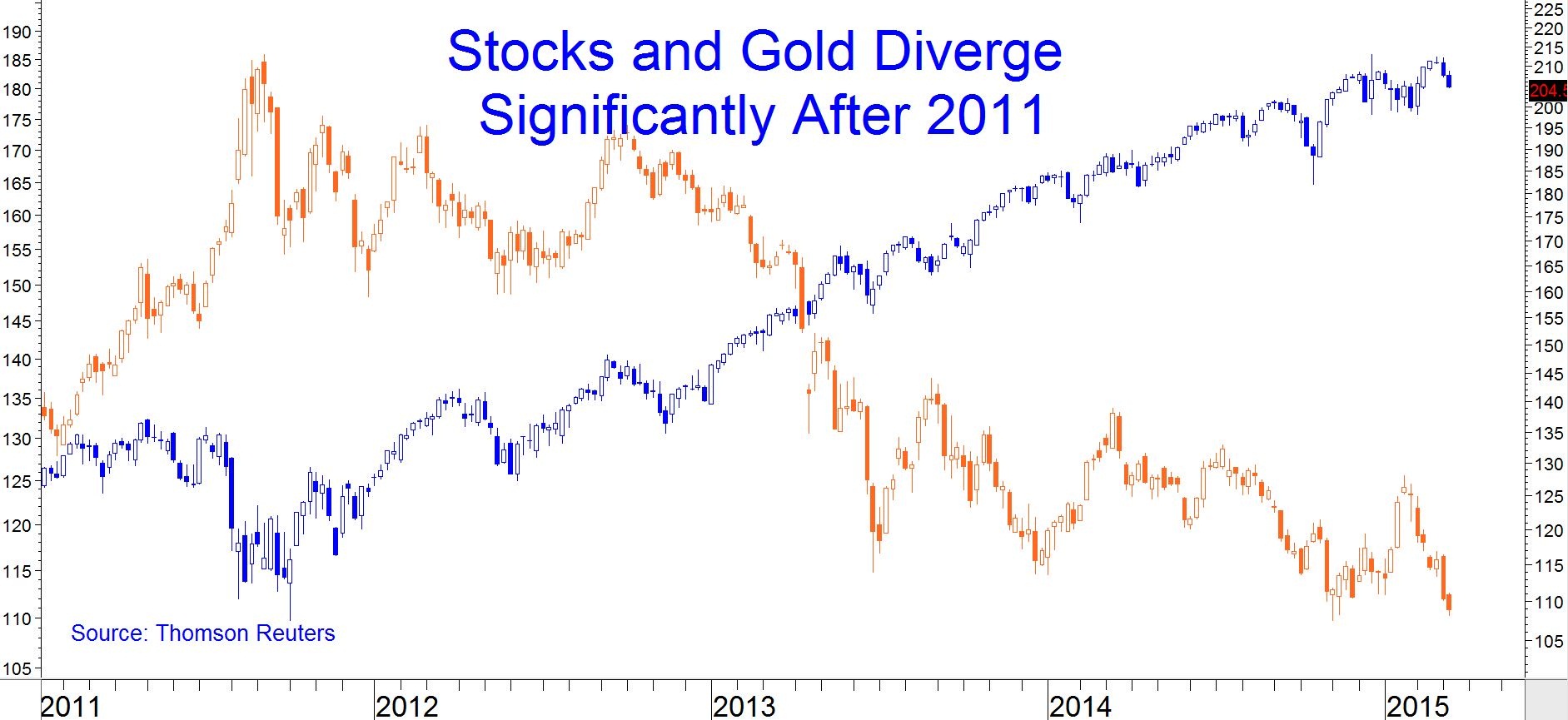

What is clear, however, is that gold (GLD in orange) and stocks (SPY in blue) diverged significantly starting in the fall of 2011 and right around the start of Operation Twist.

When this observation is extended beyond the financial system, we think it is nearly as clear that the Federal Reserve has worked very hard to help steer the U.S. economy toward full and independent health and something that the Fed should be applauded for whether successful or not ultimately.

When this observation is extended beyond the financial system, we think it is nearly as clear that the Federal Reserve has worked very hard to help steer the U.S. economy toward full and independent health and something that the Fed should be applauded for whether successful or not ultimately.

Source: Thomson Reuters

Interestingly, however, the charts of gold and the broader stock indices appear to disagree on what this outcome may be with the former supporting the constructive intentions of the Fed and the latter suggesting the Fed’s plans may be challenged and particularly in the next 12+ months.

Sticking with the topic of gold alone at this time, its charts point to continued declines as mentioned above for the following reasons.

Sticking with the topic of gold alone at this time, its charts point to continued declines as mentioned above for the following reasons.

First, gold’s broken long-term uptrend tells us the sellers are in control and are likely to exert this control over time.

Source: Thomson Reuters

Second, the congestion and uncertainty of the last two years presents in a bearish manner due to the lower highs and points to a downside resolution at this point. It is best to consider both sides, though, and this means that if gold closes above $1,433 on a weekly basis, it may climb to $1,687 per ounce but continued time spent below $1,181 per ounce suggests a move to $929 per ounce.

Third and supporting the potential move lower in gold is the Descending Trend Channel that indicates gold may fall to about $1,100 per ounce and probably within one to three months.

Should this prove true, it would constitute another severe break in support akin to the one made in April 2012 and perhaps lead to the next notable “crash” in gold. It is difficult, in our view, to believe that gold would find support near a potential move back down to $1,100 per ounce and largely due to the lack of support in 2012 on a similar aspect.

Rather, we tend to believe that gold’s sellers will be as punishing as they were in April 2012 and push gold sharply lower for a 50%+ fall from its nominal peak of $1,921 per ounce.

Whether this frees up investor money for allocation toward equities as has occurred over the last several years under the careful supervision of the Federal Reserve is to be seen and is perhaps a topic for us to explore at another time.

At this time, we think it is worth suggesting that the preponderance of the technical and multi-asset class charting evidence makes a strong case for gold to go below $1,000.

*********

Investment Advisory Services offered through Greenbush Financial Group, LLC. Greenbush Financial Group, LLC is a Registered Investment Advisor. Securities offered through American Portfolio Financial Services, Inc. (APFS). Member FINRA/SIPC. Greenbush Financial Group, LLC is not affiliated with APFS. APFS is not affiliated with any other named business entity. Abigail Doolittle is a registered representative with American Portfolio Financial Services, Inc. Information in this illustration has been obtained from sources believed to be reliable and are subject to change without notification. The information presented is provided for informational purposes only and not to be construed as a recommendation or solicitation. Investors must make their own determination as to the appropriateness of an investment or strategy based on their specific investment objectives, financial status, and risk tolerance. Past performance is not an indication of future results. Investments involve risk and the possible loss of principal. Any opinions expressed in this discussion are not opinions or views of American Portfolio Financial Services, Inc. (APFS) or Greenbush Financial Group, LLC. Options expressed are those of the writer only. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not ensure against market risk. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

More from Gold-Eagle