The Wizards Of LIBERTY Street

Most everybody has seen the Wizard of Oz, but most don’t understand that it is a story about the removal of Gold from behind the dollar and the Federal Reserve at that time. The wizard was supposed to be the Federal Reserve chairman of that time, pulling levers on the economy and managing it from the seat of his pants. Well, nothing has changed. Fed chair, Yellen, commenting on recent legislation urging the Fed to create some rule like the Taylor rule (mathematical rule to guide interest rate decisions based upon GDP growth and inflation) to guide future interest rate decisions.

"It would be a grave mistake for the Fed to commit to conduct monetary policy according to a mathematical rule," - Janet Yellen

Keep in mind the fed has been flying by the seat of its pants since the Global financial crisis erupted. Policies previously UNSEEN in history (other than Zimbabwe, the Weimar republic, Argentina and previous hyperinflations) such as UNLIMITED money printing and zero bound interest rates for almost 6 years are illustrations of financial and monetary system on life support. Money at no cost to the banks and government but priced expensively for the public, and savers who earn nothing on their accumulated life savings.

The very idea that unaccountable mandarins of money need to play with no rules or guidelines should have been halted decades ago. Now, it is TOO LATE to DO SO. Normalization of rates will bring down more things than any of us can imagine as the world is awash in financial assets which yield little or nothing. Malinvestments in the classic Austrian definition.

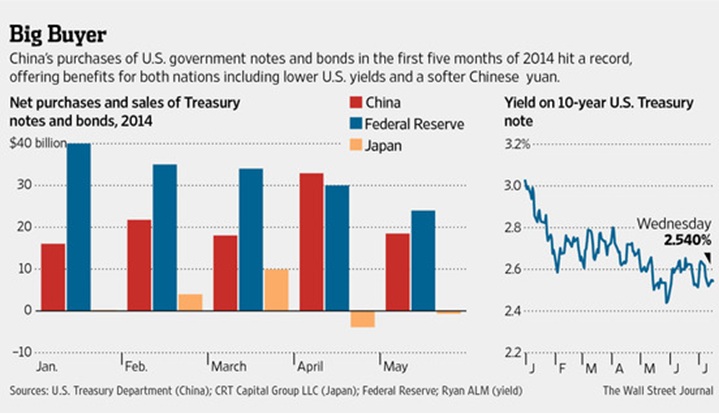

Big Buyers in a fool’s paradise

The mortgage markets are dead meat to investors unless the issues are “government guaranteed” and it would appear much of the US treasury market is unattractive to the private sector as well. Taking a look at treasury issuance since January, the vast majority of them have been hoovered up by central banks, most notably the Federal Reserve, Bank of China and Japan.

Looking closely at the purchases reveals the fed is the dominant buyer. It has monetized over 50% of US debt since 2009. Is it for quantitative easing purposes as they say or FUNDING of the DEFICIT? To me, it is the latter, regardless of the story they say. In real terms, inflation is probably 9 to 10%.

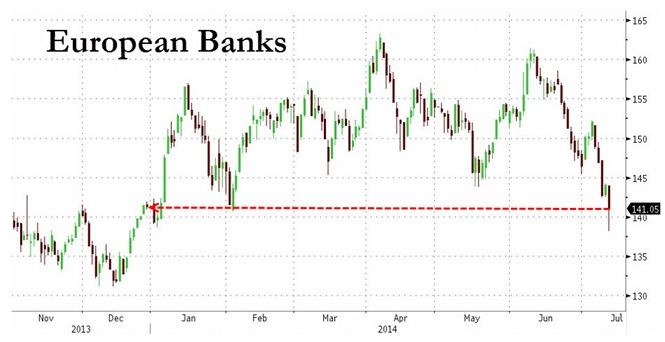

Is the TOP in for European Banks?

Last week Portugal’s second largest Bank Espirito Santo parent company missed a bond payment and markets reacted accordingly by tanking. Regular readers to this missive know that none of the banking problems in the European banking systems has even been remotely addressed. The next exercise in HOT AIR and PR is currently underway as the European Banking Authority and the ECB work together to boost CONFIDENCE with the AQR (asset quality review). I can confidently tell you in advance that ALL IS WELL. Maybe one or two banks will fail to provide the veneer of robust exams but the result was written before the test if past episodes are prologue.

Europe’s problems have not been addressed: Quoting Allianz SE’s chief Investment officer Max Zimmerer (Europe’s largest insurer managing assets of over $757 BILLION dollars) and owner of PIMCO:

“The fundamental problems are not solved and everybody knows it”… “The euro crisis in not over”… “Countries are still building their debt piles and that’s storing up trouble for the future”. “There is only one country where the debt level last year was lower than 2012 and this is a signal the debt crisis can’t be over, only a recognition of the debt crisis has changed”… If the debt levels are not going down in the end we will have a problem, that is for sure.”

Thank you Max for a very candid assessment of what lies ahead and Max is NOBODYS FOOL. Both the banks and Sovereigns are in worse shape than ever. The only thing that has recovered is the perception of the health of the nations and banks and for that we can thank the main stream media and morally and fiscally bankrupt politicians throughout the continent. Add to this the $30 Trillion dollars ($30 million million also known as a lot of ROTTING paper/cabbage) created out of thin air since 2008 desperately seeking a home anywhere a yield can be found (regardless of the risk). Although the markets MAY NOT BE FOOLED:

That’s a BIG head and shoulders TOP and fully active in technical terms projecting a 15%+ decline from here. We shall soon see if it is reflective of the CREDIT and SOLVENCY crisis returning which is baked in the cake. The only question is WHEN WILL PEOPLE WAKE UP? Is the next wave of insolvency beginning NOW?

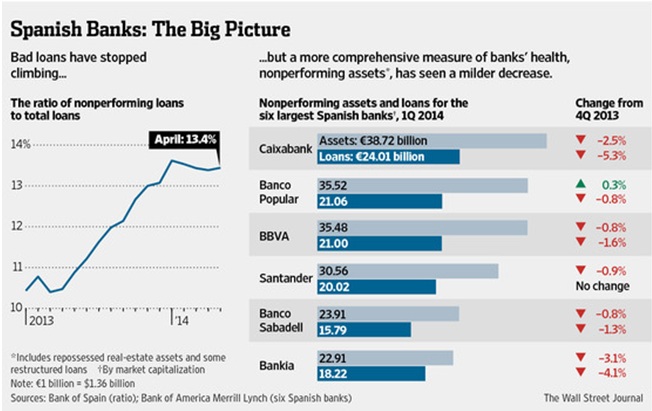

Spanish Banks, Lying with numbers.

Throughout the EU the official story is one of recovery in economies and the financial system. Neither could be further from the truth in my opinion. It is all HOT AIR courtesy of the MAIN STREAM media and the people that control them. Supposedly Spain has bitten the bullet and is firmly on the road to recovery financially and economically. But a close look at the banks REAL condition tell a different story. It is a story of selective presentation of the numbers and SPIN. Politicians and bank analysts are pointing to a leveling off of NON PERFORMING loans. Upon closer inspection their condition are barely improving and probably a result of accounting magic. Take a look at this chart of the 5 biggest banks showing the headline NON PERFORMING LOANS numbers in dark blue and the real numbers in light blue of NON PERFORMING LOANS and ASSETS combined:

“Nonperforming assets are a better measure of banks' health, some analysts say, because the metric shows the full extent of bad debts the lenders have to work through and provide a more realistic picture of the continued drag on earnings that banks face. It captures foreclosed homes a bank will have to try to sell and repeatedly refinanced loans to property developers or other businesses that are unlikely to be paid.” - Wall Street Journal

Merrill lynch reports their estimate of total non-performing assets to be euro 433 billion or $588 billion ($588,000 million) dollars or 40% of Spanish GDP. Doing the math: Non-performing assets are 22% of their balance sheets and their reserves barely 10%, simply doing the math says they are operating in BANKRUPTCY and negative equity of 12%. When will the RUNS BEGIN? Loan growth to the private sector is still CONTRACTING and buying of government debt still BALLOONING. Recent bond offerings of the banks have been gobbled up just as in all of Europe including GREECE. It’s all a con game. Who are these FOOLS?

********

Don’t miss the next edition of TedBits subscriptions are free at CLICK HERE. We will be covering the deflation in Europe and the insanity gripping sovereign bond markets.