Gold 2023 outlook: History suggests we could be gearing up for another bull market

LONDON (Nov 25) Gold has failed to benefit from the shift away from risk assets over the course of 2022, with the price of gold falling back from the $2000 peak seen in March. We have seen an incredible seven consecutive months of downside since then, with the dollar instead dominating as the primary haven asset for markets. More recently that relationship has helped drive gold higher as the US inflation decline helped drive the dollar lower. While we look to close out the year on a more positive tone than that set within much of 2022, the outlook for 2023 could create the basis for the next bull market.

Fed balance sheet highlight’s role of monetary policy

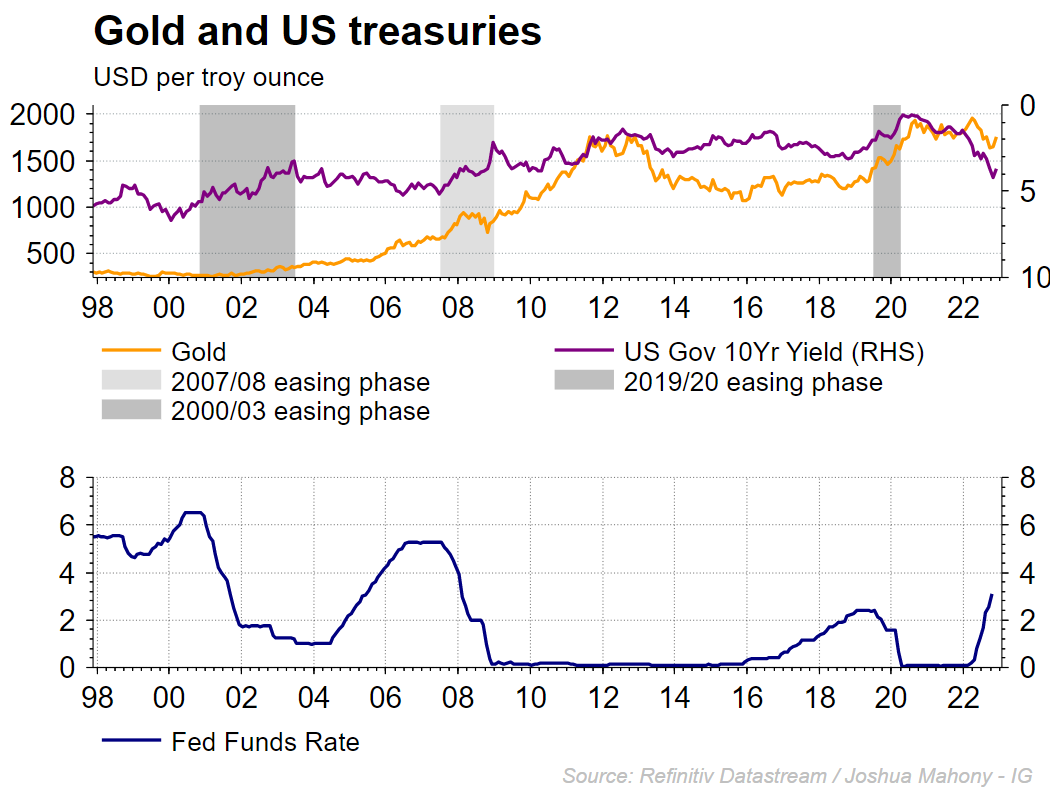

To understand the potential long-term trajectory for gold, we should understand what drives it. Unlike more commodities, gold has few use cases beyond investment and jewellery. To some this provides a primary reason to invest in silver, with the precious metal also widely used in an industrial setting. Gold meanwhile has typically been utilized as an investment vehicle, with many seeking to stockpile the commodity at a hedge against currency devaluation from central banks. The chart below highlights how gold has historically done well at times of crisis given the typical reaction from the central bank. Looking back at the 2008 and 2020 recessions (grey shaded band), we saw significant upside for gold as the Federal Reserve implemented quantitative easing programmes that enlarged the balance sheet. Typically, we see gold consolidate or reverse lower when the Fed moves to shrink that balance sheet. This does highlight why we have seen gold underperform this time around, with the inflationary element of this crisis meaning that the central bank tightens policy rather than the typical expansionary approach.

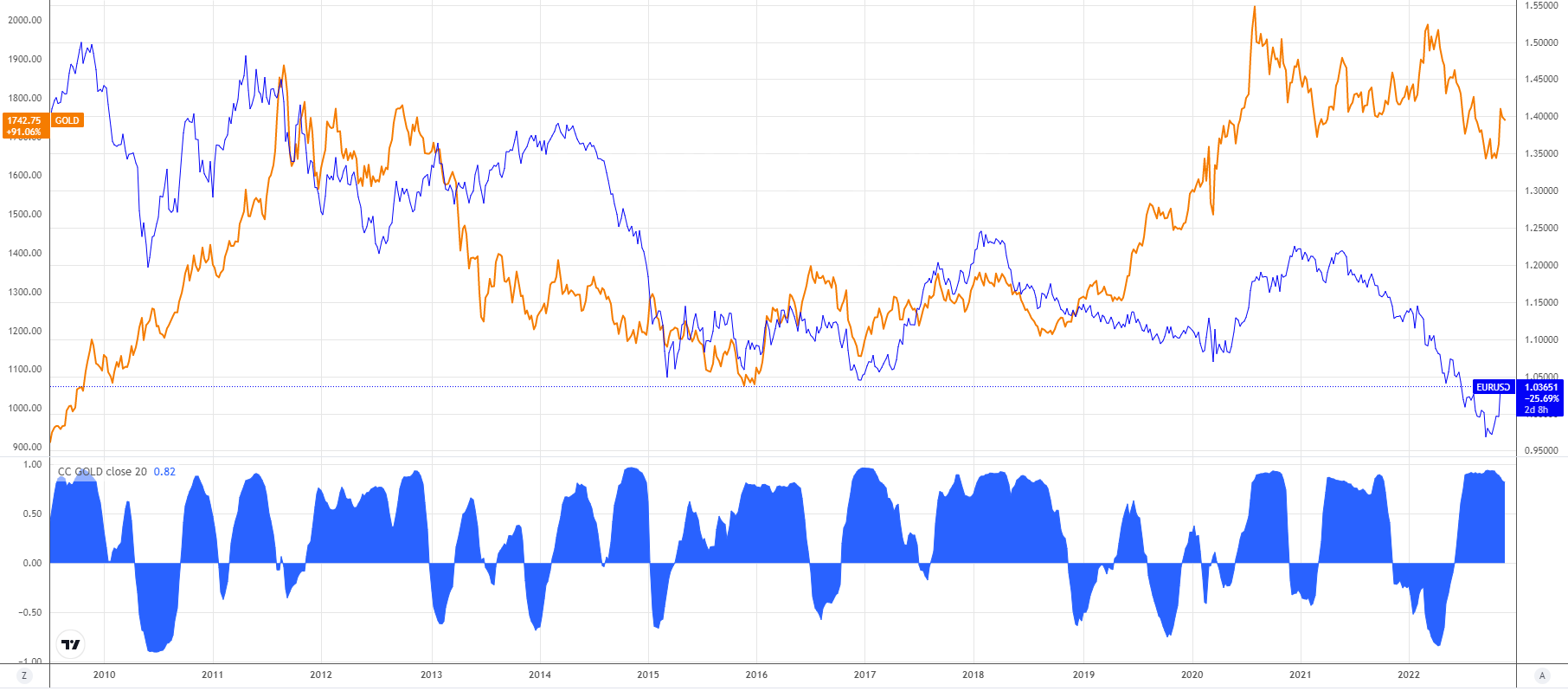

Dollar strength has hindered gold demand

While the dollar has often been blamed for the demise of gold, that negative correlation is not always a positive one. The role of inflation in this latest crisis does help heighten that inverse correlation, with the correlation coefficient between the dollar and gold below highlighting that typically a stronger dollar will result in weakness for gold. What that means is that we may have to wait for the dollar to top out before gold comes back into strength. The decline seen for the greenback over the final months of the year has helped lift gold, but traders will have to consider whether this is the top for gold or simply a blip within a wider bull market for the greenback.

Source: TradingView

Source: TradingView

10-year bonds highly correlated with gold

It is worthwhile keeping a close eye on US treasuries, with the 10-year highly correlation with gold. As seen below, the dramatic decline in US 10-year bonds over the course of this crisis has done little to help the precious metal. Historically markets have seen recessionary pressures push money into safe assets such as US bonds, thus driving down yields as demand for treasuries rise. This time is different, with bond prices heading sharply lower ahead of a Fed-fuelled recession that could be protracted in nature. Looking at the depth of this decline for bonds, we have seen a relatively small pullback for gold. While that could signal the potential for further near-term downside, this long-term picture does highlight how the likely upward turn in bonds will ultimately look to influence gold and drive the next uptrend for the precious metal.

It is worthwhile taking a look at the trajectory of US interest rates too. It is notable that the bullish phases for Gold have typically been instigated at periods of monetary loosening, with the rate cut phases in 2000, 2007 and 2019 marking the beginning of the major bull runs. In fact, we can see that the bulls do typically come into play a little before rates actually reverse lower. That could bring some similarity to the current situation. The key question here is just how long we have to wait until we see the light at the end of the tunnel from an inflation perspective. The moment that markets start to see potential loosening phase from the Fed will likely mark the beginning of the next bull market for gold. The problem is that this could take some time if inflationary pressures continue to stifle the ability of the Fed to shift back to an accommodative stance. Once we are over that hurdle and believe that inflationary concerns are on their way out, markets will likely react to the prospect of the central banks gearing up for a growth-focused policy set.

Will inflation spark the next bull market?

With inflation key to timing, traders will be keen to gauge exactly when these pressures will finally be brought under control. That is the million-dollar question, and there are many factors that could derail any forecast. Chiefly, another spike in energy would set back any plans given the potential for another secondary rise in inflation. Without such a spike in energy prices, the common perception is that we will see US inflation drift lower over the coming year. However, with the economy likely to suffer over the course of 2023, the difficulty is finding the moment when markets believe we are sufficiently out of the woods to start planning for a monetary loosening phase. According to the Reuter poll below, US CPI will be back to 3% by the end of 2023. Should that come to fruition, there is a good chance we see a strong end to next year as the bull case gather momentum.

IG.com