Market Talk, Economy & Bond Market

A premium excerpt of the first two segments of this week’s edition of Notes From the Rabbit Hole, NFTRH 876

Market Talk

At this point, far into the broad market recovery rally with gold stocks so close to the primary target (HUI 500+/-) I want to make sure I am speaking clearly as a human, rather than mechanically as a TA or macro funda dork. That will probably shorten this report and possibly the next few reports to come, until something big happens.

Big? Well, a broad top and breakdown would be big. A Fed policy shift would be big. A significant US Dollar rally would be big (given it would be against a government that seems bent on devaluation), a precious metals upside blowout and reversal, a commodity failure, a precipitous decline in long-term Treasury yields, or a resumed rise in those yields. All big.

But for now we’re in the slop. The oh so predictable recovery rally in stocks is grinding on while signs of slippage in the economy continue and the media continue to be focused on what it calls “inflation” (it’s not).

Economy & Bond Market

The big headlines (outside of robo headline maker, Trump) this week? Ooh, mortgage rates have fallen all the way to 6.6%! The media are advising whether Joe Sixpack should consider a refi on his house, assuming he bought the bubble at some higher rate. Well, I think rates will come down quite a bit further before the next inflation phase. And it’s not because the bond market will follow the Fed.

The Fed will likely follow a bond market temporarily shifting back to its traditional role of “safe haven” as the economy decelerates and inflation signals resume fading.

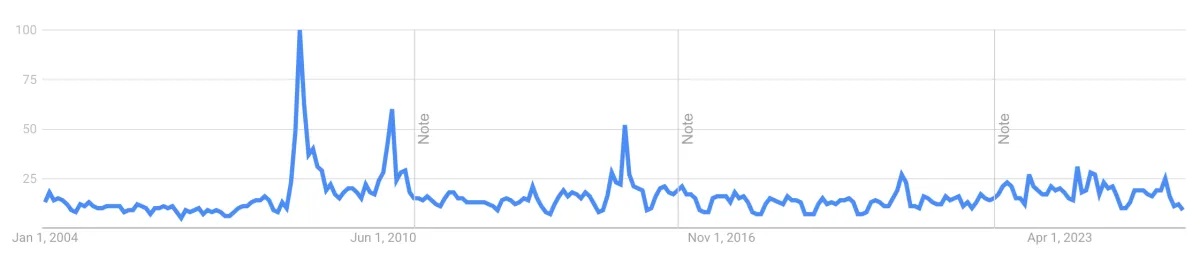

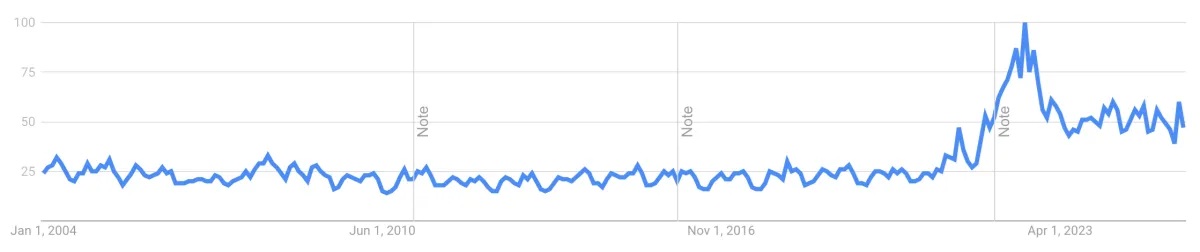

Based on Google Trends searches, nobody is thinking about deflation after deflation fear maxed in Armageddon ’08, after which Bernanke mopped up the macro with years of ZIRP (zero interest rate policy) and other unconventional policies of inflation (as permitted by disinflationary macro signaling). As a side note, the 2020 deflation hysteria pulled the Powell Fed into action so quickly that Ma & Pa did not have a chance to really start banging their keyboards about deflation before…

…the next and greatest inflation problem of this century manifested in 2021. At that point they started banging keyboards alright, and inflation remains by far the more prominent of concerns among the public.

So back to our trusty Continuum (30yr Treasury yield, monthly chart), the macro changed in 2022 and the inflation problem became all too obvious to the public. This is Captain Obvious speaking, but it is also relevant to the analysis because trends have broken. Trends in Google searches and trends in the bond market. It means something.

In my opinion, that something is that a contracting economy would probably see traditional bond market activity (declining yields) for a while, but not anywhere near the levels that allowed Bernanke to inflict ZIRP upon the world.

However, the daily version of the chart above is still trending up. So let’s be clear that the favored disinflationary view is not yet signaled by the 30yr yield. This is very likely due to noise about and effects of the tariff war and pricing. Again, this is not inflation. It is an effect of the trade war.

The 10yr is a bit more suspect, however. Take out lateral resistance and the moving averages and the two could join in a message that is yield positive and bond bearish. Until then, the 10yr yield is suspect at best and the 10yr Treasury bond is biased bullish.

As we slide down the duration curve to the 5yr yield we find a worsening picture as yields of shorter duration become more bearish (shorter-term bonds more bullish). This has been the plan for however long I’ve held short-term bonds direct from Treasury and also the SHY (1-3yr) fund in my accounts.

I recently added IEF (7-10yr) and that is in line with the prospect that the chart directly above would slide bearish, following the 5yr below. It should be noted that when including dividends, the 10yr Note has been firmly trending up for all of 2025.

This (bullish short-term bonds to still suspect long-term bonds) is of course in line with the steepening yield curve (10yr-2yr). Which is an economic bust signaler, with the question being “inflation problem or deflation problem?” Either way, short-term yields would decline relative to long-term yields.

The signal is that players are fading the long end in favor of the safety of the shorter-term. They are either fading inflation or liquidity problems. My bias is that they are slowly fading an oncoming liquidity problem and whiff of deflation.

And so it may come down to the question of whether it is different this time when yield curves steepen. Bear market example #1 below was a deflationary steepening. Bear #2 was even more pronounced deflationary.

The 2020-2021 steepener started deflationary (nominal yields dropping) and quickly morphed inflationary (nominal yields rising) after the Fed went balls out (monetary inflation) in tandem with the Trump-led government (fiscal inflation). The market rally that came with it was an “inflation trade”.

After that the curve flattened hard and inverted. The market correction of 2022 was based on fears of a hawkish Fed, but at the time we noted a flattening yield curve, which was not consistent with a real bear market. Indeed, it was just a solid correction.

Today the signal is high risk for the stock market as it rises in tandem with the steepening yield curve. By the will of Trump or just that it’s different this time in the new macro, I suppose there is a chance this will not manifest in a terrible bear market. I am not going to bet on that chance, but I will allow for the 1970s blueprint noted below [in the Precious Metals segment that followed, not included in this excerpt], that could see stocks run flat nominally, but wildly under-perform gold in this new macro.

NFTRH 876 then went on to discuss the U.S. stock market and gold/precious metals, and the two very different options in play for them. Both options are bullish for gold and gold stocks relative to the stock market. But in different ways and possibly subject to different types of interim activity.

For “best of breed” top-down macro analysis and market strategy covering Precious Metals, Commodities, Stocks and much more, subscribe to NFTRH Premium, which includes a comprehensive weekly market report, detailed NFTRH+ updates and chart/trade setup ideas, and Daily Market Notes. Receive actionable (free) public content at NFTRH.com and subscribe to our free Substack. Follow via X @NFTRHgt and BlueSky @nftrh.bsky.social, and subscribe to our YouTube Video Channel. Finally, check out Hammer’s trade (long and/or short) setups.

*********