Battle Still On…But The Tide Is Turning

share

share

share

share

share

share

share

share

share

share

What could become the turning point in a war that had become intense in 2011 and in the rear guard battle that had started in late April, happened last week. For the first four days, the battle had become one of exhaustion; it seems the counter-force lacked the reserves for a sustained offensive while the powers behind new trends of 2016 just could not make much progress either. Then on Friday a dose of reality on the worsening state of the US economy became a deciding factor. A very poor NFP number shook the metal bulls awake to the fact that the rearguard action is failing to achieve further success and that the time to stock up again has arrived. Prices of silver and gold jumped, and the DJIA needed sustained support throughout the day to try and recover from the opening weakness for a positive close, the same as on Thursday, but which failed by a small margin.

Last week gold and silver were in the midst of a major battle where the rear guard resistance to restrict the bull market was in full swing and the metals were testing their psychological support levels. Barely able to hold onto support, the metals had an ally appearing on their side – an NFP way below anything expected. In April, the NFP was a shock at just 160 000 official new jobs; in May, with the NFP at 38 000, it seemed the economy had braked to a stop! If the contributions of the Birth/Death model of jobs from new start-ups less the loss of jobs of businesses closing down in

May were not 238 000 and 224 000 respectively, the news would have been such the DJIA could never have recovered as it did on Friday, after a similar, more successful recovery on Thursday.

Whether Friday’s recovery was due to investors rushing back into the market after the weak open, knowing there would be no rate increase soon, or whether it was the PPT doing what they always do after a lower DJIA, does not matter. Even with the DJIA holding sideways, it is breaking just enough from its steep bull channel to hint at the bear coming in the front door. Also with reaction to the NFP number, the gold and silver prices jumped higher, away from the thoroughly tested support and also from off technical support that had just held, as the charts this week show.

The tide does not change in a rush; there is always a brief period of time when the tide still seems on the way out, but then the edge of wet sand no longer lapped by the stronger waves no longer increase, and then it shrinks as some waves begin to push higher, to show the tide has really turned. All of last week, after the previous decline in prices, gold and silver hung onto the psychological support and on Friday showed that the tide at last was coming in again.

The DJIA might just be ready to show that it’s tide, too, is at a turning point after a number of false starts. Dollar weakness, after it had completed a double top late in 2015, was halted early in May as it was urged also to confirm the US economy was still growing. Friday’s news was a shock to the currency; it now remains to be seen this week if it can continue to recover against the run of the turning tide.

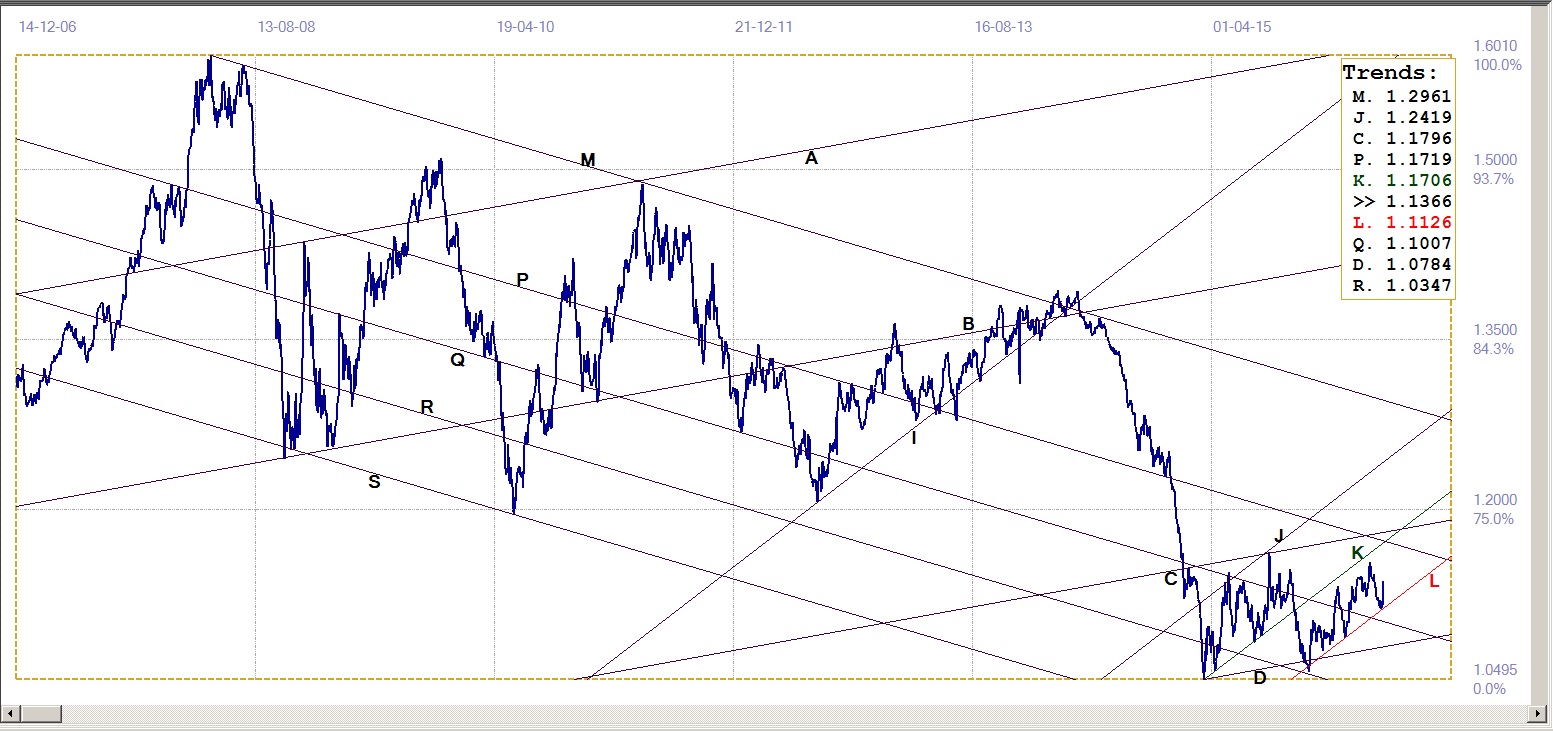

Euro-Dollar

Last week the euro really came to test support at the bottom of its bull channel on Tuesday, but the support had held despite the inability of the euro to use support at line L ($1.1126) as a springboard the reverse the trend. However, the NFP provided the springboard and the euro closed the week with a good gain, well away from the bottom of the bull channel.

Single shocks, however unnerving to people who have become complacent, often do not last. We tend to have convenient short term memory house cleaning that wipes away the effects of bad news, unless there is continuing evidence that we now have to deal with its consequences as a new fact of life. The month of June is turning into an interesting time for the euro and for other markets too. The first resistance for the euro is at line K, sitting above $1.70, and therefore clearly way out of reach for the near term. However, the real test for the euro is how well it manages to keep away from the bottom of its bull channel.

Euro-dollar, last = $1.1366 (www.investing.com)

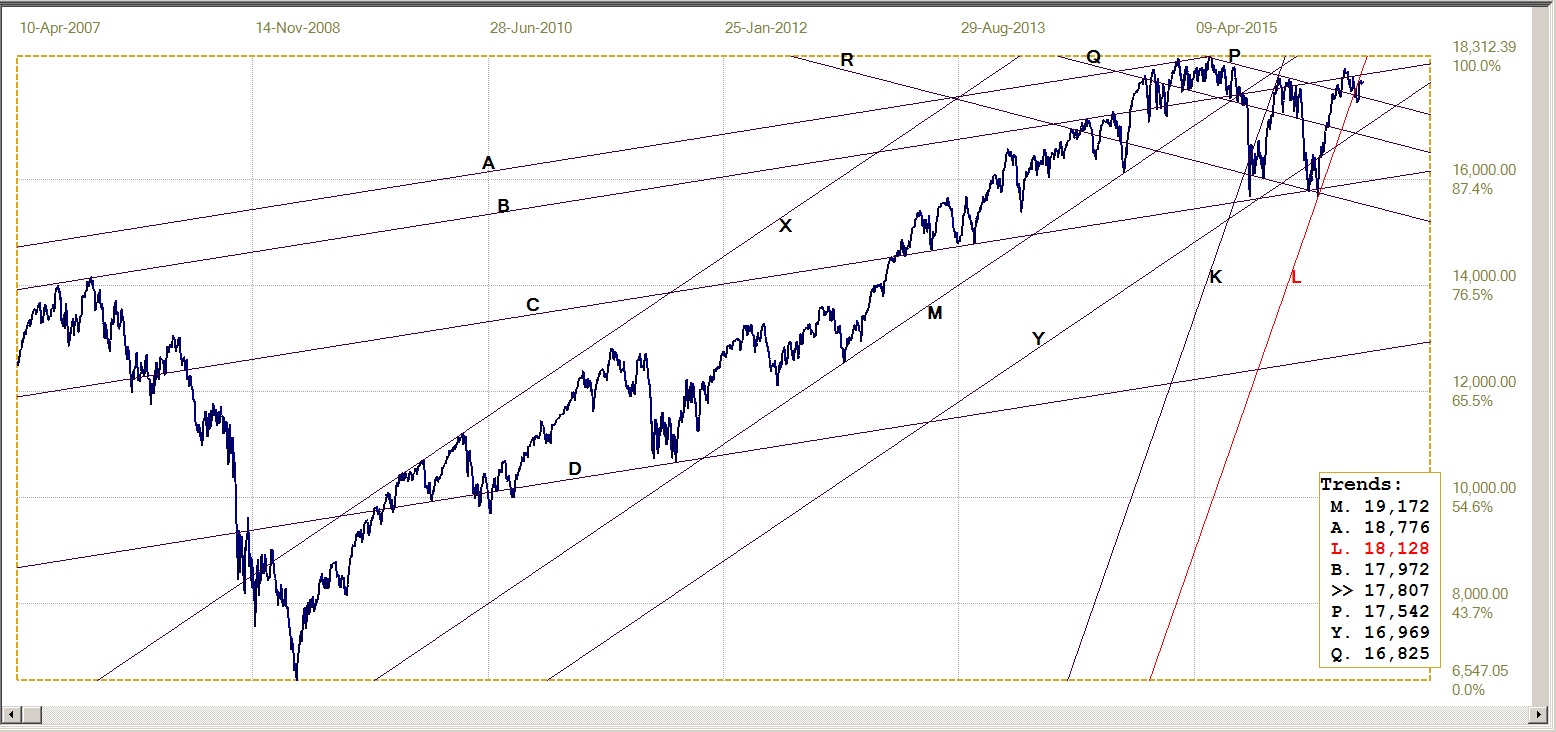

Dow Jones Industrial Average (DJIA)

Since the sell-off during August last year, that also experienced one of the magical instant reversals into a steep recovery that have become a feature of the DJIA, the new bull channel closely contained the recent wild swings. The rally from 15 666 that had started in middle August, reached a high of 17 910 right at line K in early November – for a gain of 14% in about 10 weeks – only to fall back all the way to 15 660 early in February, right on the steep support of line L (18 128). With not too much of a surprise, another immediate magical reversal happened and this time the DJIA managed to exceed the ‘threshold of complacency’ at 18 000 where people seem to accept it as evidence of a growing economy. The DJIA soon failed to hold the desired level and with the value of line L now well above 18 000 it is clear that the DJIA is breaking lower from its 9 month bull channel.

A first sign that the bear could be gnawing at the door will be when the DJIA closes back within the shallow bear channel PQR with line P currently at 17 542. A decline of 360 point is a bit much for a typical one day move, but well within reach of one week of weakness. Now that the break from the channel is clearly on, it would not be a surprise to find the DJIA back within that channel a week or two from now.

The DJIA closed the month of May on Tuesday (not Wednesday as I incorrectly had it last week!) at 17787. On the monthly there was resistance at 17747; a 40 point difference on a decades’ long chart is of no consequence. The technical inference is therefore that a second post all time high rally to set a new high has also run out of steam. The monthly and daily charts therefore both imply the end of the major post 2009 bull market has finally ended and the bear is in the process of taking over.

Dow Jones Industrial Index, last = 17807 (money.cnn.com)

Gold PM Fix - Dollars

The new and shallower bull channel defined last week was spot on as support for the bear move after the break below line V ($1311), which used o be the bottom of the older, steeper bull channel that held the first part of gold’s new bull market, but was too steep to be sustained for long. After holding right at support of line L from Monday to Thursday, the boost from the low NFP had the gold PM fix gold sharply higher, well off the important support of the bull channel.

For most of 2016, the waterfall attacks had typically achieved limited and only brief success before the now more enthusiastic bulls pushed the price of gold higher into a rally that often extinguished the effects of the bear raid in just a number of hours. The major shorts clearly were greatly concerned about May OPTEX and FND, fearing that the results will increase the threat of a short squeeze.

Pressure on the prices started right from the beginning of May and was no longer confined to the usual waterfalls; this time the pressure on the prices was sustained after the initial success of the new attack. This meant the prices remained bearish as they continued to decline. Recent bulls started to panic as they saw their profit getting less or turning into a loss and they closed enough positions to reduce the Commercial net short position by about half from its high earlier the month.

If the price of gold could gradually move higher, it might be quite some time before the bulls would be brave enough, after the repeated hammering they had endured, to return to the market. Now, with the jump in the price after the NFP, they must be sorry they had panicked and can be expected to be trying hard to get back into their positions without giving away too much of the potential profit they had before.

This is not good news for the Commercials and probably will undo much of all the good they had achieved with the month long raid.

Gold price – London PM fix, last = $1240.50 (www.kitco.com)

Gold PM Fix - Euro

With both the euro and the dollar price of gold holding at and then reversing higher from firm support, it is not much of a surprise that the euro price of gold had done the same. On Wednesday, the euro price closed the gap to the bottom of channel KL (€1087) and held there until a small bounce off that support on Friday.

The fact that given the big response of the dollar price to the low NFP managed to overcome a similar kick higher by the euro, tells us that gold was just that little bit stronger on Friday than the European currency. This superiority has to be sustained if the euro price is going to hold to the bull channel. While not essential for the gold bull market to continue, should the euro price remain bullish while the euro itself is gaining on the dollar, would be a good vote of confidence in the metal’s future.

Euro gold price – PM fix in Euro, last = €1094.0 (www.kitco.com)

Silver Daily Fix Chart

It finally proved necessary to also adjust the gradient of the new silver bull channel to accommodate the recent weakness. The gradient of the new channel is, just as all other trend lines, derived from the gradient of the master line, M. The new and shallower bull channel served as support on Wednesday and Thursday, but a slight bounce higher by the London fix on Friday, early in the morning well before the NFP was announced, was extended later after the news for silver to close above $16.30.

This holds promise for further improvement this week, in line with gold

Silver daily fix, last = $16.10 (www.kitco.com)

U.S. 10-year Treasury Note

US 10-year Treasury note, last = 1.700% (www.investing.com)

The yield of the 10-year US Treasury note – after a sideways trend on Thursday – started a slight and consistent down-trend during Asian trading early on Friday, to decline from 1.813% to 1.794%, just prior to the NFP number being announced. It may not sounds like much, but anyone who did some buying in that time frame was most pleasantly surprised when the yield plummeted down to 1.707% immediately after the announcement and then drifted sideways and lower after a brief bounce to close the day at 1.700%. Excellent foresight of what would happen!

The steep decline is of course the result of new expectations that the very low NFP is a sign that a rate hike is now delayed much further into the future than feared by the bond market before the NFP. If the yield hold this level or mover even lower, it will be a reasoned acceptance that the US economy is stagnant with not much hope of a resurgence soon.

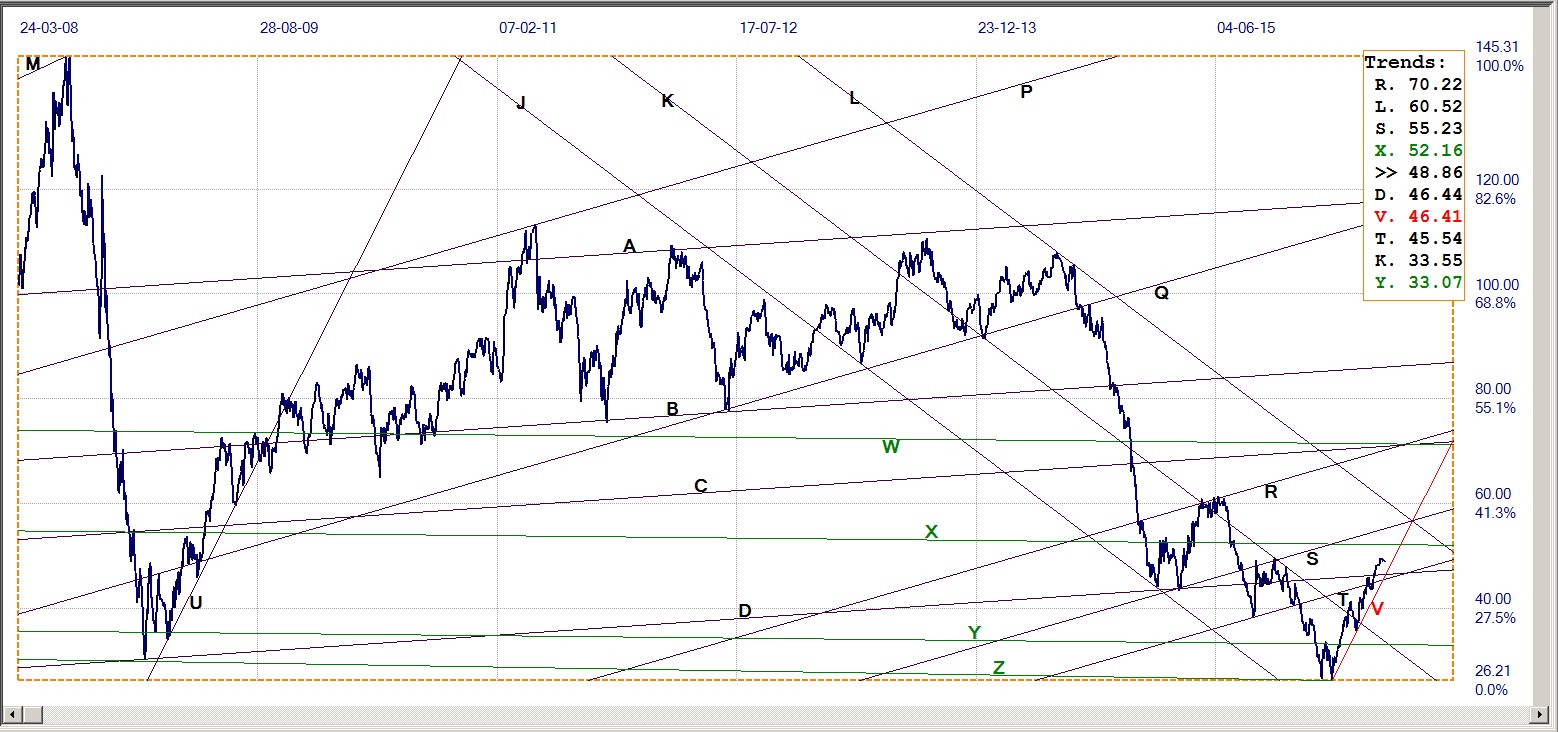

West Texas Intermediate crude. Daily close

The new bull trend in WTI crude is still holding well clear of the steep support along line V ($46.41). The true state of the supply demand relationship remains murky so there is not much incentive to move the price in either direction. $50 is acting as a psychological resistance and therefore the sideways trend is expected to continue sideways below that level until there is a clear reason for a new trend.

WTI crude – Daily close, last = $48.68 (Investing.com)

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com

share

share

share

share

share