Beware The Secular Bear

“A secular bear market can last anywhere from 10 to 20 years and is characterized by below-average returns on a sustained basis.”

In last week’s missive entitled “The Bear Resumes”, I laid out a fairly strong case for maintaining a defensive portfolio posture despite the major averages (as well as many junior miners) being well of their respective 12-month highs. During the ensuing week, I fielded no fewer than fifty messages all chastising me for being such a pessimist and urging me to reconsider due to my outdated and in fact prehistoric analysis of these “modern markets”. In those messages, while not exactly spelled out, the counterpoint argument seemed to follow the logic train of a phrase well-known to sexagenarian investors - “…but it’s different this time” – referencing technological advance and visionary fiscal and monetary policy maneuvers as the panacea for both business cycle and market pain.

In last week’s missive entitled “The Bear Resumes”, I laid out a fairly strong case for maintaining a defensive portfolio posture despite the major averages (as well as many junior miners) being well of their respective 12-month highs. During the ensuing week, I fielded no fewer than fifty messages all chastising me for being such a pessimist and urging me to reconsider due to my outdated and in fact prehistoric analysis of these “modern markets”. In those messages, while not exactly spelled out, the counterpoint argument seemed to follow the logic train of a phrase well-known to sexagenarian investors - “…but it’s different this time” – referencing technological advance and visionary fiscal and monetary policy maneuvers as the panacea for both business cycle and market pain.

Well, as if Mr. Market had been reading these messages, he responded by taking the retail-dominated NASDAQ out behind the woodshed and summarily thrashed it to within an inch of its life while creating havoc in many of the inflation and economically-sensitive sectors including cyclicals and the precious metals. I cite the NASDAQ because it has become the poster child for unfathomable (and immediate) risk-free enrichment, at least in the minds and dreams of the New Generations of investors and speculators that now ride herd on Wall Street. The vast majority of the “meme” stocks reside within the hallowed halls of the NASDAQ exchange and it is their noticeable absence from any recent CNBC topics of discussion that stands out. The “NAZ” went out for the week at a year-to-date loss of 21.16% loss and is now officially and undisputedly in a bear market. What one does not see is the underlying damage in the bulk of small-cap issues where drawdowns of up to 70% are not uncommon.

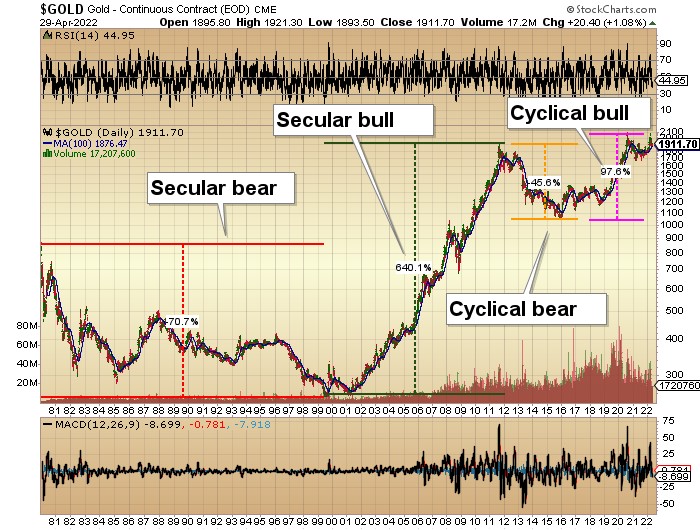

The definition of a bear market is any market that loses in excess of 20% over any given time frame but it should be noted that there are two completely different breeds of the bear: there is the cyclical bear that last usually for months and is part of “normal market volatility” and then there is the dreaded secular bear where it can last for decades and is characterized by sharp, violent reflex rallies followed by plodding, persistent declines.

As I have been writing about since last fall, investors enjoyed the fruits of a Fed-orchestrated secular bull market coming out of the Great Financial Crisis Bailout of 2008 while gold investors have been suffering a dissimilar fate after gold topped at $1,920 in 2011. Being a market deemed integral to “maximum full employment” (one of two Fed mandates), stocks were handed countless lifelines during the last secular bull while gold has been forced to claw and grind its way to the current cyclical bull status minus anything vaguely resembling central bank assistance.

I believe that gold and, to a lesser extend, silver are in long-term secular bull markets since 2002 within which there have been a number of cyclical bears sluffed off as “corrections” by the PM permabulls community. Whether one uses the term “bear” or “correction”, gold and silver have been maddeningly frustrating markets in which to invest due their inability to respond appropriately to unprecedented and egregious quantities of credit creation known as “stimulus”. In fact, I find it rather revealing that all of the Fed policy moves (trillion-dollar purchases of Wall Street member bank-owned securities) did not result in anything resembling “soaring CPI” but once the government’s fiscal stimulus came into play with cheques bypassing the member banks and going directly into the pockets of consumers, only then did monetary velocity receive ventricular fibrillation resulting in escalating consumer prices. It is truly amazing how undemocratic the banks can be when doling out Fed money and the reason is simple: The Fed was created by the banks, for the banks, and their only true mandate is to protect the member banks and they did so by hoarding the gargantuan Fed stimulus only to be allocated to those, as George Carlin famously said, “that belong in the Club”. (and you and I ain’t in it.)

Rants notwithstanding, I believe that there is soon to appear a tradable entry point for the cyclicals and precious metals equities that have been mauled as collateral damage inflicted by the overall broad market rout. Scrambles for liquidity have forced sales of fundamentally sound, low-P/E companies like Newmont Mining and Agnico Eagle as well as zinc-centric Teck Resources, companies that dwell soundly in the category of the deeply-discounted for all the wrong reasons.

Also falling into disrepute are the juniors, both precious and base metals, whose popularity has gone from the penthouse to the outhouse with the recent rise in real interest rates. There is nothing “different this time” in the weakness in the juniors; if Teck can get smoked for a 10% drawdown despite near-record all-time highs in the price of zinc, then there is little reason to realistically expect the junior wannabe’s to outperform. That said, exploration companies like Max Resource Corp. (MAX:TSXV / MXROF:US) (up 132% YTD) have been doing just fine.

The reason for this is found in my experiences of the 1990’s when the commodity markets were mired in a disinflationary malaise. Since valuation could not elicit any help from rising commodity prices, the only events that drove them were new discoveries and with that as a stark reality, the ingenious Canadian mining industry embarked on an unprecedented decade long binge (1987-1997) of one world-class discovery after another across a broad spectrum that included diamonds, gold, nickel, and silver. In a decade of meandering metal prices and low inflation, untold wealth was created through innovation and calculated risk-taking, both of which remain the domain of the junior explorers. As soon as the current market malaise settles down, I think that the New Generation of stock speculators are going to wake up to a painful reality that “story stocks” are just that – “stories” – with little in the manner of substance or dependability upon which to recover the enormous losses inflicted by their fatal attraction to the NASDAQ.

My largest holding and top-ranked junior is one that I continue to believe fits all of the criteria so necessary in today’s financial landscape. Juniors need to have the following key features in order to rise above the throng of TSXV and CSE juniors all furiously waving their hands for recognition and more importantly, funding. They need:

- A resource or evidence of one while residing in the stage of “advanced exploration”

- Favourable jurisdiction

- Ability to raise capital

- Ability to secure permits

- Management expertise and experience

- Market sponsorship, and most importantly,

- Exit strategy

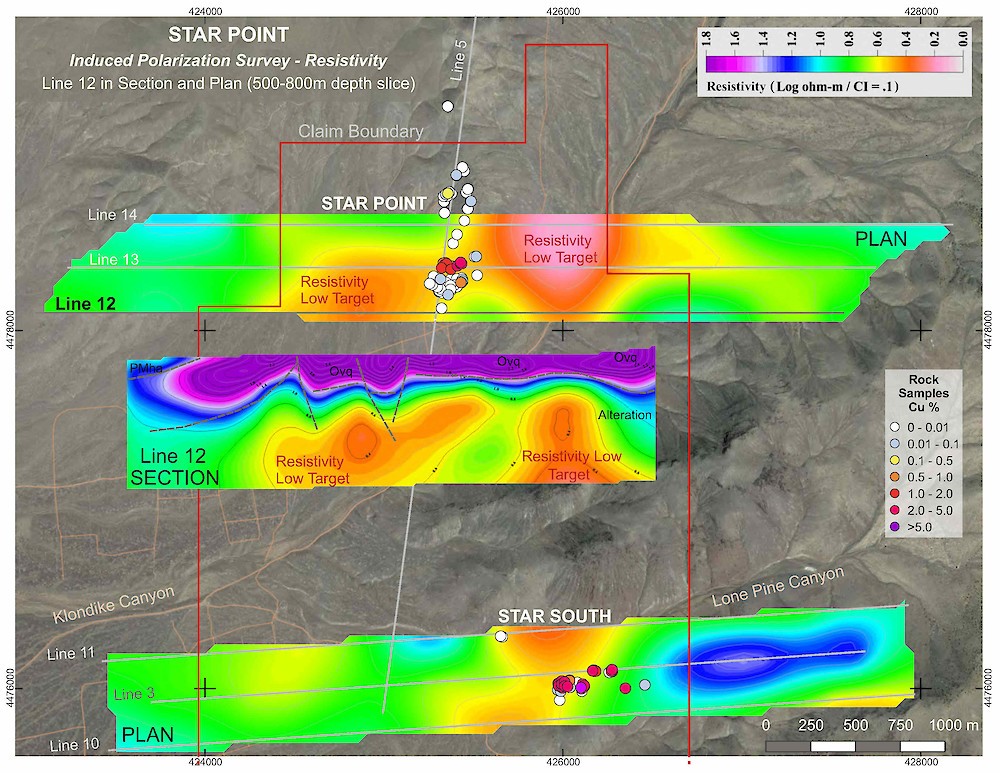

My largest holding is Getchell Gold Corp. (GTCH:TSXV / GGLDF:US OTC QB) and without going into a great deal of detail (email me at [email protected] if you want a “great deal of detail”), they get 5-star ratings in all categories but this year, unlike recent exploration seasons, they are embarking on a maiden drill program at Star Point in Nevada to see what lurks below the old prospector dumps where the material the old-timers left behind ran 1%-plus copper and north of a gram of gold. Geophysical analysis including IP surveys have revealed a number of very large resistivity-low targets that are going to be drilled within days.

When combined with the Fondaway Canyon resource (minimum 1 million ounces of high-grade gold), Getchell gives me a two-pronged assault on both base and precious metals exposure in a perfect location (Nevada) with a $4m treasury and a history of being able to raise money and create shareholder value.

If you do a scroll-down on the Twitter site focusing on FinTwit commentary, the amount of bearish commentary tells me that we are fast approaching the point of “maximum pessimism” which is also the point where risk dissipates and reward potential resurfaces. You see, the bear that has arrived is not a “baby” bear and it is not a “mama” bear; this one is a “grandaddy”, a mammoth “Kodiak” bear. This type of bear market is one where the bear began feeding on canapes in late 2021 and then sat down for the main appetizers in January. Now, he has gorged himself on shrimp cocktail and caviar and is about to prepare for the main course, the entrée, the piece de resistance which will probably arrive with a vengeance but only after he can lure more unsuspecting dip-buyers into the market. Only after a rally like the 11% rebound we had after March 14 retest of the February lows can the bear be lured back from his den. The next few trading sessions will possibly result in a massive capitulation-type reversal that will be tradable but the one sector that is ripe for a rebound is the PM sector. With the FOMC meetings coming up on Tuesday-Wednesday, the arrival of rate hikes has historically marked the lows for gold and silver as they begin their ascents in anticipation of a Fed policy-reversal. I will be allocating cash to my favourite juniors next week but be forewarned: if it follows the pattern of other tradable bottoms, you will be absolutely petrified with fear as you watch stocks go “No-Bid” so I want you to fight the waves of nausea and incontinence and be ready to remove your hedges and load the proverbial gun with this smorgasbord of value.

This is a countertrend trading opportunity in the midst of a secular bear market of Kodiak size and ferocity requiring agility, nerve, and ample dollops of four-leaf clovers and rabbits’ feet.

Forewarned is forearmed…

Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

********

More from Gold-Eagle