Does Gold Like Acronyms? The Golden Story Of SPX, CPI And IMF

SPX continued losses. CPI slowed down. IMF cut its projection of global growth. What does it all imply for the gold market?

Stock Market Turmoil Continues

Let’s start from the US stock market. In the last edition of the Gold News Monitor, we discussed the Wednesday’s stock market turmoil. But the bear market continued later. On Thursday, the SPX extended its losses, declining about 2 percent. It means that traders continued their liquidation sale of risky assets and moved into safe havens, such as gold. The yellow metal jumped above $1,220 on Thursday, as one can see in the chart below.

Chart 1: Gold prices from October 10 to October 12, 2018.

In our Stock Trading Alerts you can read about the current correction from trading perspective. Fundamentally, we do not see reasons to panic. At least not yet. Of course, the financial system is nowadays quite fragile as it used to live on a drip from the Fed. The tightening of monetary policy ends the year of ultra-low interest rates and easy money, so certain corrections are inevitable. However, the bond yields are still historically very low, so the elevated stocks valuations might be actually justified. Hence, gains in gold might be temporary, unless the correction transforms into a genuine bear market, or the Fed becomes more dovish.

Inflation Slows Down

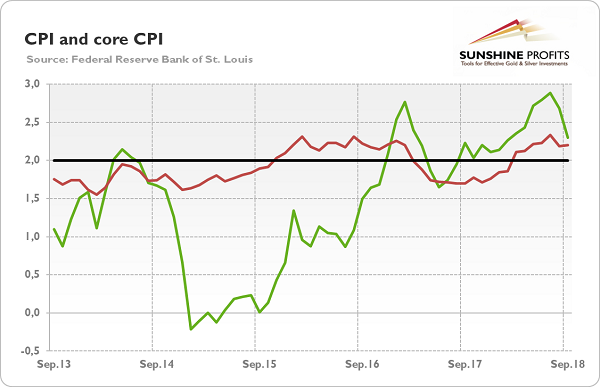

Or we will see the acceleration in inflation. But now we’re seeing the opposite. The CPI rose 0.1 percent in September, following an increase of 0.2 percent in August. The core CPI also moved up 0.1 percent, the same change as in the previous month. Over the last 12 months, the consumer prices jumped 2.3 percent, compared to 2.7 percent increase in August. The slowdown was mainly caused by a notably smaller increase in energy prices. The index for all items less food and energy climbed 2.2 percent, the same as last month, as the next chart shows.

Chart 2: CPI (green line, annual change in %) and core CPI (red line, annual change in %) over the last five years.

Hence, the inflationary pressure eased somewhat in September. However, inflation is still slightly above the Fed’s target. So we don’t expect any changes in the Fed’s policy of gradual hiking the federal funds rate. Surely, trade disruptions and rising shelter prices may actually support inflation in the near future, but there will be no price revolution. And we bet that the new FOMC with Powell as a chair will not allow for a sudden surge in inflation. Precious metals investors should remember about that.

IMF More Pessimistic about Global Economy

Gold should also shine if the global economy significantly slows down or enters the recession. The gold bulls should welcome the new edition of the World Economic Outlook, as the IMF cut its projection of global growth in 2018-2019 by 0.2 percentage point from 3.9 to 3.7 percent. Importantly, the organization also downgraded its forecast for the US economic growth from 2.7 to 2.5 percent in 2019 to reflect the impact of protectionist trade measures. And the balance of risks deteriorated, as “downside risks to global growth have risen in the past six months and the potential for upside surprises has receded.” The trade barriers and political uncertainty rose, while the fiscal stimulus is likely to soften next year. Moreover, the Global Financial Stability Report, also written by the IMF, finds that “global near-term risks to financial stability have increased somewhat, reflecting mounting pressures in emerging market economies and escalating trade tensions.”

However, the global economic expansion continues and most of the risks mentioned by the IMF concern the emerging countries which are sensitive to a strong greenback and rising dollar-denominated rates. The bottom line is thus that some caution is warranted, but it isn’t quite time to panic.

Arkadiusz Sieron

Sunshine Profits - Free Gold Analysis

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017. He is a board member of the Polish Mises Institute of Economic Education, author of several dozen scientific publications (including in such periodicals as the Journal of Risk Research, Prague Economic Papers, Quarterly Journal of Austrian Economics, and Research in Economics), and a regular contributor to GoldPriceForecast.com and SilverPriceForecast.com. His two books, Money, Inflation and Business Cycles and Monetary Policy after the Great Recession, are both published by Routledge. Arkadiusz is also a certified Investment Adviser, a long-time precious metals market enthusiast, and a free market advocate who believes in the power of peaceful and voluntary cooperation of people.