Dollar And Glitter

share

share

share

share

share

share

share

share

share

share

The president’s election has turned more convoluted than even the more complex plots of a top mystery writer. It looks to take more than a week or two, into 2021, to resolve in either one way or another. Time enough then to speculate about what the future might be like. More immediate are the changes during the past week as the dollar and the prices of gold and silver suddenly took off in opposite directions. Can it be that the misty magic crystals people use to discern the future have cleared to make it possible for normal people to also spy trends as they begin to happen?

On the virus front the vaccines are slowly beginning to roll out and, hopefully, will begin to have effect in reducing the infection rates and associated deaths, if not yet during 2020 then doing so early in 2021. In the meantime, the global and US rates of new infections and deaths are still close to or making new highs.

The debate on whether it is necessary for regulations to limit the spread of the virus continues to rave with neither side really willing to listen to the other. The potential for violent rejection of presumed unnecessary or ineffective measures and regulations is on the increase amidst blatant disregard for the use of masks and social distancing. 2021 is going to be an interesting year in more than a few respects.

News from London about a possible mutation of the virus that causes it to become more virulent is disturbing, but not yet confirmed. The normal flu viruses mutate and therefore each flu season tends to require a special vaccine. They are corona viruses, similar to the COVID-19 virus, and if this strain is to begin mutating, it will make the situation much worse; the vaccines that are now being distributed might not be effective with new mutations.

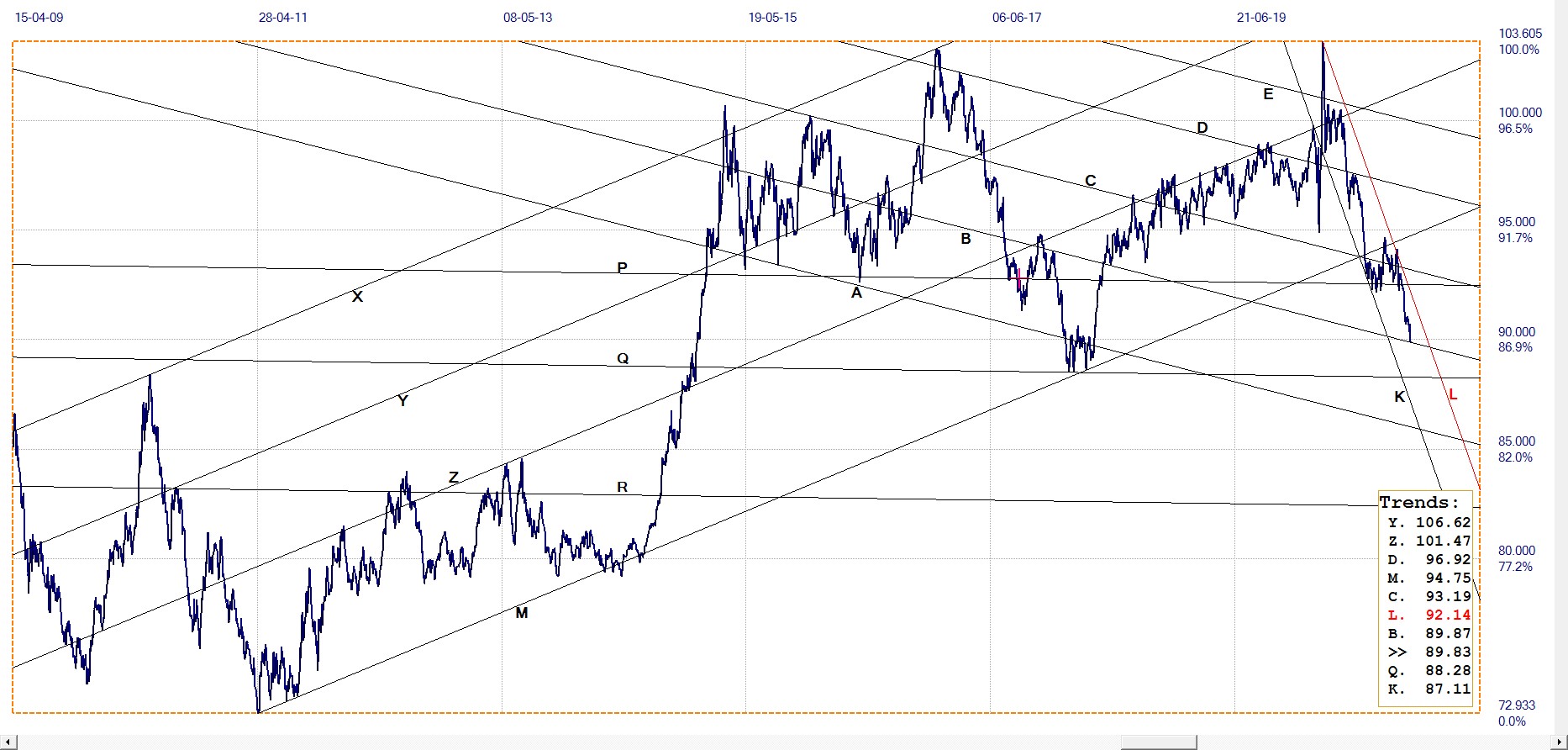

The daily chart of the dollar index shows that the bear trend since its high on 19 March 2020 at 103.605 has kept in the narrow and steep channel KL. There were two quite long periods of consolidation; the first one immediately after the break below line Z and then again more recently between lines P and M. The break below line M late in November had the dollar losing value with only a brief hesitation two weeks ago, before resuming the steep decline last week to end at line B.

Line B is now key support and a rebound is possible, but the bear trend remains in place while channel KL holds. If the dollar manages to hold above line B, it could again enjoy a period of consolidation. An immediate break below line B would be bearish, with line Q a first target for support. This balancing act should make for an interesting week into the end of the year.

Dollar index. Daily close. Last = 89.83

The euro rally out of its consolidation started the last week in November and it was almost a week before the dollar’s sudden break below support on the last day of November. Gold and silver also bottomed on 30 November, making certain that the Comex futures would be at a low on FND, then the metals started their own rallies. Last week saw the price of gold improve by 2.7% from a low of $1831.15 to reach Friday’s PM fix at $1879.75. Silver gained 8.4% from $23.82 to the Friday London fix at $25.815, to close slightly stronger later in the US.

With silver being more suppressed than gold – or more amenable to react lower in response to a selling spree – the converse is now happening; silver spiking steeper than gold now that the pressure is less. Silver nevertheless still is almost $4 (15%) lower than the recent new high and will have to sustain the steep recovery to end the year at a new intermediate high. That implies another two weeks at the same rate of improvement as last week. Not impossible, but if many OTC contracts are set to expire on December 31, there could be a new bout of selling into the year end for both gold and silver.

The euro price of gold improved last week from a low of €1505.57 to €1536.13 on the Friday PM fix, which is a gain of barely 2%. Compared to the 2.7% gain in the dollar price, also in terms of the London PM fix, this indicates that gold displayed a bit of intrinsic strength last week; the improving price is not simply because of the weaker dollar. While not keeping up with silver, as yet, should silver again nearly do as well as last week, the price of gold could begin to follow silver’s lead and also accelerate at a faster rate.

The presidential election is still the top news topic in the US and probably the world. Two conclusions appear to be reasonable at the moment; there is substantial, quite credible, evidence that in some key states the voting process was not as clean and above board as it should have been and secondly, based on the persistent attempts to block the investigation into voter fraud at all levels, the organisation behind the fraud is both widespread and very powerful.

There appears to be much credible evidence of how fraud was committed but how this problem is to be dealt with now and what the outcome will be is not yet clear. There are too many imponderables that have to be resolved first, from what the constitution dictates down to what is to be done about evidence that may have been destroyed before proper investigation could be done. It is therefore still too premature to explore what 2021 and the years to come will bring forth.

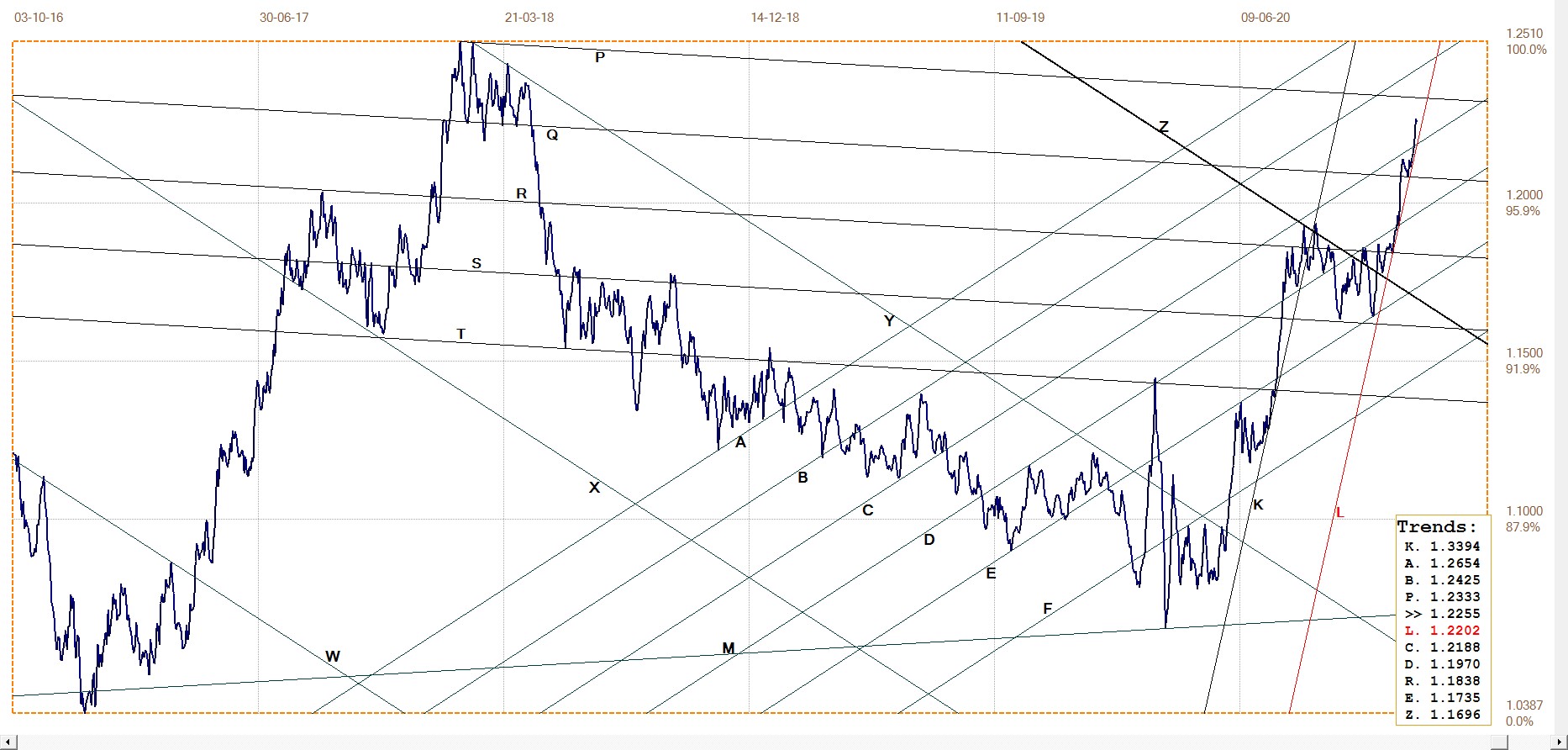

Euro–Dollar

The euro is keeping within steep bull channel KL and has broken clear above lines Q and C. The outlook remains bullish for the euro as long as it can hold above line K, or at least hold the break above line C. This may well depend on whether the dollar index is to hold at the support of line B in the earlier chart, or break lower soon.

Euro–dollar, last = $1.2255 (www.investing.com)

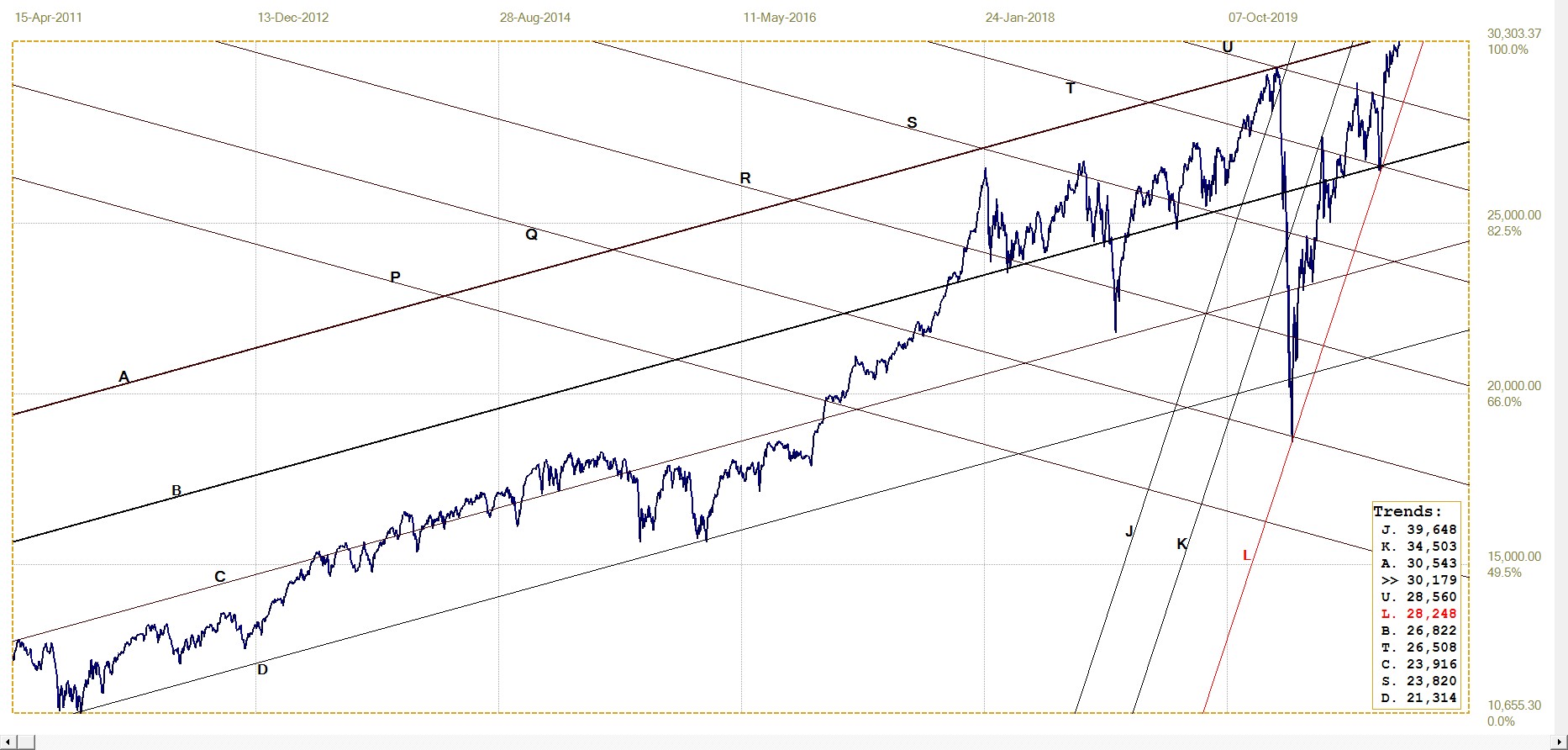

DJIA Daily close

DJIA, last = 30179.06 (money.cnn.com)

The DJIA achieved another new all-time high on 17 December. When COVID took hold in the US in February/March 2020 and restrictions were introduced to limit its spread, most comments on the future of Wall Street were negative, with some of them predicting a major crash. As expected, the stock market took a dive in March, but unexpectedly reversed trend steeply after 23 March. Many of the commentators – myself included – saw the hand of the Fed in this new rally, as had happened in March 2009 to end the 2008/9 sell-off.

It was thought that with Wall Street so often quoted as evidence of the economic success of the Trump administration, that the stock market had to be kept elevated to ensure better odds for Trump’s re-election in November. The election came and went and Wall Street remained elevated and ramped even higher. Part reason for the persistent rally was seen in the massive COVID-related handouts and later it also became known that the Fed had been subsidising its primary dealer banks with literally $trillions, of which a fair amount would have found their way to Wall Street.

Now, with a third wave of infections still rife, it is puzzling that the long term rally still continues. Why would investors – or is it mostly daytraders? – still put money into Wall Street? Is it like the dot.com rally in 1999 that momentum trading and a promise of good profits have credibility because the market is moving higher all the time? In effect a widespread belief that what happened yesterday and last week will continue through tomorrow into next week. Is the DJIA rally going to continue until the top of channel AD is reached at above 30 500?

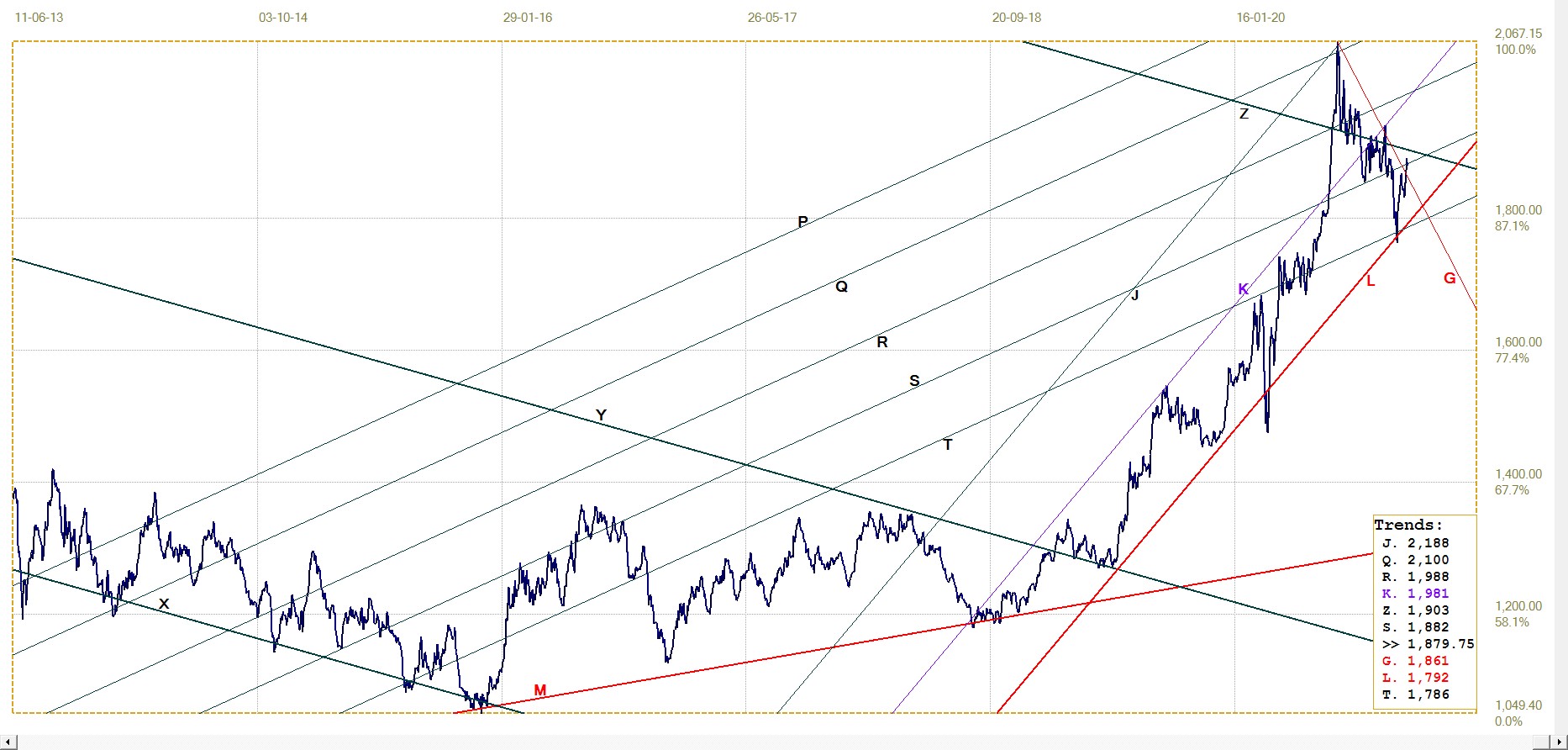

Gold London PM fix – Dollars

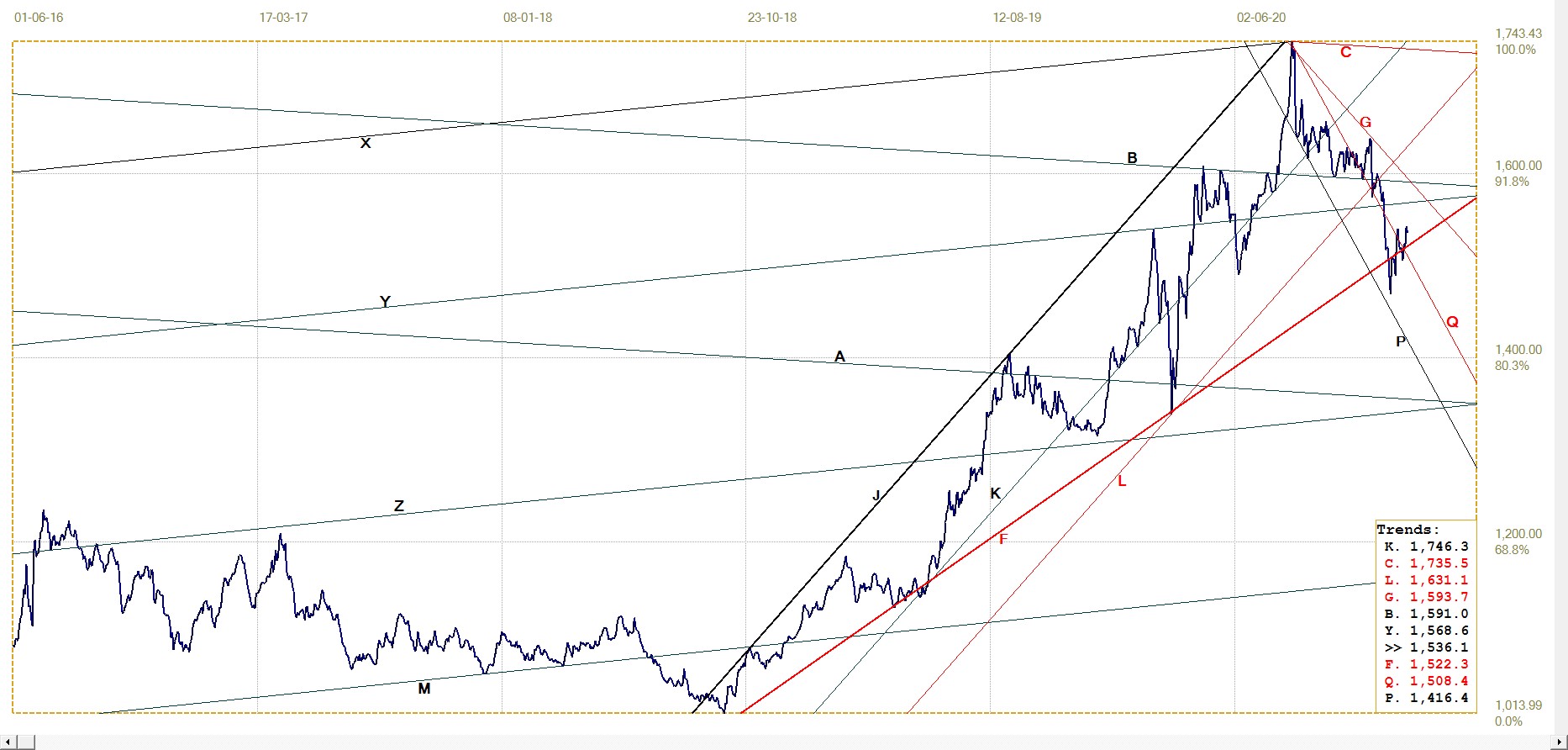

As discussed earlier, the price of gold last week did not perform as well as the price of silver had done. Yet the move higher was good enough to break firstly above the resistance of line G and then also effect a marginal break above line S. This places the price within reach of the important resistance along line Z, top of channel XYZ.

A brief penetration above line Z not long after the August attack on PM prices had started, failed to hold and was followed by a steep decline. It is to be hoped that a new break higher, perhaps before Christmas, will happen and have more success in holding the break. This might be easier said than done if the year-end is associated with many OTC contracts. Then we might see a repetition of what had happened up until 30 November as the holders of such contracts are cheated out of their profits.

Gold price – London PM fix, last = $1879.75 (www.kitco.com)

Euro–gold PM fix

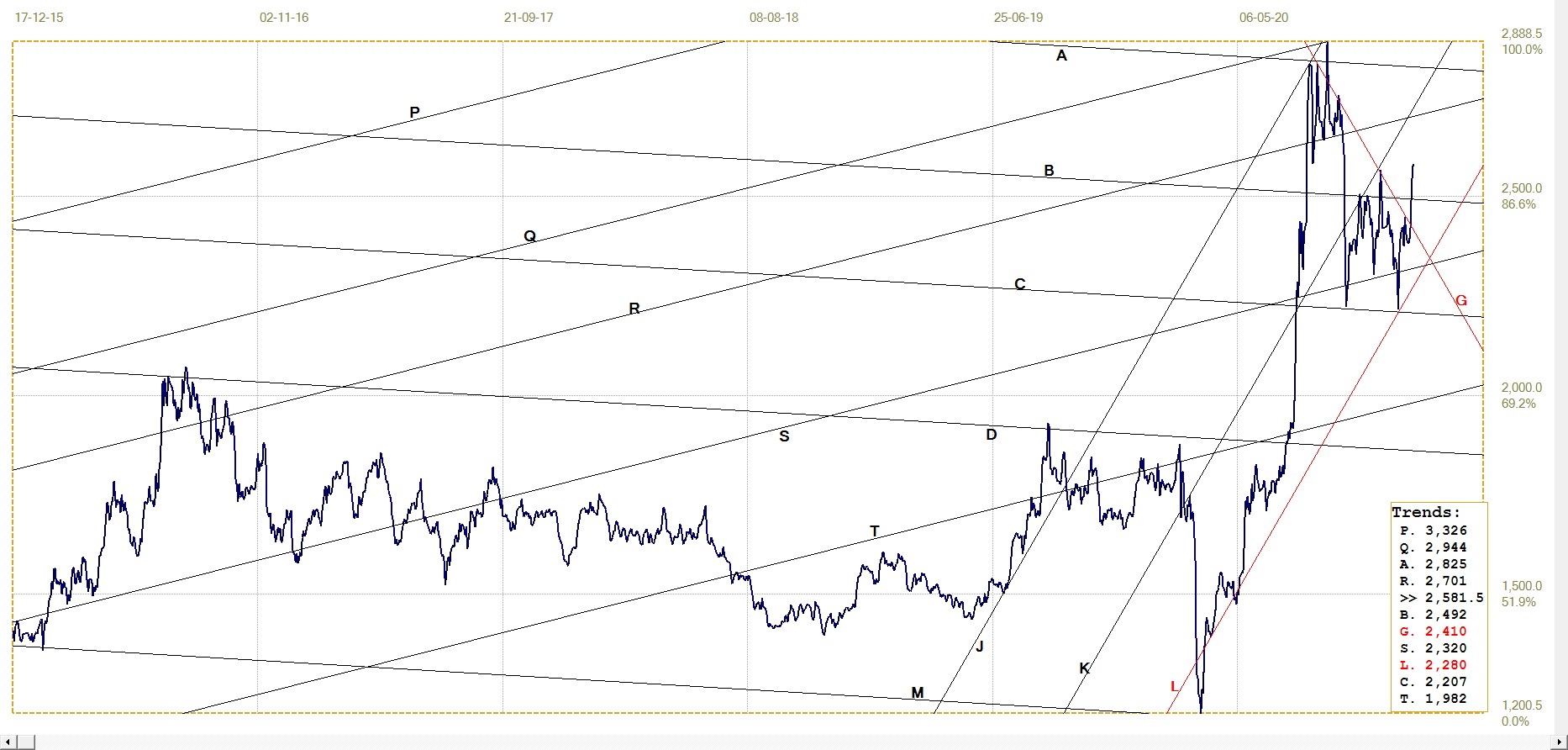

Given the inhibiting effect of the stronger euro, it is a good surprise to see the euro price of gold again breaking higher from channel PQ and back into megaphone JF. It is to be hoped that this performance will prove more successful than the recent break above line L, which barely broke above line G.

Euro gold price – PM fix in Euro. Last = €1536.1 (www.kitco.com)

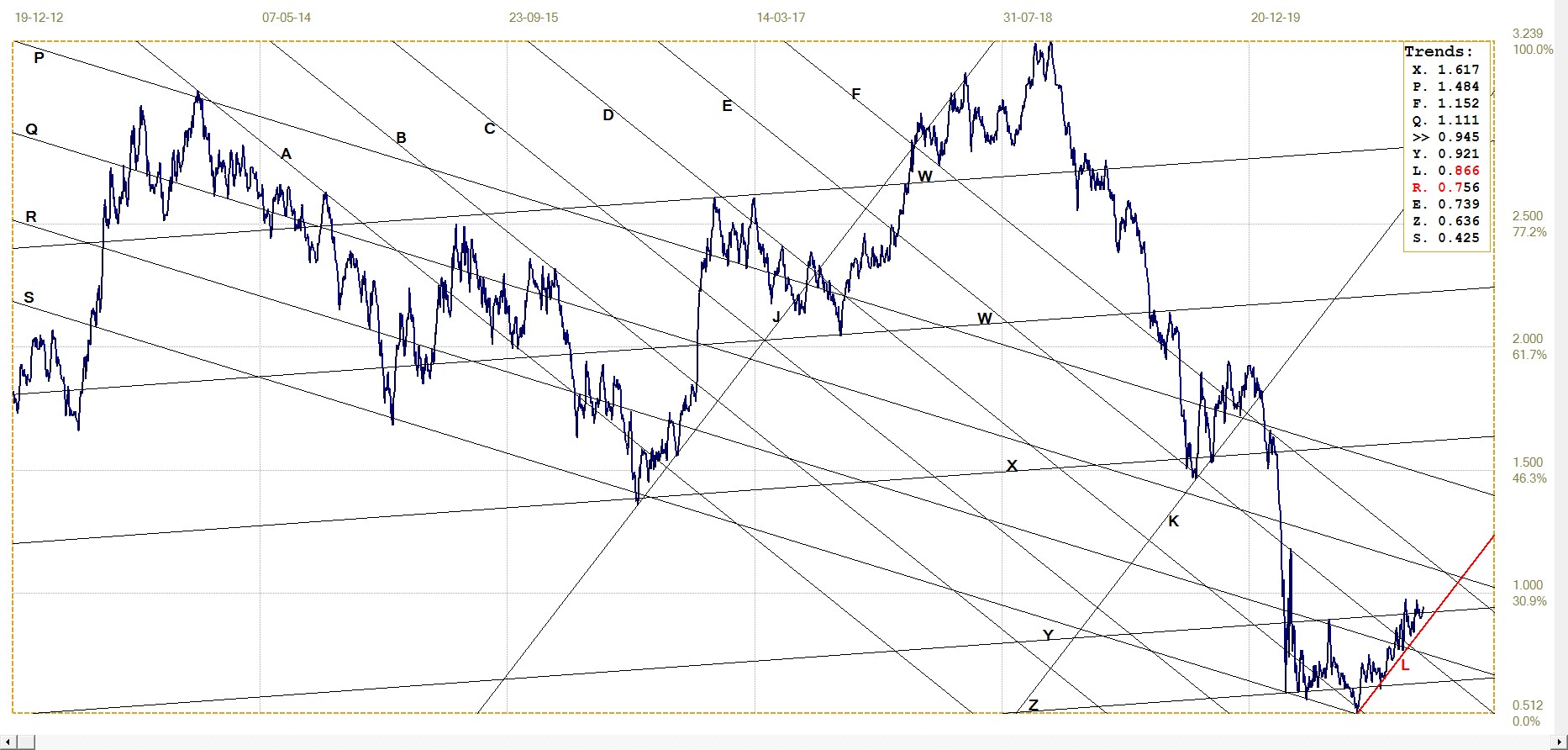

Silver Daily London Fix

Silver daily London fix, last = $25.815 (www.kitco.com)

Last week, the price of silver finally managed to break clear above line G after having first failed to do so and then was stuck in a tight consolidation. The break higher was sufficient to also break clear above line B and has now achieved a new intermediate high since the punishment of the price had started early in August. It even seems possible to break back into the top half of bull channel JKL before the price achieves a new post 2011 high.

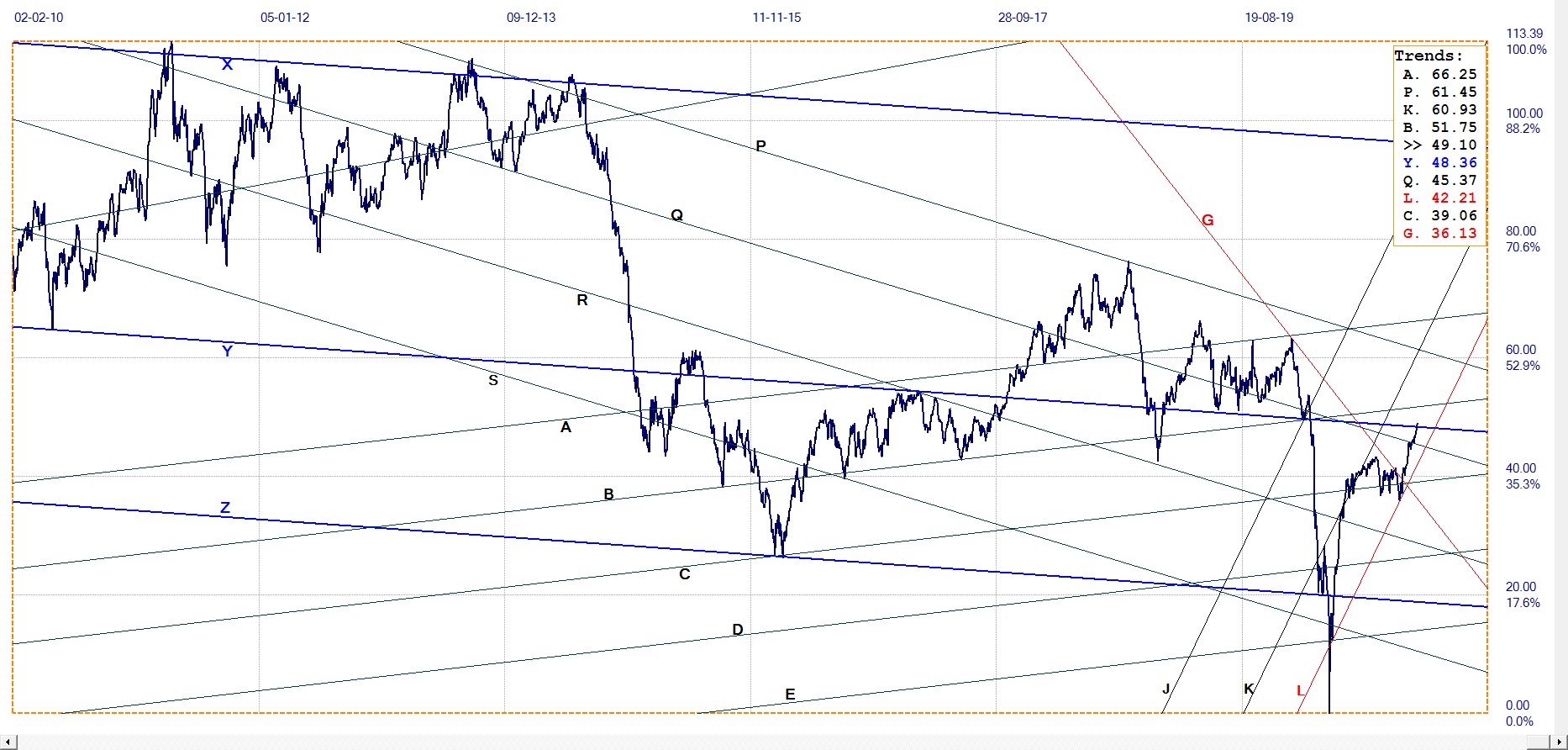

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 0.945% (www.investing.com )

The yield on the US 19-year Treasury note earlier formed a near double top at 0.973% and is now holding only a little lower at 0.945%. While following the increasing gradient of channel KL, it nevertheless looks as if there are forces that would not like to see the yield above 1%.

If that were to happen, it might be seen as a signal that the long term low interest rate of the economic summer is due to experience an autumn, that perhaps will be followed by a higher rate winter. This would not be welcome at all with Wall Street at super high levels and with COVID still very active.

West Texas Intermediate crude. Daily close

The potential prospect of higher rates is joined by the rising price of crude to cause a sense of nervousness among investors and economists. And also in government circles. The minor break above line Y is a warning of what could happen, should the break hold and extend higher to bring a whiff of inflation.

WTI crude – Daily close, last = $49.10 (www.investing.com )

********

share

share

share

share

share